Guest Post: Stock Analysis [Advanced]

Sony – Deep Value?

Bryan Wang, an investment analyst with a portfolio of equities focused on ‘best ideas’.

15 June 2018

Editor note: Bryan is a personal friend of mine – and is a genuine value investor. We often have a discussion on some of his investment ideas and Sony is one of them. The analysis is pretty thorough, focusing on the company and its competitive environment (and its future) – with some emphasis on competitors. Have fun reading.

Executive Summary

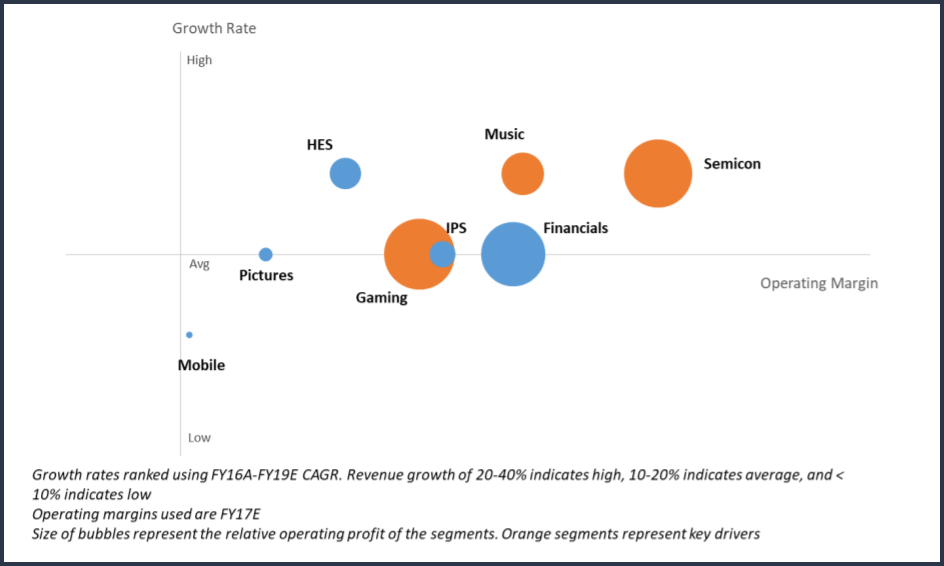

Sony is at an inflection point after years of restructuring. Having shed and restructured loss-making business units, it comfortably exceeded its 2014 medium-term plan to deliver an ROE of 10% and operating profit of JPY500bn in FY17. The company is seeing a number of tailwinds for games, music, and the semiconductor segments, which will drive earnings into the future.

The management of the company has successfully proven their execution skills through delivering on their restructuring plans under ex-CEO Hirai. New CEO Yoshida (ex-CFO) has been Hirai’s right hand man throughout his tenure as CEO (since 2012), and has been credited with pushing through painful structural reforms, such as selling off business units. Their efforts have put Sony into profitability after years of losses from attempting to achieve profitability through scale and market share. The new CEO should be seen as more of the same, with more emphasis on shareholder returns due to his IR background. Succession risk is minimal.

Sony’s gaming and music segments are benefiting from structural tailwinds. In gaming, there are at least three structural shifts that result in an improving business model: i) the shift towards subscription services, ii) downloadable content (DLC) and micro-transactions (MTX) replacing “fire and forget” business models, and iii) shift to digital distribution, effectively making Sony a monopolist in the field. The emergence of music streaming platforms as a viable business model for music companies also provides a strong tailwind for the music segment.

Sony is trading with a huge margin of safety, as investors appear to stay away from the stock, regarding it as uninvestable. However, Sony should be seen in new light now that its business models have firmed up and the company is strongly delivering on profitability. Sony trades at a consolidated forward P/E of 11x, near historical lows (5th percentile is 14.5x). An SOTP analysis suggests that Sony should be valued at $90bn, vs today’s $65bn. The icing on the cake if $10bn of DTAs previously written-off. This is likely to be released into net income in the near-future, providing a clear upside catalyst.

Introduction

Sony is a multi-national conglomerate based in Japan. It was originally a consumer electronics company known for its innovative products (Trinitron TVs, Walkman music players, 3.5” floppy disks etc). However, those years of innovation are likely to be behind the company. Today, it is more of a diversified conglomerate with multiple business interests. Its major interests lie in gaming, semiconductor (CMOS image sensors manufacturing), and music.

