Is SIA Shares Worth Buying? Here Are My Thoughts (August 2020)

22 August 2020

Think About How SIA Was When Times Was “Normal”

Before we got into this COVID-19 mess, SIA is already not a great business to own even when times were “normal.”

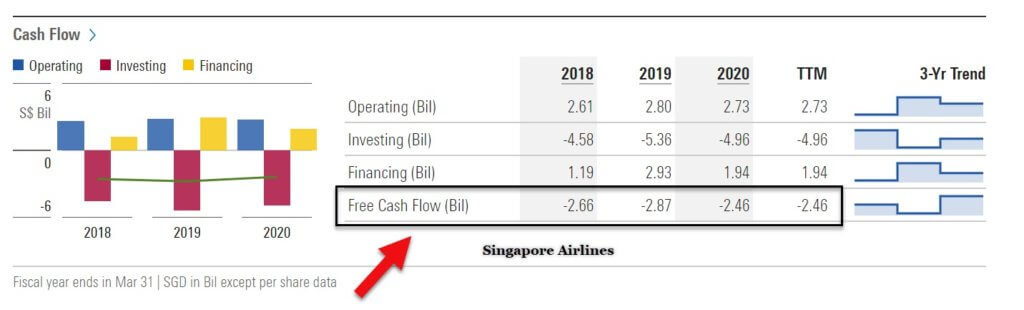

Source: Morningstar

All of us know that the airline business is a very capital intensive business. For SIA, their free cash flow has been negative most of the time in the last five years.

That means that after deducting their operating cash flow for capital expenditures, they are left with negative cash flow.

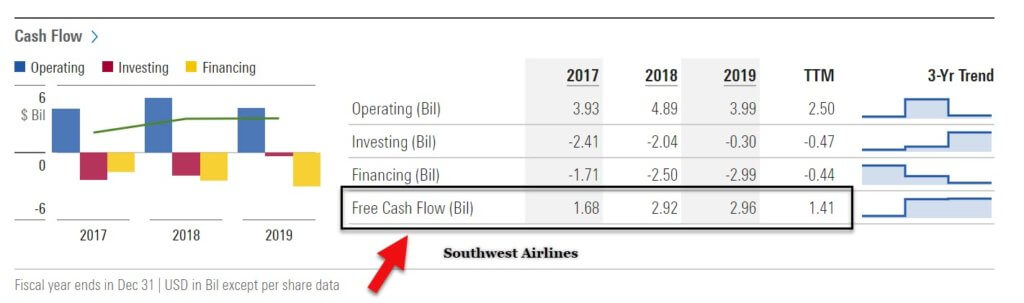

Source: Morningstar

The truth is very few airlines in the world can consistently produce a positive and growing free cash flow. Southwest Airlines, based in the US is an exception, as you can see from the chart above.

Southwest is able to do it because they are able to streamline their operations well – combined with an amazing working culture inside the company.

