Business Related Article

The Role of Synergies in M&A; Reliable to Warrant a Premium Over Market Value?

Chris Lee Susanto, Founder at Re-ThinkWealth.com

25 May 2018

Today, I want to talk about the role of synergies in M&A. And is it reliable enough for companies to pay a premium over market value because of it?

I for one think that this is a very important topic to discuss for both investors and business people alike. Simply because people tend to be over optimistic of the future and overpay for many things – especially in good times when things are looking all bright and sunny.

I think it should not be the case.

Let’s talk about M&A and synergies first.

Mergers and acquisitions may sound like a big word and something that is very complex – especially for the layman.

But it doesn’t have to be.

What are merger and acquisition?

Merger and acquisition is simply a process of a company buying over or merging with another company to become one new company.

Sounds simple?

A merger usually occurs when two companies have different strengths in which if combined, it would be a 1+1=3 instead of 1+1=2.

The additional 1 happens because of synergies. I will explain more on synergies later on.

If I own company A and you own company B and my company A wants to buy your company B at X price, that is an acquisition offer and your company B is the target. My company A is the buyer.

After the acquisition, there are two possible outcomes:

- Your company B may stay as a separate entity after the acquisition – easier for me to sell off company B at a profit in the future as company A do not have to disintegrate the accounting, operations etc again for the future potential sale.

- Or your company B may come under the umbrella of my company A and no longer exist as a separate entity – would be good in the long run as it is easier to manage and execute potential synergies successfully.

There will be many reasons why a company will choose to want to do M&A, but it seems like a lot of times, they cite synergies as one of the reasons.

What are synergies?

Synergy is simply an immediate advantage – usually, in monetary terms such as cost savings or potential growth opportunities – a company can have by merging or buying over another company.

Based on a research by McKinsey for 1,640 deals from 2010 to 2017, they found that on average, companies have been paying a premium of 40% or more – than their target’s market value. Reason being due to potential synergies from the deal.

So from McKinsey’s research, we would notice that synergies are a reason to pay a premium to buy over or merge with another company. Which also means that potential synergies = premiums over market value = goodwill reflected in the balance sheet of the acquirer.

There are commonly three types of synergies:

1. Cost (eg: from lower headcounts needed to run operations)

2. Revenue (eg: being able to sell more products thus increasing the sales)

3. Financial (eg: higher economies of scale hence lower cost of borrowings).

But how reliable are synergies for people to pay a premium?

First, let’s establish the fact that M&A is important for companies to continuously grow and become a better company over time. So M&A is good.

M&A is also good because it allows the buyer to have a “shortcut” that is less risky than building the business from scratch. After which, the buyer simply integrates the new company into their existing operations.

In good times, you see more companies doing M&A because it is easier to borrow money – easier to do financing activities – banks have more confidence in lending you money.

In bad times, there are less M&A activities, people get retrenched and valuations get lower so sellers usually do not want to sell because of the fear that they are selling at the bottom.

Synergies or potential synergies are commonly used as a reason for a company to pay a premium during M&A.

For example, if there are three companies competing to buy the same company, the company that is willing and can pay more would probably be the company that expects to have the most synergies out of the other three.

These expected synergies would already be reflected in the buyer’s M&A team analysis when offering a buy price. So the accuracy of these financial model is very important for the buyer because expected synergies are after all still “expected”, if it is not realized and not practical, they would be over-paying for the target company.

There are successes and failures across many companies and many sectors in terms of how successful they are in realizing these so-called synergies.

Usually, a company that acquired another company in the industry that is more closely related to their current core business would be more successful than a company that acquires another company in a totally unrelated industry.

Cost synergies such as using lesser manpower or consolidation of facilities for operations would be more easily realized as compared to say, revenue synergies. Simply put, when we have one company, we only need 1 CEO, CFO, marketing department etc than two – so this is an immediate cost reduction.

Revenue synergies, on the other hand, are sales growth opportunities derived from the combination of the two businesses. For example, if I have a company that has a good number of product offerings but no retail distribution channel, another company might want to acquire my company to sell my products via their distribution channel. This would result in higher revenue if executed successfully.

