Here Are 4 Reasons Why Intel Stock Plunged 16% Last Friday

Last Friday on 24 July 2020, Intel closed 16.24% down.

Although I do not own any Intel stock, I was curious why it fell after releasing their Q2 2020 results.

Just a while ago, I saw the news that after 15 years of partnership, Apple decided to break up with Intel and stop using its chips for Macs.

Here are four reasons why I think Intel fell by more than 16%:

1. Delay of Their 7 Nanometer Chips by About Six Months

Their rival AMD (Advanced Micro Devices) has already started selling their 7 nm chips.

This means that technologically, Intel is lagging behind AMD.

In the fast-paced technological environment, this delay is big news. After all, Intel’s competitive advantage will depend a lot on its technological advances.

See also: Our free investing telegram channel. We post daily.

2. Expects Total Revenue in 3rd Quarter To Drop

Intel is a huge company.

One downside to being a huge company is that it is hard to maintain a high growth rate.

For Intel, they expect total revenues in the 3rd quarter of 2020 to reduce 5.16% year on year to $18.2 billion.

3. Gross Margin Dropped From 59.8% to 53.3%

Intel gross margin was 59.8% in 2Q 2019, now it has dropped to 53.3%. That is a sharp drop.

A drop in gross margin can be a sign of a drop in terms of its pricing power and potential competitive advantage.

Definitely not a good sign if it persists.

Also read: “Patience Produce Uncommon Profits” – Why Patience in Investing is Vital.

4. Exposure to China

Intel has exposure to China.

Recently US-China tensions are on the rise again. And that is not good news to add to Intel’s recent woes.

China is in fact Intel’s largest market. In fiscal 2019, they generated 28% of its revenue or about $20 billion from China.

Intel’s largest facilities are also located in Chengdu and Dalian.

In Conclusion

I think that Intel might be losing its long-term competitiveness in the market. In their industry, technological advantages are also an important source of competitive advantage. Being big and having economies of scale is no longer enough.

As to whether the company is currently undervalued or not, we will need to do our own valuation assumptions on that and decide.

See also: My 5 Key Takeaway From Temasek Portfolio Value in 2020.

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Chris Lee Susanto

Founder of the value investing blog Re-ThinkWealth.com (if you type “value investing blog” in Google, his blog is likely the first one). Being a full-time investor himself, Chris knows that he did not beat the S&P 500 return so far (as of the time of this writing) by listening to stock tips. So, when he teaches, he also doesn’t believe in giving stock tips as it is not sustainable for you in the long run. He will teach you how to make your own intelligent decisions with his 4M1S framework. Feel free to also join his free investment telegram channel here.

Last Friday on 24 July 2020, Intel closed 16.24% down.

Although I do not own any Intel stock, I was curious why it fell after releasing their Q2 2020 results.

Just a while ago, I saw the news that after 15 years of partnership, Apple decided to break up with Intel and stop using its chips for Macs.

Here are four reasons why I think Intel fell by more than 16%:

1. Delay of Their 7 Nanometer Chips by About Six Months

Their rival AMD (Advanced Micro Devices) has already started selling their 7 nm chips.

This means that technologically, Intel is lagging behind AMD.

In the fast-paced technological environment, this delay is big news. After all, Intel’s competitive advantage will depend a lot on its technological advances.

See also: Our free investing telegram channel. We post daily.

2. Expects Total Revenue in 3rd Quarter To Drop

Intel is a huge company.

One downside to being a huge company is that it is hard to maintain a high growth rate.

For Intel, they expect total revenues in the 3rd quarter of 2020 to reduce 5.16% year on year to $18.2 billion.

3. Gross Margin Dropped From 59.8% to 53.3%

Intel gross margin was 59.8% in 2Q 2019, now it has dropped to 53.3%. That is a sharp drop.

A drop in gross margin can be a sign of a drop in terms of its pricing power and potential competitive advantage.

Definitely not a good sign if it persists.

Also read: “Patience Produce Uncommon Profits” – Why Patience in Investing is Vital.

4. Exposure to China

Intel has exposure to China.

Recently US-China tensions are on the rise again. And that is not good news to add to Intel’s recent woes.

China is in fact Intel’s largest market. In fiscal 2019, they generated 28% of its revenue or about $20 billion from China.