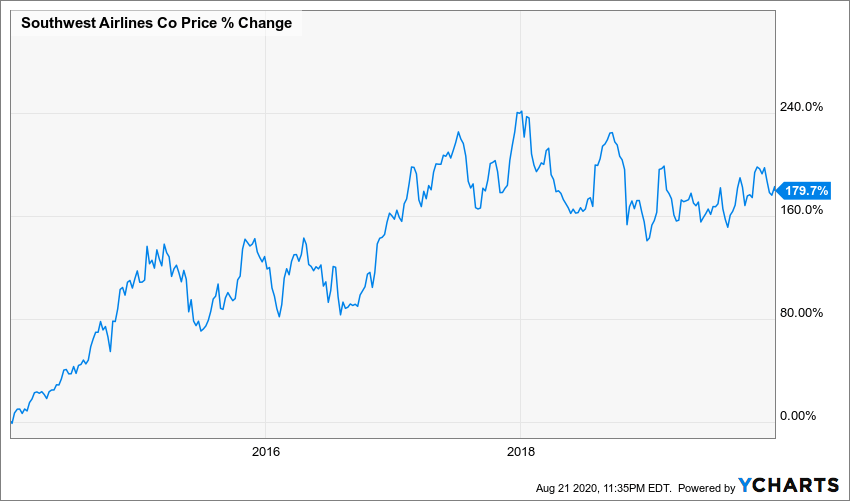

Source: Ycharts

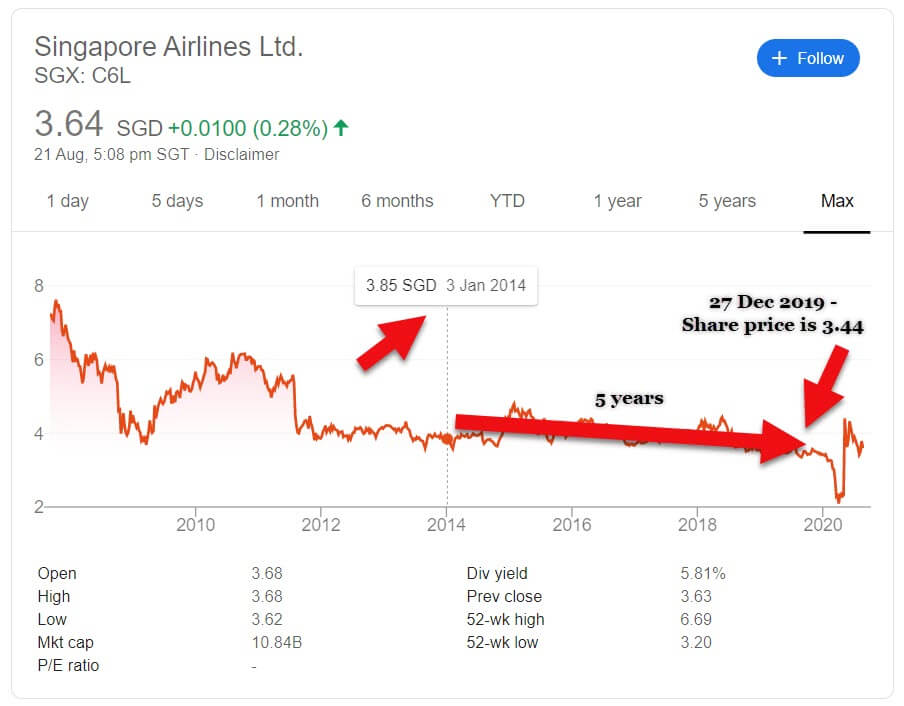

Source: Google

And based on the stock price chart above from 2014-2019, you can see that Southwest has been a better business (and therefore, stock) to own over the last five years as compared to SIA.

Based on the same 5-year period, while Southwest is up 179.7%, SIA is down 10.65%.

Yes, although we cannot compare directly as they operate in different markets but as investors, we still can choose where to allocate our capital.

And as you can see, the stock price reflects the strength of the business that we buy.

My fundamental investing philosophy is always, “if the business does well, the stock price will likely do well too.”

Hence I would say that as an airline business, I’d rather own Southwest as opposed to SIA.

See also: Our free telegram channel. We post daily.

Huge Dilution in A Competitive Industry

SIA is in such a dire state that due to the fund-raising they did, their issued share capital could potentially be diluted by more than 3 times its original share capital.

That simply means that if last time they earn $0.30 per share, and if we assume they manage to reach back to the previous net earnings, its earnings per share will be down to about $0.10 due to the dilution.

That is such a huge potential dilution in which the full effect we will only know maybe in 2021.

Great Branding, Bad Business Economics

Image Source: Wikipedia

SIA is an iconic brand. They are consistently ranked as the best airline brand in Asia.

In fact, in 2018, they were ranked as the most positively perceived brand by Singaporean consumers, based on a study by British-based independent research firm YouGov.

However, it’s economics paints a different picture.

