Options

Part 1 of 2: Here’s How to Use The Black-Scholes Model to Price Options

Chris Lee Susanto, Founder at Re-ThinkWealth.com

14 October 2018

This is the first of the two-part article series on The Black-Scholes model. The first part will cover how we can use The Black-Scholes model to price options and the second part, the limitations of it.

Summary

- The Black-Scholes Model is used to price options.

- In calculating the fair price of the put or call options, there are six variables that are taken into account: time to expiry, the underlying stock price at the time, volatility of the underlying stock, type of option, strike price and risk-free rate.

- The options pricing online calculator can be found for free here at TradingToday.com.

What is the Black-Scholes Model?

Source: Global Finance Magazine

The Black-Scholes model was first developed by three economists. Two of them – Myron Scholes and Robert Merton – received a Nobel prize in 1997 for their work in this model. The Black-Scholes model is also commonly known as the options pricing model. And as the name indicates, it is used to price options in order to know the fair price for the call or put options.

In calculating the fair price of the call or put options using the model, it will take into account six variables. The six variables are time to expiry, the underlying stock price at the time, volatility of the underlying stock, type of option, strike price and risk-free rate. These six variables are all taken into account in the Black-Scholes Model. For example, the longer the time to expiry of the options, the more expensive the option will be. The further the price of the underlying stock price at the time to its strike price, the cheaper or more expensive the options will be depending on if it is a put or call options. The higher the volatility, the more expensive the options. And lastly, higher interest rates will cause put prices to decrease and call prices to increase and vice versa.

There also a few more assumptions that the Black Scholes model used to come out with the pricing for options. The first is that the stock does not pay any dividends during the options life. Second, the Black-Scholes model assumes that the type of option is European which means that the option can only be exercised on the expiration date. The model also assumes that the stock market is efficient – which means that anytime the stock market may go up or down – with both being an equal probability. The last important assumption is that the interest rates remain constant from the time the options were bought or sold. Rising interest rates will result in the put options to fall in value and call options to rise in value because theoretically, costs are higher to buy stocks when interest rates increase.

How Can We Use the Black-Scholes Model to Price Options?

Source: Investopedia

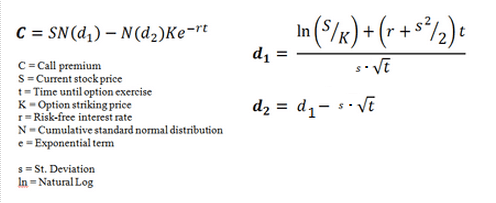

The above image shows the full original formula of how we can use the Black-Scholes Model to price options. It may look complicated but mainly the key input that we have to put in are the current stock price, the strike price, time to expire in days, the volatility or also known as the implied volatility in % terms as well as the current risk-free interest rate.

Fortunately for us, we can use an online Black Scholes Model calculator to calculate the options pricing for us. We only need to enter the fields required and the calculator is able to do the rest for us. The calculator can be found here at TradingToday.com. To test out the calculator, I did a calculation on a call option pricing on one of the stocks of my choice in the US options market. See the screenshot below.

New update as of 24 May 2022: TradingToday calculator seems to be offline the last I checked. I found another calculator by Good Calculators, which also has The Black Scholes Option Calculator.

Source: TradingToday

The calculator showed me a value of about $7.30 as you can see above for the call options. I then compared it with the real call options pricing value in the US options market which is lower at $6.38 – which might indicate that the current options market is pricing the options too cheaply. Or there is also a possibility that the parameters or assumptions the market is currently using are a little different than the one that I use. But more importantly, through this knowledge, we will be able to know how the options price will behave when certain conditions change such as the interest rate and the volatility – and profit from it. And my personal favourite is through selling the options to get premiums.

In the second part of the article, I am going to share with you guys the limitations of The Black-Scholes Model and how we can take advantage of it.

Disclaimer:

The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Beyond value investing: Timeless Insights from the Late Charlie Munger

Charlie Munger was not just an investment icon and the partner of Warren Buffett. He was also a master of navigating life’s complexities…

WeWork: Would An Investment in WeWork Have Worked Out?

WeWork looming bankruptcy. But would an investment in WeWork have worked out, ever? In this article, we look into the story and …

A Beginner’s Guide to Value Investing in Singapore

Value investing is an investment strategy that seeks to buy stocks that are trading below their intrinsic value. This means that the stock is …

Finding True Wealth: Achieving Peace of Mind and Balance in Life

Tony Robbins says that the quality of your life is directly proportional to the amount of uncertainty you can comfortably live with. The key is …

Mastering Risk vs. Return in Investing | Re-ThinkWealth

Risk and return are two of the most important concepts in investing. The relationship between these two factors is crucial to understanding […]

Here are the key principles of value investing | Re-ThinkWealth

The first value investing principle focuses on a company’s intrinsic value. This means looking beyond its market price and considering its […]

Understanding the Margin of Safety in Value Investing

One of the key concepts of value investing is the margin of safety, which is used to potentially reduce the risk of loss in investing in case of…

The Warren Buffett Approach to Value Investing

Based on the Oxford dictionary, value stocks are shares of a company with solid fundamentals that are priced below those of its peers, based …

8 Tips on Life and Investment from Charlie Munger

Based on the Oxford dictionary, value stocks are shares of a company with solid fundamentals that are priced below those of its peers, based …

The Definition and Important Good Characteristics of Value Stocks

Based on the Oxford dictionary, value stocks are shares of a company with solid fundamentals that are priced below those of its peers, based …

The Ultimate List of Investing Resources in Singapore (Updated 2022)

Being an avid follower of many investments and finance blogs/websites/resources in Singapore, I thought, why not create an article sharing the…

Here Are 3 Powerful Lessons Investors Can Adopt from Roger Federer

“There is no way around the hard work. Embrace it.” – Roger Federer. In investment, it is important to continue “turning the stones” or keep finding […]

Wait, Wait!

I often share insights that I do not share in this blog over at my Facebook page. Don’t forget to like it before you go!

Conquering the Inner Market: Psychology for Investing Success

The concept of “Antifragile” is popularized by Nassim Nicholas Taleb in his book that is aptly named “Antifragile”. What is Antifragile? …

Becoming Antifragile in Stock Investing by Embracing The Volatility

The concept of “Antifragile” is popularized by Nassim Nicholas Taleb in his book that is aptly named “Antifragile”. What is Antifragile? …

Demystifying the S&P 500: A Beginner’s Guide to America’s Stock Market Powerhouse

Have you ever heard of the S&P 500? This mysterious abbreviation often pops up in financial news, leaving many wondering what is it […]

Here’s How to Budget with Value Investing Principles

For a lot of people, budgeting their finances feels like a chore. In this article, I will share my thought process on how we view budgeting …

Beyond value investing: Timeless Insights from the Late Charlie Munger

Charlie Munger was not just an investment icon and the partner of Warren Buffett. He was also a master of navigating life’s complexities…

WeWork: Would An Investment in WeWork Have Worked Out?

WeWork looming bankruptcy. But would an investment in WeWork have worked out, ever? In this article, we look into the story and …

A Beginner’s Guide to Value Investing in Singapore

Value investing is an investment strategy that seeks to buy stocks that are trading below their intrinsic value. This means that the stock is …

Finding True Wealth: Achieving Peace of Mind and Balance in Life

Tony Robbins says that the quality of your life is directly proportional to the amount of uncertainty you can comfortably live with. The key is …