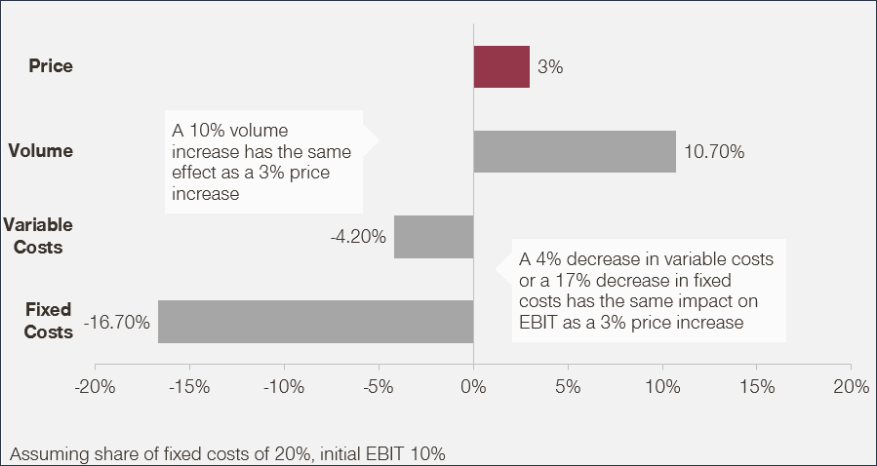

Based on an article by Simon Kucher, it agrees that cost synergy is easier to achieve than revenue synergy but revenue synergy is more powerful than cost synergies. The article mentions that a company would need to reduce its cost using cost synergies by at least 16% to achieve the same margin impact of a 3% price increase through revenue synergies.

Source: Simon Kucher

Although Simon Kucher mentions that revenue synergies are more important than cost synergies, the market and the economy is unpredictable in my opinion. And when it does not happen, the buyer would have already paid that extra premium for nothing.

There are always risks in execution.

But besides that, I think there are 3 factors, in summary, to consider, whether the acquisition warrants a premium and how reliable does it warrant that premium for the acquisition:

- Current market condition – if the market condition is good, a premium is warranted.

- Type of synergies expected to be realized – cost synergies is more reliable than revenue synergies.

- How much extra premium is the buyer paying for the target – my thinking is that the premium that the buyer is paying for the target, should not exceed cost synergies + (revenue+financial or any other synergies x 10%) X 1.2 if the market is doing good and X 1.1 if the market is doing badly.

The above calculation is derived from my own thinking and opinion on what is deemed as a conservative and well-justified amount of premium that buyer should pay for a target.

But in reality, the amount that a company usually pay for a target is much more than that – and that is a problem. Based on the McKinsey’s research, companies commonly pay 40% premium over market value – which I think is way too high and way too optimistic.

That is why so many M&A deals fail based on a Harvard Business Review article – from 2,500 of such deals, more than 60% destroys shareholder value.

So it’s best to follow my thinking that the premium that the buyer should be paying for the target should not exceed cost synergies + (revenue+financial or any other synergies x 10%) X 1.2 if the market is doing good and X 1.1 if the market is doing badly [which will sum up – from my calculation – to definitely be less than 40% of premium over market value].

Otherwise, walk away – if not, the odds are that that M&A deal that you are overpaying, will destroy shareholder’s value.

References:

https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/making-m-and-a-deal-synergies-count

https://www.simon-kucher.com/en/blog/revenue-synergies-key-ma-success

https://www.wallstreetmojo.com/types-of-synergies/

https://hbr.org/2016/05/so-many-ma-deals-fail-because-companies-overlook-this-simple-strategy

Disclaimer: The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Thank you for your time reading. Just want to also take this time to share with you that I have been coaching a number of high-level executives in terms of guiding them and being their main point of contact for important stock discussions in crucial times using value investing and options selling principles with the goal to enhance their overall investment return (capital gain + dividend + options premium). If you are keen to learn more about this service of mine – value investing mentorship, you can WA me now at +65 83946824.

Will The Fed Finally Raise Interest Rate on 16 Dec 2015?

The expectation was based on Chair Janet Yellen's oft-repeated stance that she'd like to see rate rises before the end of 2015. The last time the United States Federal Reserve raised their interest rates was back in 2006, a decade ago. With shares and commodity...

