Investing Lessons [Advanced]

Re-examining GameStop as a cigar butt stock investing opportunity

Chris From RWOA.io, Re-ThinkWealth Content Expert

9 November 2017

Earlier this year on 12 May 2017, I wrote an article on GameStop indicating that it is a cigar butt investment play.

You can read the article here.

My average price for GameStop is around US$21.51. And with yesterday’s GameStop closing price at US$17.83, I am now at a 17.16% paper loss.

Update: I averaged down on 10 November 2017 and my average price for GameStop is now around US$20.

So my aim today is to re-examine the good and the bad — weighing the pros and the cons of GameStop as a stock investing opportunity.

GameStop has a market capitalization of about US$1.8B.

Trailing twelve months revenue of about US$8.73B with a quarterly year on year growth of 3.42%.

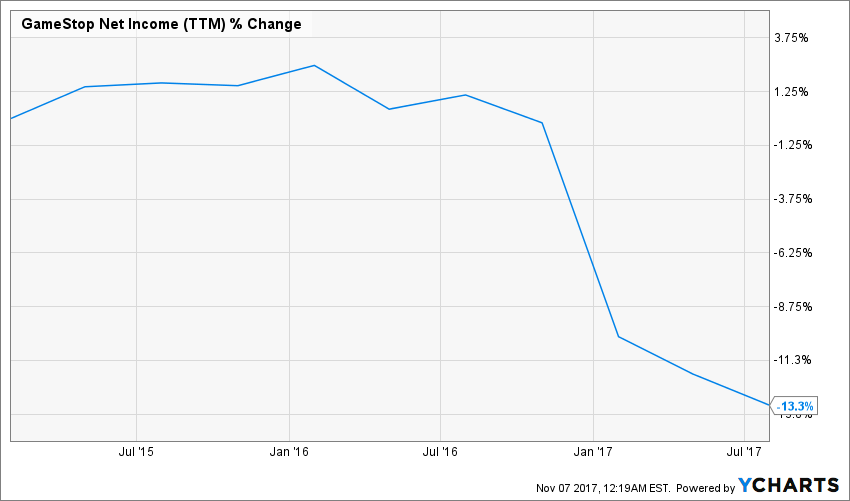

While the revenue seems to be doing alright, their bottom line (net income) is hit badly at US$340.70 M for the trailing twelve months. If you look at it in a basis of three years, their net income has dropped by 13.3%.

The reason for the drop in net income is due to its declining revenue in higher margins business — buying and selling pre-owned games.

In fact, the percentages of its revenue derived from selling physical games has dropped alot in the past years.

GameStop diversification effort to counter the drop in buying and selling pre-owned games/physical games is by opening up more stores selling collectibles and selling technological products (via a partnership with AT&T).

Recently, GameStop announced a new subscription service called the Power Pass which allows people to play as many pre-owned games as they want within six months— provided that they borrow it one at a time — via an upfront payment of US$60. At the end of the period, they are also able to keep the last game they have taken out. It will officially be launched November 19 2017.

Will this new program be a success?

I think that it can work. I mean, personally the notion that I can play as many games as possible for six months at US$60 is very enticing.

But it still does not stop the fact that games are now being distributed more online and that people are having more preference to a game where they can play with friends instead of playing on their own (like what most traditional games is).

We need to remind ourself that GameStop is a product distributor and not a product owner. Naturally as a product distributor, they are paid according to the number of products it sells for other brand owners.

The margin as a product distributor is razor thin as compared to being a product owner.

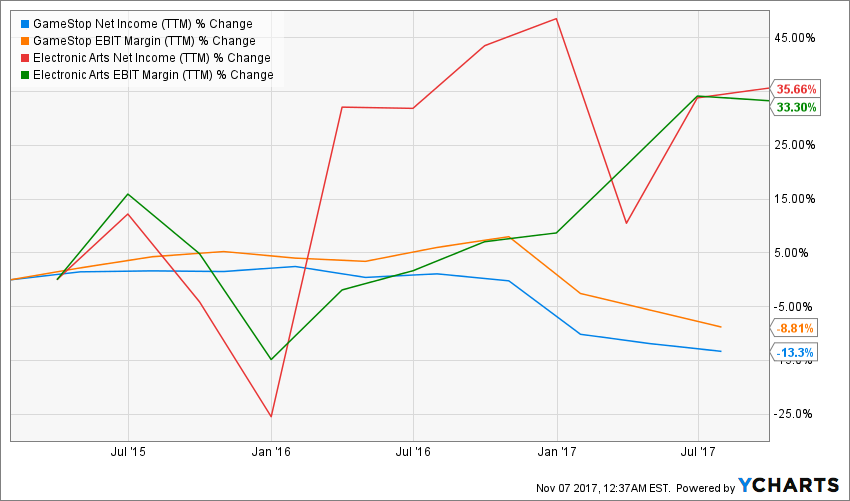

The above chart shows the percentage returns over the past three years for EA [product owner](net income and EBIT margin increase of 35.66% and 33.30% each) and GameStop [product distributor](net income and EBIT margin decrease of 13.3% and 8.81% each).

The reason for GameStop’s under performance (and declining economic moat) is that selling other people’s products gives them razor thin margins — they earn most from buying and selling pre-owned games.

And pre-owned games are in physical forms. But physical games are dying out pretty fast with product owners like EA and Xbox selling their games directly online.

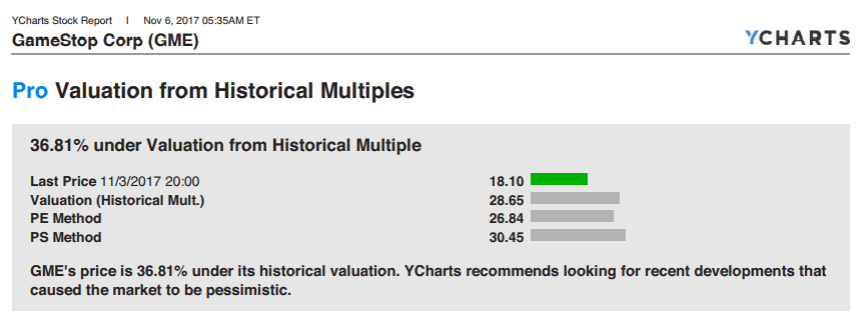

Now, we all know that GameStop is clearly undervalued from a historical perspective. But a stock that is undervalued from a historical perspective does not mean that it is undervalued or overvalued right now.

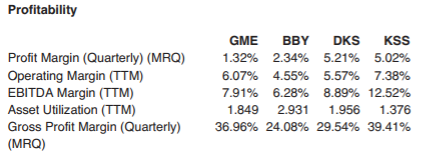

The image above shows again the fact that GameStop has the thinnest profit margin (net income/revenue) as compared to its comparable companies. And it is becoming thinner over the past three years at a -7.8% decline.

Cheap stocks can get cheaper and low pe ratio can turn into high pe ratio once earnings dropped due to the erosion in competitive advantage.

Based on the latest annual report, selling of video games and pre-owned games still have the majority (55.2%) over GameStop’s other revenue sources.

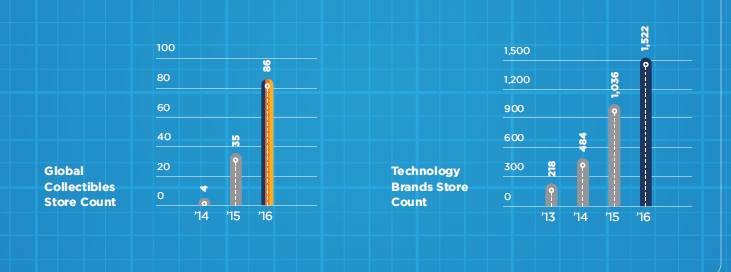

Clearly, GameStop management is aiming to reduce reliance on selling video games and pre-owned games by reducing the store counts for this two — while increasing the store counts (as you can see from the chart above) for Collectibles and Technology business (which is currently still at 5.7% and 9.5% of their overall revenue).

I think that it is a step in the right direction as even though the collectibles and technology business only accounts for 15.2% of GameStop’s revenue for 2016, it accounted for 36.9% of GameStop’s total operating earnings. This means that increasing the store counts for this two business area will definitely increase the revenue contribution and hopefully up its overall operating earnings generated for GameStop.

So the key question is: will the diversification effort of GameStop to grow its non-video gaming business while at the same time monetize its pre-owned games business further using the power pass program work?

My gut feel says yes.

But to what extent will it be successful? Only time will tell.

But for now, I will closely monitor the results (specifically mentions of the Power Pass program and growth for its technology and collectibles business) in the upcoming quarterly earnings report for GameStop on 28 November 2017.

Disclosure: I am long on GameStop (NYSE: GME)

Disclaimer: The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

Want new articles before they get published? Subscribe to our Awesome Community.

And join our Investors Community

A Happy environment for all to share and learn investment knowledge with one another, guided and mentored by Chris Lee Susanto.