Investment Merits

PlayStation ecosystem a cash cow supported by multiple drivers.

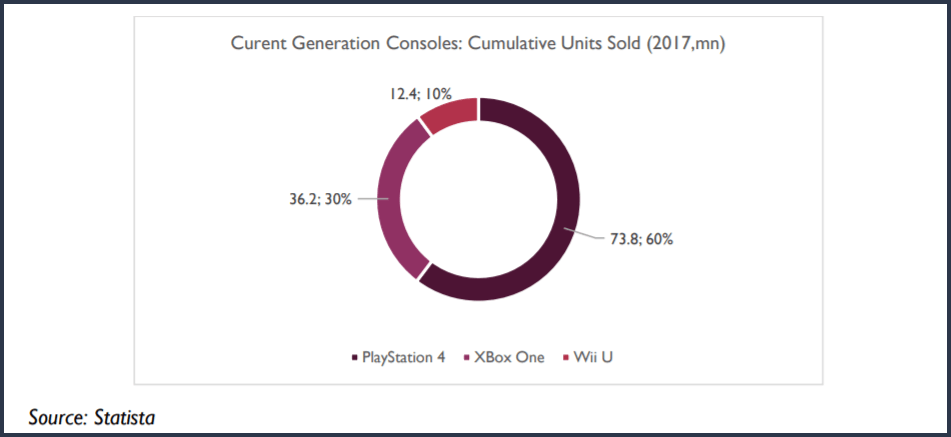

PS4 the market leader among 8th generation consoles.

Sony’s PS4 has an installed base of ~75m, which is 2x that of its nearest competitor, Microsoft’s Xbox One. This market leadership is important as a higher installed base makes for increasing game shipment volume, even as console sales slow.

Source: Sony company filings

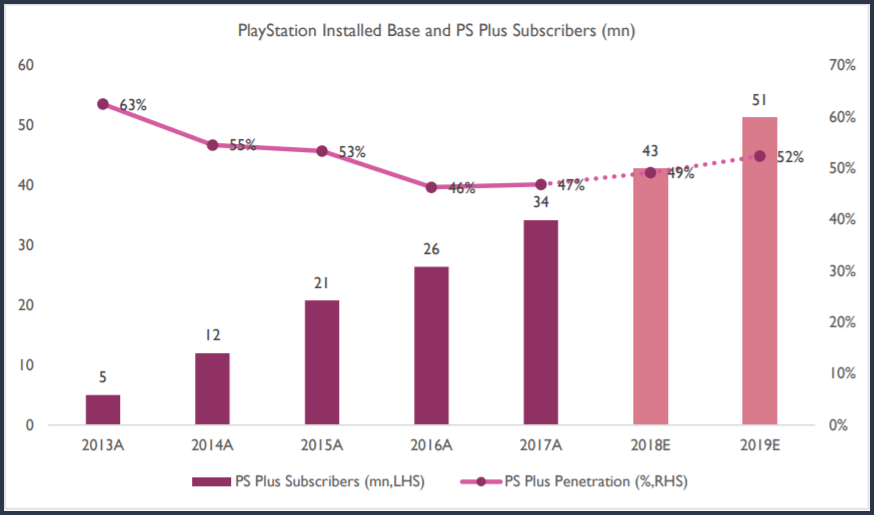

Games-as-a-Service (GaaS) a fundamental shift in game consumption; expect higher recurring revenue

A key driver of the gaming segment is the increasing success of gaming subscription services. Sony has the PS Plus, a subscription service which allows for multiplayer gaming, among others. PS Plus is seen as a core part of the gaming experience, selling for $10 per month. The stickiness of GaaS make for higher quality recurring revenue as the sub base expands:

