Is SIA Shares Worth Buying? Here Are My Thoughts (August 2020)

22 August 2020

Think About How SIA Was When Times Was “Normal”

Before we got into this COVID-19 mess, SIA is already not a great business to own even when times were “normal.”

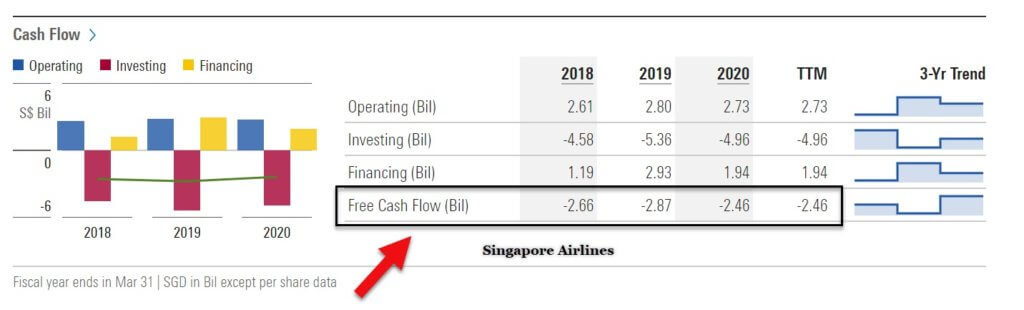

Source: Morningstar

All of us know that the airline business is a very capital intensive business. For SIA, their free cash flow has been negative most of the time in the last five years.

That means that after deducting their operating cash flow for capital expenditures, they are left with negative cash flow.

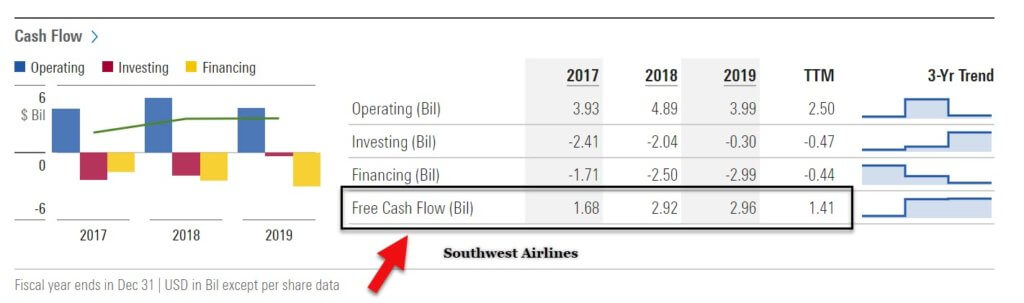

Source: Morningstar

The truth is very few airlines in the world can consistently produce a positive and growing free cash flow. Southwest Airlines, based in the US is an exception, as you can see from the chart above.

Southwest is able to do it because they are able to streamline their operations well – combined with an amazing working culture inside the company.