Intel’s largest facilities are also located in Chengdu and Dalian.

In Conclusion

I think that Intel might be losing its long-term competitiveness in the market. In their industry, technological advantages are also an important source of competitive advantage. Being big and having economies of scale is no longer enough.

As to whether the company is currently undervalued or not, we will need to do our own valuation assumptions on that and decide.

See also: My 5 Key Takeaway From Temasek Portfolio Value in 2020.

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Especially For Ambitious Professionals and Business Owners

- Our Telegram Channel – If you’d like to hear from us daily on stocks, business, economy, and value investing knowledge, please join our free telegram channel here.

- Our Value Investing Mentorship Program – We specialize in coaching (1-on-1) ambitious professionals and business owners looking to learn how to invest in stocks safely and sustainably. Learn more about mentorship with Chris here.

Read also now:

How I Review My Stocks In A Simple Way- 28.11.2016

It is nearing the end of the year and I am doing a review of all my 4 stocks in a simple way, namely Mobile Telesystems (NYSE:MBT), Keryx Biopharmaceuticals (NASDAQ:KERX), Keppel DC REIT (SGX:AJBU) and Keppel Corporation (SGX:BN4). When I do my stock review, it has to...

Here’s What I Learnt From Trump Winning The US Election 2016…

This week, history was made. It was the first time that someone like Trump actually became the US president. And it's the 45th US president, I mean, the number 45 is also so easy to remember so it will definitely go down in history as the craziest thing that happened...

Investing Is The Same As Gambling, Or Is It?

A few days back, I was at a carnival at Singapore Management University (SMU) whereby they have games and foods lined up. After I played the games, I was given lucky draw slips. The lucky draw's prizes were quite attractive, there were three prizes-- iPod Nano 16 GB,...

3 Reasons Why You Should Only Invest In Something You Understand

1) You Tend To Be More Competent In Things You Understand There are things you know and there are things you think you know There are things we understand and there are things that somehow always seemed so Greek to us One thing for sure is that we can only be...

My Stock Update: Keppel DC REIT Q2 DPU up 3.1%– Will I Sell?

What Keppel DC REIT Do Keppel DC REIT (SGX: AJBU) is a Singapore-based real estate investment trust (REIT). It was established with the main investment strategy of investing in a portfolio of income-producing real estate assets. They are primarily used for data centre...

Mr. Lim Say Boon, Chief Investment Officer of DBS Wealth Management’s 8 Predictions for The 2nd Half 2016 Market Outlook

This is what I have gathered from Mr Lim Say Boon, Chief Investment Officer of DBS Wealth Management's 8 predictions for the 2nd half 2016 market outlook: Brexit will not break EU but will break European stocks Global economy will continue to suffer and corporate...

Valuing Mobile Telesystems (NYSE: MBT) Using H Dividend Discount Model

Summary MBT is a telecommunications company with more than 100,000,000 subscribers and is Russia’s largest mobile operator and has high payout ratio close to their Free Cash Flow-- which warrant the use of dividend discount model (DDM) to value it H Dividend Discount...