Source: Sony company filings, Bernstein

Source: Sony company filings, Bernstein

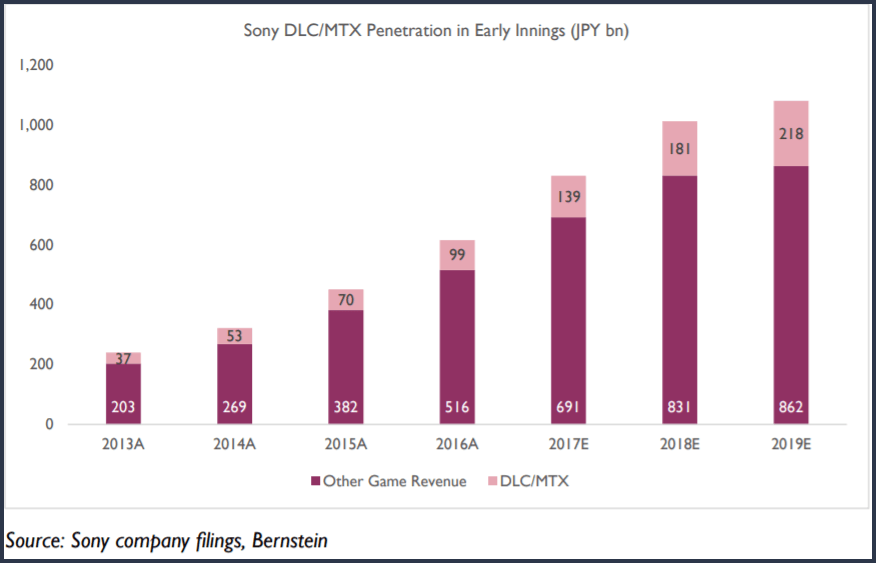

Increasing popularity of downloadable content and microtransactions fundamentally improve business model by increasing recurring revenue, reducing risk

Game developers/publishers used to employ a “fire and forget” model, which saw companies earning revenue upfront for game sale, with no subsequent monetization.

Today, post-sale products and services are commonly embedded into games, increasing game monetization and increasing game lifespans.

Top gaming developers/publishers which have successfully adopted this business model have seen a great improvement in revenue, coming to resemble high-quality compounders. ATVI has already mastered this business model, with over half of revenue coming from such products/services:

Source: Activision Blizzard company filings

Sony’s runway for growth is still in its infancy, with only ~17% of gaming revenue coming from such recurring sources. DLC/MTX contribution is expected to grow at 20-30% a year going forward:

Digital distribution increases value capture and moves Sony towards a monopoly on distribution

Digital distribution has been made possible by increasing broadband penetration and connection speeds.

Today, digital distribution penetration on PC is at 75%. Digital distribution widens Sony’s moat in gaming and increases Sony’s share of the total gaming pie. PC’s Steam has shown how successful digital distribution can be – it has disintermediated the physical retailer, and digital distribution is the main way through which games are sold today.

In contrast, the PS4 ecosystem is lagging. With digital penetration at only 32%, the convergence towards PC’s 75% is driving earnings at Sony, leaving plenty of upside:

Why is this important? Firstly, digital distribution allows Sony to capture a greater portion of the total gaming pie (about 2.5x increase):

Source: Bernstein

Secondly, a move towards digital distribution strengthens Sony’s control of the PS ecosystem, essentially allowing Sony to build a monopoly on game distribution (ATVI and EA are already moving towards a 100% digital model).

A key turning point lies in future consoles – if they do not have a disc drive, it would cement Sony’s distribution monopoly. This allows Sony to reap massive rewards – it earns 30% of each digital sale (video game, downloadable content, and microtransactions), making for a hugely profitable gaming ecosystem.

Music streaming a clear industry driver for Sony Music

Sony one of Big Three record labels

Sony Music Entertainment (SME) is one of the Big Three record labels remaining, with the other two being Universal Music Group (UMG) and Warner Music Group (WMG):

Record labels enjoy a monopoly on supply due to ownership of key IP, benefitting from downstream competition among music streaming platforms

Record labels own the IP rights to recorded music, and are thus the primary beneficiaries of an increase in music consumption as they are the gatekeepers to the industry – music streaming platforms must license tracks (30-40m to be competitive) from them in order to provide a competitive service to consumers. This gives record labels negotiating power, resulting in music streaming platforms paying out a huge amount of revenue to the record labels:

Music streaming giving a new lease of life to the music industry; industry at inflection point

The proliferation of music streaming services has revived the music industry, with the industry growing for the first time in 2005 (below). Streaming is powering the industry ahead, with the music industry growing 6% in 2016:

The engine of growth is music streaming, growing by ~50-60% a year.

This rapid growth means that the increase in streaming revenue more than makes up for the decline in physical and digital music sales. Streaming has two main impacts: i) increases TAM through high streaming penetration, and ii) reduces piracy, which has plagued the industry for years.