Here Is Everything You Need To Know About The Singapore Savings Bonds

What Are Bonds Bonds are one of the methods for corporations and governments to raise funds. It is a form of borrowing whereby we lend money to the government or corporations and we earn interest on it. We are able to redeem the principal amount but normally there is...

Seven Steps For Starting A Conversation

The seven steps for starting a conversation at a party Give a sincere smile and say Hello Provide a short introduction of who you are and give a firm handshake Listen closely to the person's name - Ask them to repeat it if you did not hear it clearly the first time...

My Week 2 Summary of Yale University Financial Markets Course: The History and Real Impact of Behavioral Finance

The History and The Real Impact of Behavioural Finance People are complex and our financial institutions are designed for real people. This study of behavioural finance started because of the revolution of neuroscience and the fact that the human brain is a...

My Week 1 Summary of Yale University Financial Markets Course: Introduction and Principles of Finance

Recently I embarked on 8 weeks online course from Coursera.org that covers the basics of financial markets. It is taught by Professor Robert J. Shiller, an American Nobel Laureate and also a sterling professor of Economics Yale University. The course will run from the...

2 Key to be SUCCESSFUL in VALUE INVESTING

As the saying goes, "Many roads lead to Rome." The same with value investing, there are many key aspects you can focus on in choosing to buy an undervalued stock. Here is two key to be successful in value investing: Company’s earnings power and whether the stock is...

Sold January 2016 put for KERYX

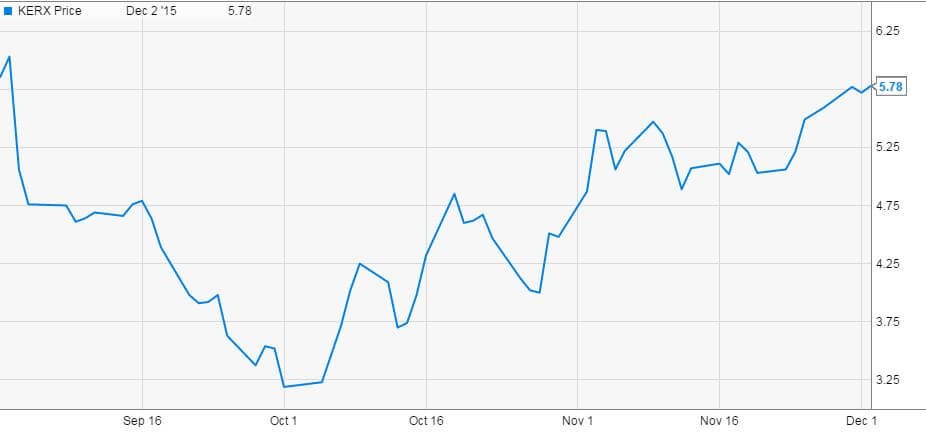

Today i sold January 2016 Put option for Keryx Bio-pharmaceuticals Current Implied Volatility= 98% Margin of safety for stock to fall before being exercised= 30% Strike price=4 USD Premium per contract= 13 USD Commission= 1.4 USD Return in 44 days time=...

The Return on Invested Capital/ROIC Formula | RW Education Series

Return on Invested Capital is an important formula we should look at when analyzing stocks. ROIC, in short, focuses on analyzing the profitability of a company. What is the formula for ROIC?

Return on invested capital […]

Singapore Airlines SIA Retail Bond 2019 – My Thoughts

My take on SIA Retail Bond 2019 where I discussed the pros, cons and overall, my thoughts on it. And whether I would invest in it or not. A few good things to say about it, and some things I thought that people should at least be informed on. Instead of using […]

The Best Value Investing Course in Singapore – VIM Mentorship?

Value Investing Mentorship is created with the goal to be the most effective and exclusive value investing online program. The approach is using twelve exclusive one to one educational lessons that come with assignments to do after each session. With the benefits of […]

Like Investing, Selling Options is Equally Hard. Here’s Why.

Having multiple streams of income is important in my life. In stock investments, most investors I know get their streams of passive income from capital gains and dividends. Getting premiums/cash flow through selling options is another strategy I often use. But all the serious investors will tell you […]