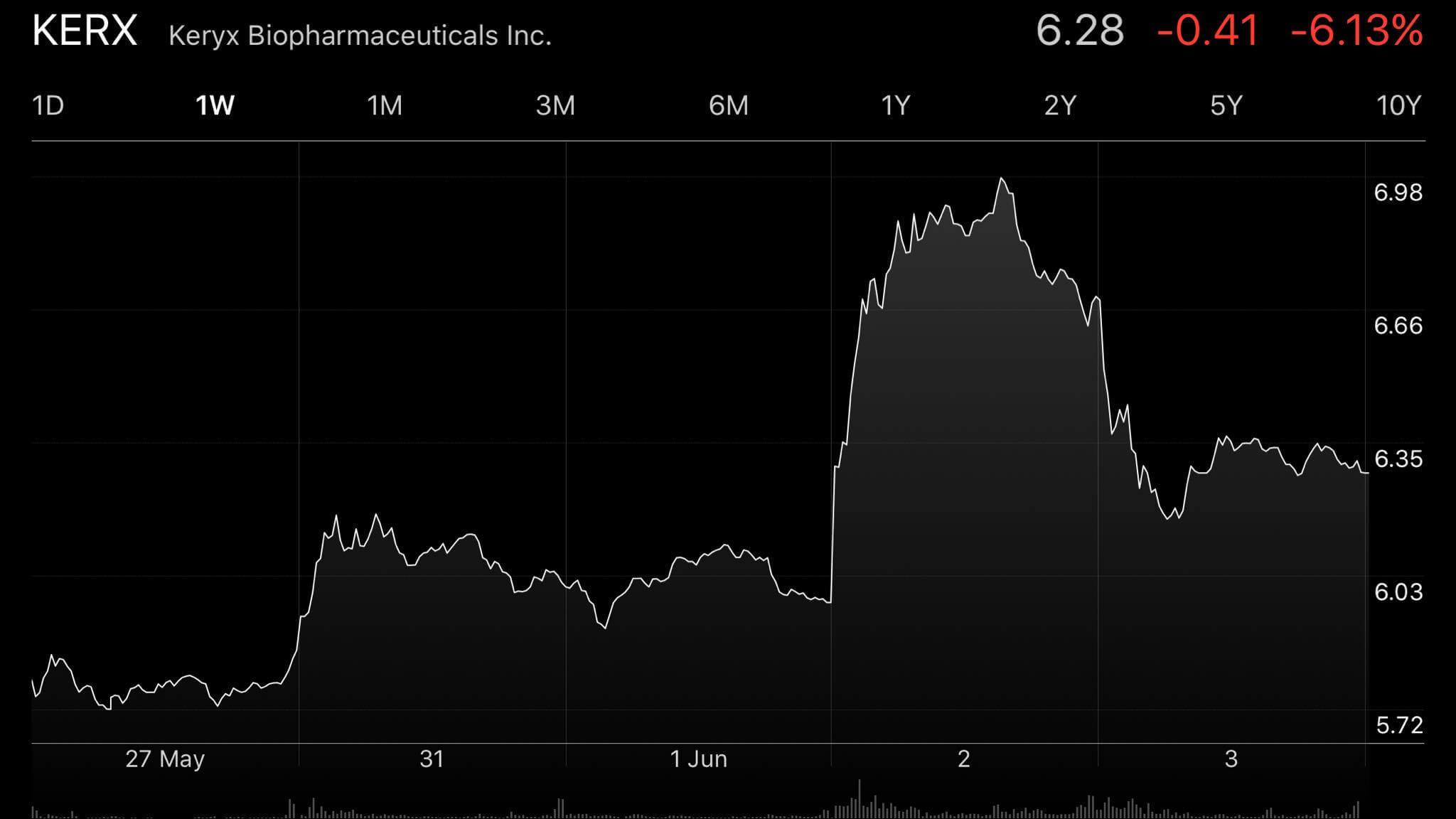

Keryx Biopharmaceuticals Went Up 11.87% On 2 June 2016– BUT Should It?

Keryx Biopharmaceuticals (NASDAQ: KERX) As Part Of My Portfolio KERX is one of the more interesting stock in my portfolio-- and it is also a growth stock that has the potential to be a multi-bagger. What is a multi-bagger? "A multibagger is an investment that has...

Here Is What I Learnt From Watching Money Monster

I am a fan of George Clooney. The latest movie that he acted in is called Money Monster. This article aims to share what I have learnt from watching the movie-- from the perspective of someone who love investing. Before I share with you the lessons that I learnt, I...

#FAQ What To Take Note When Using Past Returns To Estimate Future Returns Of Stocks

Past Equal To Future? We have to take note that since expected returns we expect to receive from a stock investment is based on assumptions using past returns, we are basing the assumption that the past would equal to the future. This assumption would not be relevant...

Addition to My Family Portfolio- A Biotechnology ETF!

One of the first stock that I bought was called iShares Nasdaq Biotechnology ETF (NASDAQ: IBB). I bought it on 5th February 2015 at $310.51 and sold it on 13th July 2015 at $380, netting a cool 21.39%. I like biotechnology stock and so far I have had good experience...

7 Offline Channels For Leads And Their Real Cost

7 Offline Channels for leads and their real cost So much ado has been made about leads and their real cost. But what are the channels that you, the business owner or salesperson, can use to get more leads? The role of face-to-face event prospecting is in the business...