Quick Analysis on FB Stock by Re-ThinkWealth.com (August 2021)

30 August 2021

In this “Quick Analysis” series, I will share my general quick views on different types of companies (you can think of it as a simplified summary). These are just my views and are not meant to be financial advice and you do not have to agree, they are purely for educational purposes only (read our full disclaimer here). If I am vested in the company as of the time of writing, I will also disclose it.

To be updated on all my latest articles, join my free Telegram Channel.

What Does Facebook Do?

Source: Facebook

Is Facebook a social media company?

An advertising company?

Or a chat company?

Or a VR company?

Online shopping company?

Based on their latest 2Q 2021 earnings, they foresee themselves transforming and be known as a metaverse company in the future.

So Facebook wants to be known as a metaverse company!

How will they make money from metaverse? They are looking to make money from selling virtual items in the metaverse along with advertising and other virtual experiences. It will take several years to build this vision of his, based on Mark Zuckerberg.

“A lot of the metaverse experience is going to be around being able to teleport from one experience to another. So being able to basically have your digital goods and your inventory and bring them from place to place, that’s going to be a big investment that people make.” – Mark Zuckerberg

An analyst estimated that Facebook is already spending about $5 billion per year on metaverse-related development.

As of their latest Q2 2021 earnings, they continue to execute well. The daily active users for the Facebook app continue to increase to now 1.908 billion users and the monthly active users are at 2.995 billion users.

Their family of apps daily active people increased to 2.76 billion and monthly active people is at 3.51 billion.

Revenue is the highest it has been in the last 3 years at $29.077 billion in the 2nd quarter of 2021, and so is diluted earnings per share at $3.61.

Cash and equivalents are also very high at $64.08 billion for Q2 2021.

Source: Facebook

The main source of Facebook’s revenue is still advertising, which is up 56% year on year. “Other” sources are gaining traction at $497 million for 2Q 2021.

In the metaverse vision, Mark also foresees that advertising will play a huge role in it (not surprising).

Does Facebook Have A Competitive Advantage?

In my view, Facebook has a clear and durable competitive advantage on three fronts:

1. Network effect

One of the key reasons why Facebook grew so big so fast is due to the “network effect”. It’s a simple principle that the more users Facebook has, the more attractive for others to join as well.

Simply put, Facebook becomes more useful to more people as more people join Facebook and its other apps (WhatsApp, Instagram, etc).

It’s kind of a “winner take all” situation in this social media kind of business.

2. Economies of Scale

Based on Harvard Business Review, Facebook enjoys three advantages over rivals: technological capabilities, economies of scale in its infrastructure, and network effects (our first point). With economies of scale, all of Facebook’s offerings can rely on the same back-end infrastructure system and hence, achieving cost-savings that rivals rarely be able to match.

3. Innovative Management

Facebook’s technological prowess in my view comes from the willingness of the management to fail in the process of innovation and keeping up with the times. There are many examples of companies being disrupted because they were too slow in innovation and therefore succumbs to disruptions from competitors.

Facebook has so far been able to move ahead of the curve (an example is their recent announcements with regards to building a Metaverse company) as well as their continuous investments in building payment and shopping infrastructure in their platforms.

How is The Management Quality of Facebook?

Mark Zuckerberg has proven over time that he is a reliable leader for Facebook.

Reliable not in the sense that there are no controversies. But reliable in the sense that he never fails to continue to try to innovate and be ahead of the curve in terms of what his customers want – and in terms of technological innovation.

“Facebook, it appears, can’t be hurt — not by major ad buyers boycotting its service, not by state and federal investigations, and not even by a pandemic.” – Fortune magazine

Mark has crafted Facebook in a way that there is no single customer concentration. Most of their revenue comes from the small and medium-sized businesses that do advertising on Facebook.

He has also been able to navigate Facebook throughout the different challenges that it has faced over the past few years, privacy issues, state and federal investigations, etc. And in between all those, there are improvements in terms of Facebook’s Oculus Quest 2 offerings and their initiatives on Metaverse.

So overall, the management of FB, in my view has been great. Innovative, flexible and forward looking.

How Is The Valuation Range For Facebook Like?

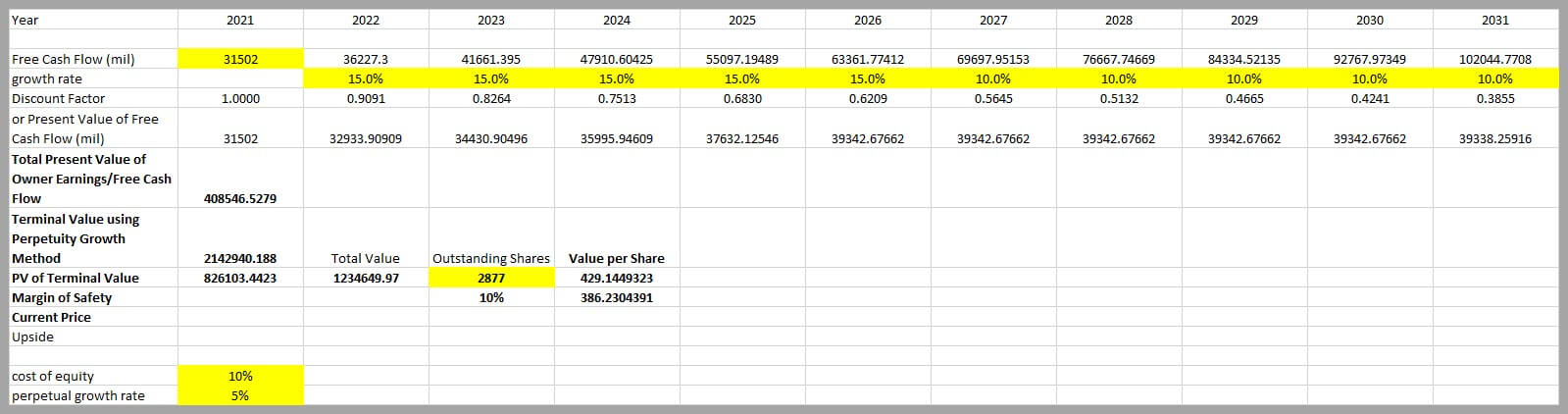

Source: own calculation and model

Facebook’s free cash flow has been steadily going up over the years. Using FB’s latest FCF figure, based on my assumption of a 15% FCF growth rate for the next 5 years followed by 10% for another 5 years before moving towards a perpetual growth rate of 5%, FB fair value is roughly $386.23 after a 10% margin of safety. As of 30 August 2020, FB’s price is at $372.60, which is around its fair valuation based on my assumption.

In Conclusion

I have owned FB for a few years now, first bought it at around $130, $140 region. I view FB as a great company that is in the category of Compounders. A company that continues to evolve and innovate, similar to Microsoft. That is why even in an overvalued region, I would think twice before selling FB.

Some companies are worth paying a premium on and in my view, FB is one of them.

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Disclosure:

I am/we are long FB. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Learned something from this article?

Share it 🙂

Chris Lee Susanto

Founder, investment blogger, full-time investor, and editor of this quality investing x business-like stock investing blog Re-ThinkWealth.com.

Chris started investing in stocks early at age 21 and is a big proponent of business-like stock investing – a mixture of both value and growth investing. He invests in companies where there is value to be found (as long as it is still within his circle of competence), be it a turnaround, depressed, value, or quality growth company (compounders). He either buys the stock outright or he profits through selling put or selling call options – or buying call options (buying and selling options are especially dangerous for those who do not know how to properly execute it).

Some of the places where Chris has been invited to speak or have added value as a mentor or writer includes Singapore Polytechnic, SMU Institute of Innovation and Entrepreneurship (IIE), Dollars and Sense, The New Savvy, Value Walk Blog, Investment Moats, NUS Tembusu College, NUS Investment Society, CGS-CIMB Singapore, Singapore Financial Conference by NTU IIC, The Financial Coconut Podcast, Money FM 89.3 and Internationally in Myanmar.

He is also a practitioner of Transcendental Meditation and Mindfulness practice. He also advocates regular exercise, enough sleep, and nutritious food as part of our lifestyle as an investor.

As of the time of this writing, Chris is focusing on setting up his MAS Licensed Fund with the goal to beat the market over the long run.

Feel free to join his FREE investment telegram channel here to be one of the first to be updated on his new articles.

Don’t Leave First, Read Also:

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

Remembering Daniel Kahneman: Author of Thinking, Fast and Slow

The world of behavioral economics and psychology lost a giant with the passing of Daniel Kahneman in March …

Ray Dalio’s Gems: My Key Learnings for Life and Success (Updated Regularly)

Ray Dalio is a global macro investor for more than 50 years, who founded Bridgewater Associates out of …

Asbury Automotive: An Undervalued Gem in The Stock Market?

I have owned shares in Asbury Automotive Group, Inc., for about 18 months. Asbury is essentially a collection of …

Recession Fears and Value Investing: Navigating Uncertainty and Building Long-Term Wealth

In the past year, the world has been grappling with a looming recession and high inflation. There is a question of whether we […]

Conquering the Inner Market: Psychology for Investing Success

The concept of “Antifragile” is popularized by Nassim Nicholas Taleb in his book that is aptly named “Antifragile”. What is Antifragile? …

Becoming Antifragile in Stock Investing by Embracing The Volatility

The concept of “Antifragile” is popularized by Nassim Nicholas Taleb in his book that is aptly named “Antifragile”. What is Antifragile? …

Demystifying the S&P 500: A Beginner’s Guide to America’s Stock Market Powerhouse

Have you ever heard of the S&P 500? This mysterious abbreviation often pops up in financial news, leaving many wondering what is it […]

Here’s How to Budget with Value Investing Principles

For a lot of people, budgeting their finances feels like a chore. In this article, I will share my thought process on how we view budgeting …