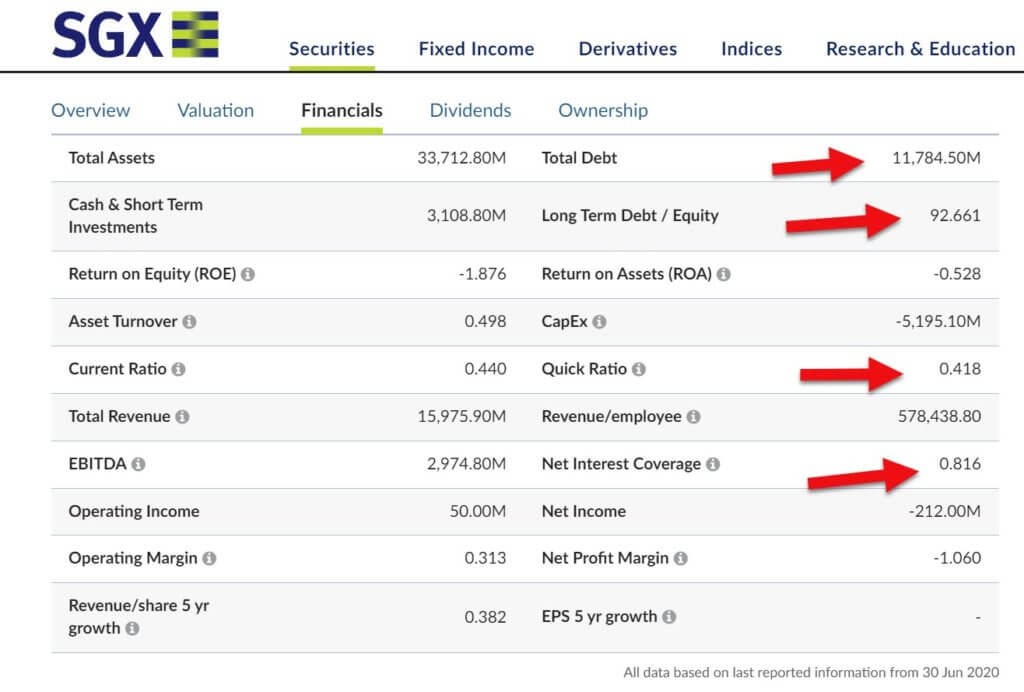

Source: SGX

Based on current data as of 30 June 2020, they are in a dire state. Their debt is more than 92 times as much as it’s equity.

They cannot even cover the current interest with net interest coverage of 0.816.

And their quick ratio is currently below 1. This means that they cannot meet their current short-term obligations with it’s most liquid assets.

Government Support is High for SIA

PM Lee said in April 2020 that the Singapore government is determined to see SIA through the Covid-19 crisis.

PM Lee said that no effort will be spared to ensure that SIA and the aviation sector see through the current crisis because it is a strategic sector.

“SIA has always flown Singapore’s flag high all over the world and made us proud. We will spare no effort to enable it to do so again.”

Share Price Might Go Up Due to Emotional Hype But Might Not Last Due to Lack of Growth

Due to government support, I do not think that SIA will go under.

When the vaccine is found, I think there might be an initial surge for its share price due to a possible return of flying.

But even before COVID-19, SIA is already struggling as a business with high capital expenditure.

Management has not seemed to have found a way to compete effectively in this competitive airline industry filled with other choices.

Also read: The Eight Accounting Fraud or Red Flag Signs To Look Out In Stocks

In Conclusion

The brand alone cannot be constituted as a good investment and a good business. They have to provide a solid return for shareholders.

Airlines like Southwest are able to have positive and growing free cash flow in normal times because they are able to streamline their business very well.

SIA on the other hand would need to innovate its business and give better returns to shareholders if they were to survive and grow.

The airline industry is already so tough, the COVID-19 pandemic would have been a nail in the coffin for SIA if not for government support.

Based on current information and my view as of August 2020, I Would Categorize SIA Stock as a speculation, not investment.

Read next: Kodak Stock is Up Over 1,400% in Two Days. Does It Make Sense?

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Chris Lee Susanto

Founder of the value investing blog Re-ThinkWealth.com (if you type “value investing blog” in Google, his blog is likely the first one). Being a full-time investor himself, Chris knows that he did not beat the S&P 500 return so far (as of the time of this writing) by listening to stock tips. So, when he teaches, he also doesn’t believe in giving stock tips as it is not sustainable for you in the long run. He will teach you how to make your own intelligent decisions with his 4M1S framework. Feel free to also join his free investment telegram channel here.

More from Chris

Re-examining GameStop as a cigar butt stock investing opportunity

Clearly, GameStop management is aiming to reduce reliance on selling video games and pre-owned games by reducing the store counts for this two — while increasing the store counts (as you can see from the chart above) for Collectibles and Technology business (which is currently still at 5.7% and 9.5% of their overall revenue). I think that it is a step in the right direction as even though the collectibles and technology business only accounts for 15.2% of GameStop’s revenue for 2016, it accounted for 36.9% of GameStop’s total […]

Valuation Ratios – The Basics

[…] Not a true cash flow as it excludes CAPEX and working capital. D&A may be added back to net income when calculating cash flows, however, this implicitly assumes that no additional CAPEX is required. A more refined multiple is EV/(EBITDA – CAPEX), though no news source reports this […]

Determining Value: Why Price Is Meaningless, and Multiples are Informative

Investing Lessons [Advanced] Determining Value: Why Price Is Meaningless, and Multiples are Informative Bryan Wang, Re-ThinkWealth Content Expert 23 September 2017 One of the typical responses people give when talking about stocks is..."What's the price?" In the...