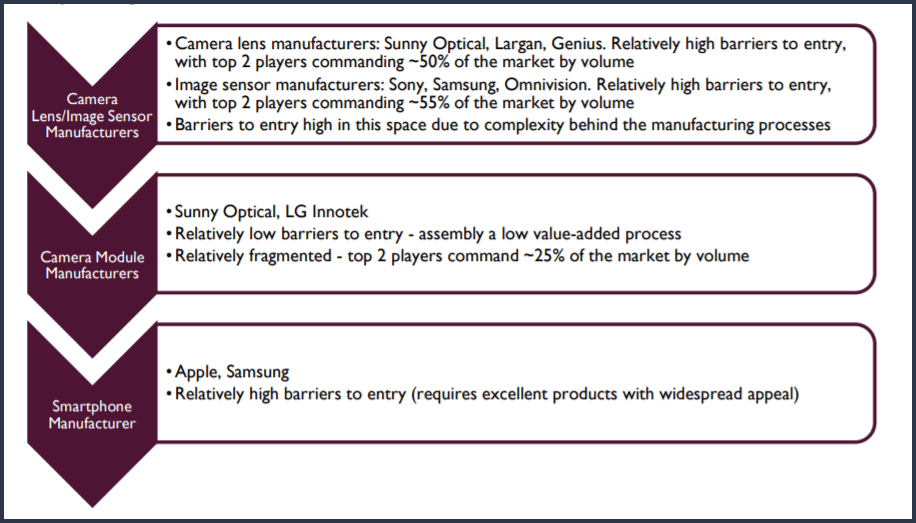

Image Sensor Leadership with Multiple Upside Options

Sony’s CMOS manufacturing operates in an attractive part of the value chain

Sony’s semiconductor division manufactures image sensors for applications ranging from cameras, mobile, and automotive. Most of its products are used for smartphones, with major customers being Apple and Samsung. Sony operates in the upstream segment of the value chain where barriers to entry are high:

Sony as the clear market leader in CMOS manufacturing

Sony is the clear industry leader in this market. While it has only ~30% volume share in the CMOS industry, it has ~50% value share, suggesting that it product mix is tilted towards the premium segment (65% share in 10MP and above).

CMOS applications to enjoy growth from multiple tailwinds

Despite camera and smartphone sales slowing down, image sensor makers enjoy a tailwind from dual-cam adoption in smartphones, with dual-cam penetration forecast to increase from ~15% in 2017 to ~50% in 2020, representing a 3x increase in the smartphone TAM without any smartphone adoption effects.

Other than smartphones, automotive is a long-term growth driver for the image sensor industry, with the number of cameras per vehicle expected to increase from ~0.7 today to 1.5 in 2021. ASP for automotive applications are also ~5x higher than smartphones:

Supportive market dynamics in the near term

The CMOS market is expected to be tight, with supply constrained by i) high capital costs of constructing a fab ($10bn or more), and ii) long lead-time to initial production (can take a few months just for the first batch of image sensors to be ready to ship).

Demand is expected to grow by 12% in 2018, outstripping supply growth of 10%.

Most of the supply growth will be contributed by Sony and Samsung.