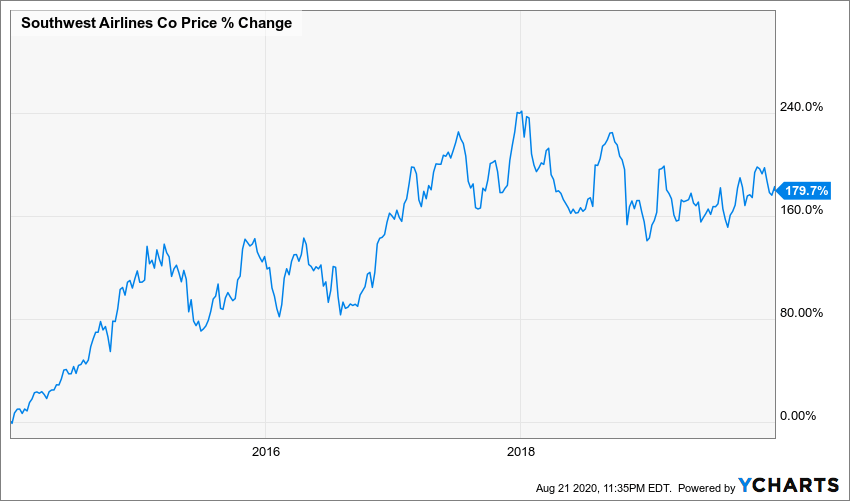

Source: Ycharts

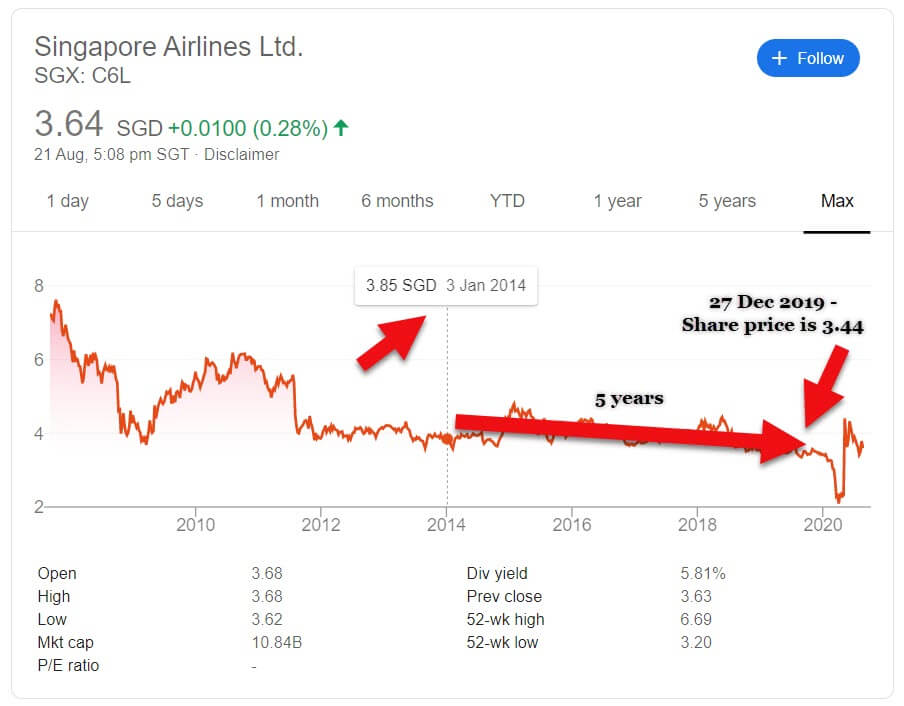

Source: Google

And based on the stock price chart above from 2014-2019, you can see that Southwest has been a better business (and therefore, stock) to own over the last five years as compared to SIA.

Based on the same 5-year period, while Southwest is up 179.7%, SIA is down 10.65%.

Yes, although we cannot compare directly as they operate in different markets but as investors, we still can choose where to allocate our capital.

And as you can see, the stock price reflects the strength of the business that we buy.

My fundamental investing philosophy is always, “if the business does well, the stock price will likely do well too.”

Hence I would say that as an airline business, I’d rather own Southwest as opposed to SIA.

See also: Our free telegram channel. We post daily.

Huge Dilution in A Competitive Industry

SIA is in such a dire state that due to the fund-raising they did, their issued share capital could potentially be diluted by more than 3 times its original share capital.

That simply means that if last time they earn $0.30 per share, and if we assume they manage to reach back to the previous net earnings, its earnings per share will be down to about $0.10 due to the dilution.

That is such a huge potential dilution in which the full effect we will only know maybe in 2021.

Great Branding, Bad Business Economics

Image Source: Wikipedia

SIA is an iconic brand. They are consistently ranked as the best airline brand in Asia.

In fact, in 2018, they were ranked as the most positively perceived brand by Singaporean consumers, based on a study by British-based independent research firm YouGov.

However, it’s economics paints a different picture.