10 Mistakes an Investor should Avoid

Investing Lessons [Beginners] 10 Mistakes an Investor should Avoid Benjamin Tan, Content Expert, Re-ThinkWealth 1 September 2017 Every investor has their own investment philosophy and discipline. Each philosophy has its own merit and what is important...

Value Investing And Behavioral Finance

Investing Lessons [Advanced] Value Investing And Behavioral Finance Chris Lee Susanto, Founder and CEO of Re-ThinkWealth 15 July 2017 SUMMARY: Value Investing is inevitably linked to Behavioural Finance Value Investing is a stock methodology practised by many...

![Options Selling Strategy – Wk 4 June 2017 [Keryx Pharmaceuticals (NASDAQ: KERX)]](https://www.re-thinkwealth.com/wp-content/uploads/2017/06/Options-Seliing-400x250.jpg)

Options Selling Strategy – Wk 4 June 2017 [Keryx Pharmaceuticals (NASDAQ: KERX)]

Options Selling Options Selling Strategy – Wk 4 June 2017 [Keryx Pharmaceuticals (NASDAQ: KERX)] Chris Lee Susanto, Founder and CEO, Re-ThinkWealth 24 June 2017 SUMMARY: Options are a form of financial derivatives Options selling strategy have...

Options Selling Strategy – Wk 3 June 2017 (GameStop Inc (NYSE: GME)

Options Selling Options Selling Strategy – Wk 3 June 2017 (GameStop Inc (NYSE: GME) Chris Lee Susanto, Founder and CEO, Re-ThinkWealth 16 June 2017 SUMMARY: Options are a form of financial derivatives Options selling strategy have stocks as...

GameStop Corp (NYSE: GME)– A Cigar Butt Investing Play

Top Articles GameStop Corp (NYSE: GME)– A Cigar Butt Investing Play Chris Lee Susanto, Founder and CEO, Re-ThinkWealth 12 May 2017 SUMMARY: GameStop's valuation is at an all-time low Gross profit margins have been doing well Debt management is good I...

UPDATE: Sold Off All My Stocks In Mobile Telesystems (NYSE: MBT) And This Is What I Learnt From It

Summary Mobile Telesystems (NYSE: MBT) is the biggest stock holdings I had for over two years and it is also the first stock that I bought in my life My absolute gain for this stock is about 34.15% A review of the earnings and revenue growth of MBT indicated an...

![[Edited] Importance Of Knowing When To Sell Your Stocks Cannot Be Understated](https://www.re-thinkwealth.com/wp-content/uploads/2017/03/blur-1853262_640-400x250.jpg)

[Edited] Importance Of Knowing When To Sell Your Stocks Cannot Be Understated

"Knowing when to sell your stocks is as important-- or even more important-- than knowing when to buy them."- Chris Lee Susanto My Experience I have had experiences in buying stocks of good companies that quickly went to two years high price after I bought it earning...

![[Edited] Apple Sued Qualcomm. Here Is Why I Bought It.](https://www.re-thinkwealth.com/wp-content/uploads/2017/02/apple-qualcomm-400x250.png)

[Edited] Apple Sued Qualcomm. Here Is Why I Bought It.

In February 2017 I initiated a position on Qualcomm (NASDAQ: QCOM)-- a few days after it was sued by Apple-- when stock price plunged 12%-- for receiving unreasonable royalty fees via leveraging on their monopoly in the chip making industry. Apple sued Qualcomm and I...

My 10 Biggest Takeaways from Warren Buffett and Peter Lynch

Who is Warren Buffett? Born 1930, Omaha, Nebraska Started managing funds in 1956 with the formation of the Buffett Partnership (dissolved in 1969). Now chairman and major owner, Berkshire Hathaway Inc $1,000 invested with Buffett in 1956 would be worth $ 25,289,750 as...