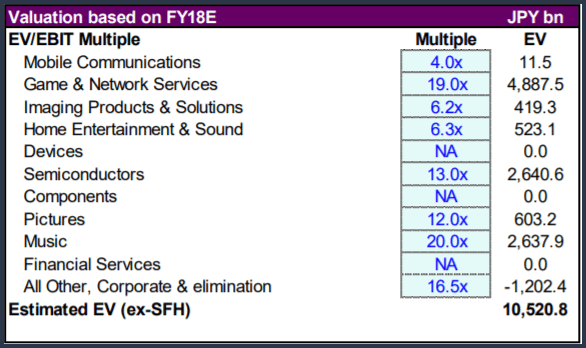

Valuation

SOTP analysis suggests significant upside and margin of safety

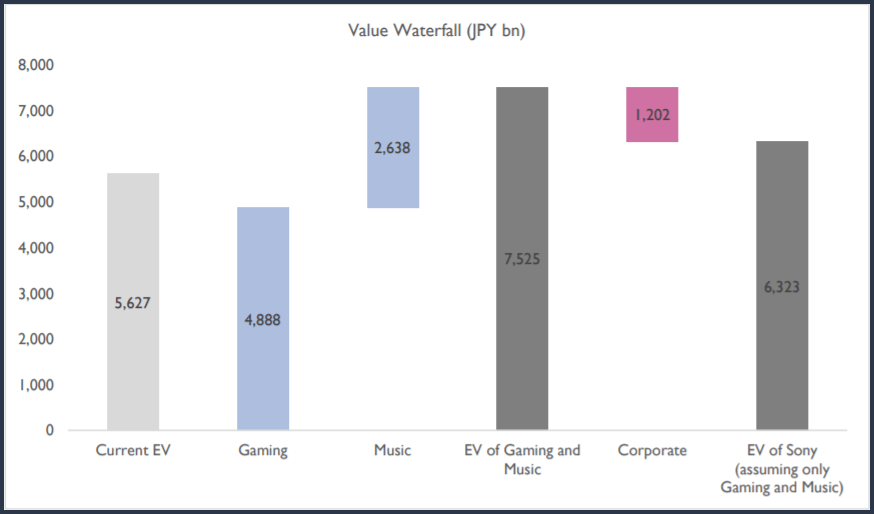

Stripping out SFH, the implied enterprise value of Sony’s underlying businesses is ~$50bn. However, these businesses should be valued at about ~$100bn (below SOTP analysis). Penalizing the valuation with a heavy conglomerate discount still yields substantial upside.

To illustrate the margin of safety, Sony’s current EV (ex-SFH) prices in only the gaming and the music segments – everything else comes free:

Valuation of DTA – $10bn of ‘hidden value’ vs $60bn market cap

Sony hides about $10bn worth of DTAs, which are written off under ‘valuation allowance’, a contra- asset account.

These were written off in the past due to loss-making operations during Sony’s restructuring.

However, Sony today is profitable, and three-year trailing cumulative income has turned positive.

This is significant as it is sufficient evidence to reverse these valuation allowances (Freddie Mac example in 2013) and release them directly into net income, providing for a significant earnings lift.

With $10bn of valuation allowances, Sony does not need to pay taxes for ~5 years.

While the release of valuation allowances does not impact the cash flows of the company, the actual utilization of DTAs itself will reduce cash taxes paid, increasing the value of the company.

Key Investment Risks

Gaming – Slow take up rate of PS5

Sony is near the end of the current PS4 cycle. The next PS cycle brings the risk that Sony loses its market share to Microsoft in the console wars, which will result in ecosystem value destruction (lower sales through the PS Store). In mitigation, Sony appears more in touch with gamers than Microsoft, having pulled off brilliant marketing over the past console cycle to thoroughly secure its dominance.

Cloud gaming currently a way to monetize back catalog, but long-term future impact on consoles uncertain

PS Now service currently allows gamers to stream games on-demand for a $15/month fee. The continual evolution of cloud services should call into question the role of the home console – why is the console needed when all the gamer needs is a sufficiently fast broadband connection, and he can connect to a remote gaming station elsewhere?

Emergence of Spotify as downstream player in music industry; potential future disintermediation of record labels

The power in the music industry currently resides with record labels (i.e. SME, UMG, and WMG), due to their ownership of key IP. This allows the record labels to play off competition at the platform level. However, should platforms like Spotify grow large enough, the dynamics could change – a major warning sign would be Spotify becoming a record label. While unlikely to happen in the short-term, this represents a longer-term risk.

Disclaimer: The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Disclosure: Bryan owns shares of and is long on Sony (NYSE: SNE)

Important: Please read our full disclaimer.

Thank you for your time reading.

Learn more about the new RWOA.io VIM Membership* (limited slots).

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

Remembering Daniel Kahneman: Author of Thinking, Fast and Slow

The world of behavioral economics and psychology lost a giant with the passing of Daniel Kahneman in March …

Ray Dalio’s Gems: My Key Learnings for Life and Success (Updated Regularly)

Ray Dalio is a global macro investor for more than 50 years, who founded Bridgewater Associates out of …

Asbury Automotive: An Undervalued Gem in The Stock Market?

I have owned shares in Asbury Automotive Group, Inc., for about 18 months. Asbury is essentially a collection of …

Recession Fears and Value Investing: Navigating Uncertainty and Building Long-Term Wealth

In the past year, the world has been grappling with a looming recession and high inflation. There is a question of whether we […]

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …