Options

Part 1 of 2: Here’s How to Use The Black-Scholes Model to Price Options

Chris Lee Susanto, Founder at Re-ThinkWealth.com

14 October 2018

This is the first of the two-part article series on The Black-Scholes model. The first part will cover how we can use The Black-Scholes model to price options and the second part, the limitations of it.

Summary

- The Black-Scholes Model is used to price options.

- In calculating the fair price of the put or call options, there are six variables that are taken into account: time to expiry, the underlying stock price at the time, volatility of the underlying stock, type of option, strike price and risk-free rate.

- The options pricing online calculator can be found for free here at TradingToday.com.

What is the Black-Scholes Model?

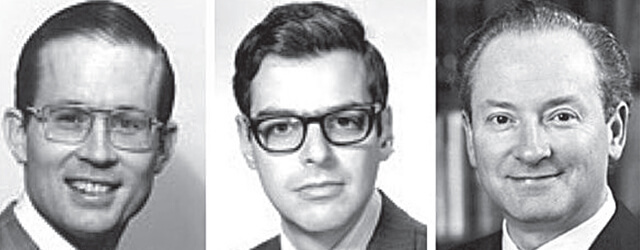

Source: Global Finance Magazine

The Black-Scholes model was first developed by three economists. Two of them – Myron Scholes and Robert Merton – received a Nobel prize in 1997 for their work in this model. The Black-Scholes model is also commonly known as the options pricing model. And as the name indicates, it is used to price options in order to know the fair price for the call or put options.

In calculating the fair price of the call or put options using the model, it will take into account six variables. The six variables are time to expiry, the underlying stock price at the time, volatility of the underlying stock, type of option, strike price and risk-free rate. These six variables are all taken into account in the Black-Scholes Model. For example, the longer the time to expiry of the options, the more expensive the option will be. The further the price of the underlying stock price at the time to its strike price, the cheaper or more expensive the options will be depending on if it is a put or call options. The higher the volatility, the more expensive the options. And lastly, higher interest rates will cause put prices to decrease and call prices to increase and vice versa.

There also a few more assumptions that the Black Scholes model used to come out with the pricing for options. The first is that the stock does not pay any dividends during the options life. Second, the Black-Scholes model assumes that the type of option is European which means that the option can only be exercised on the expiration date. The model also assumes that the stock market is efficient – which means that anytime the stock market may go up or down – with both being an equal probability. The last important assumption is that the interest rates remain constant from the time the options were bought or sold. Rising interest rates will result in the put options to fall in value and call options to rise in value because theoretically, costs are higher to buy stocks when interest rates increase.

How Can We Use the Black-Scholes Model to Price Options?

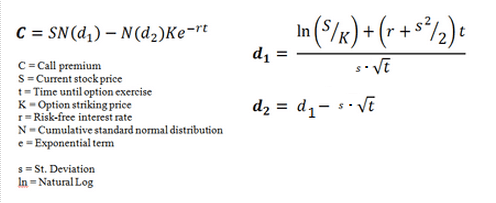

Source: Investopedia

The above image shows the full original formula of how we can use the Black-Scholes Model to price options. It may look complicated but mainly the key input that we have to put in are the current stock price, the strike price, time to expire in days, the volatility or also known as the implied volatility in % terms as well as the current risk-free interest rate.

Fortunately for us, we can use an online Black Scholes Model calculator to calculate the options pricing for us. We only need to enter the fields required and the calculator is able to do the rest for us. The calculator can be found here at TradingToday.com. To test out the calculator, I did a calculation on a call option pricing on one of the stocks of my choice in the US options market. See the screenshot below.

New update as of 24 May 2022: TradingToday calculator seems to be offline the last I checked. I found another calculator by Good Calculators, which also has The Black Scholes Option Calculator.

Source: TradingToday

The calculator showed me a value of about $7.30 as you can see above for the call options. I then compared it with the real call options pricing value in the US options market which is lower at $6.38 – which might indicate that the current options market is pricing the options too cheaply. Or there is also a possibility that the parameters or assumptions the market is currently using are a little different than the one that I use. But more importantly, through this knowledge, we will be able to know how the options price will behave when certain conditions change such as the interest rate and the volatility – and profit from it. And my personal favourite is through selling the options to get premiums.

In the second part of the article, I am going to share with you guys the limitations of The Black-Scholes Model and how we can take advantage of it.

Disclaimer:

The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

Remembering Daniel Kahneman: Author of Thinking, Fast and Slow

The world of behavioral economics and psychology lost a giant with the passing of Daniel Kahneman in March …

Ray Dalio’s Gems: My Key Learnings for Life and Success (Updated Regularly)

Ray Dalio is a global macro investor for more than 50 years, who founded Bridgewater Associates out of …

Asbury Automotive: An Undervalued Gem in The Stock Market?

I have owned shares in Asbury Automotive Group, Inc., for about 18 months. Asbury is essentially a collection of …

Recession Fears and Value Investing: Navigating Uncertainty and Building Long-Term Wealth

In the past year, the world has been grappling with a looming recession and high inflation. There is a question of whether we […]

Conquering the Inner Market: Psychology for Investing Success

The concept of “Antifragile” is popularized by Nassim Nicholas Taleb in his book that is aptly named “Antifragile”. What is Antifragile? …

Becoming Antifragile in Stock Investing by Embracing The Volatility

The concept of “Antifragile” is popularized by Nassim Nicholas Taleb in his book that is aptly named “Antifragile”. What is Antifragile? …

Demystifying the S&P 500: A Beginner’s Guide to America’s Stock Market Powerhouse

Have you ever heard of the S&P 500? This mysterious abbreviation often pops up in financial news, leaving many wondering what is it […]

Here’s How to Budget with Value Investing Principles

For a lot of people, budgeting their finances feels like a chore. In this article, I will share my thought process on how we view budgeting …

Wait, Wait!

I often share insights that I do not share in this blog over at my Facebook page. Don’t forget to like it before you go!

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

Remembering Daniel Kahneman: Author of Thinking, Fast and Slow

The world of behavioral economics and psychology lost a giant with the passing of Daniel Kahneman in March …

Ray Dalio’s Gems: My Key Learnings for Life and Success (Updated Regularly)

Ray Dalio is a global macro investor for more than 50 years, who founded Bridgewater Associates out of …

Asbury Automotive: An Undervalued Gem in The Stock Market?

I have owned shares in Asbury Automotive Group, Inc., for about 18 months. Asbury is essentially a collection of …

Recession Fears and Value Investing: Navigating Uncertainty and Building Long-Term Wealth

In the past year, the world has been grappling with a looming recession and high inflation. There is a question of whether we […]