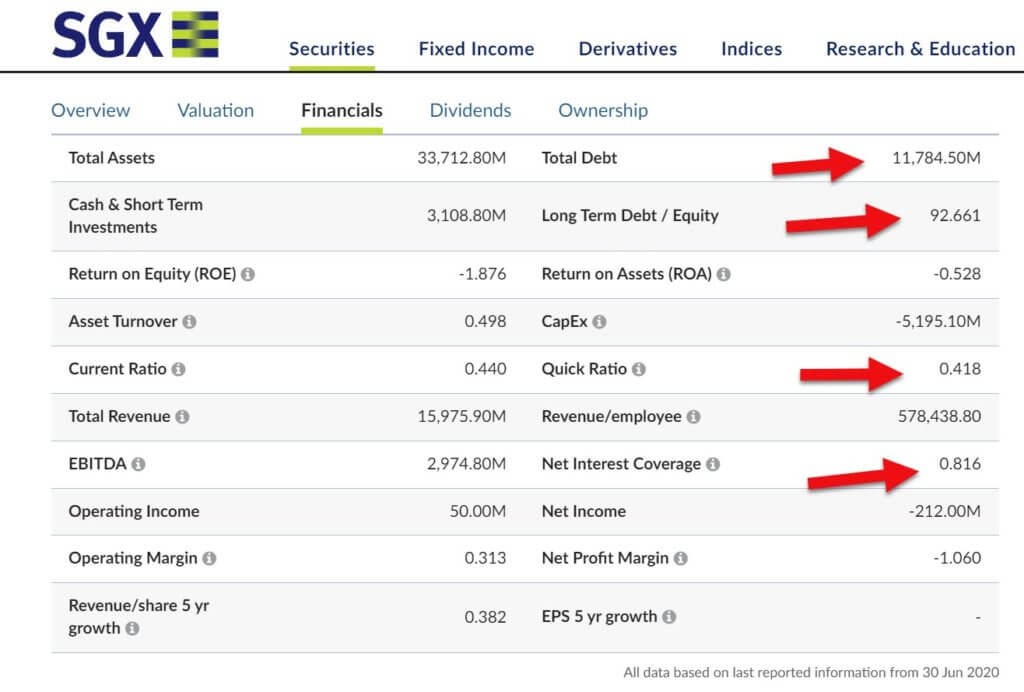

Source: SGX

Based on current data as of 30 June 2020, they are in a dire state. Their debt is more than 92 times as much as it’s equity.

They cannot even cover the current interest with net interest coverage of 0.816.

And their quick ratio is currently below 1. This means that they cannot meet their current short-term obligations with it’s most liquid assets.

Government Support is High for SIA

PM Lee said in April 2020 that the Singapore government is determined to see SIA through the Covid-19 crisis.

PM Lee said that no effort will be spared to ensure that SIA and the aviation sector see through the current crisis because it is a strategic sector.

“SIA has always flown Singapore’s flag high all over the world and made us proud. We will spare no effort to enable it to do so again.”

Share Price Might Go Up Due to Emotional Hype But Might Not Last Due to Lack of Growth

Due to government support, I do not think that SIA will go under.

When the vaccine is found, I think there might be an initial surge for its share price due to a possible return of flying.

But even before COVID-19, SIA is already struggling as a business with high capital expenditure.

Management has not seemed to have found a way to compete effectively in this competitive airline industry filled with other choices.

Also read: The Eight Accounting Fraud or Red Flag Signs To Look Out In Stocks

In Conclusion

The brand alone cannot be constituted as a good investment and a good business. They have to provide a solid return for shareholders.

Airlines like Southwest are able to have positive and growing free cash flow in normal times because they are able to streamline their business very well.

SIA on the other hand would need to innovate its business and give better returns to shareholders if they were to survive and grow.

The airline industry is already so tough, the COVID-19 pandemic would have been a nail in the coffin for SIA if not for government support.

Based on current information and my view as of August 2020, I Would Categorize SIA Stock as a speculation, not investment.

Read next: Kodak Stock is Up Over 1,400% in Two Days. Does It Make Sense?

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Chris Lee Susanto

Founder of the value investing blog Re-ThinkWealth.com (if you type “value investing blog” in Google, his blog is likely the first one). Being a full-time investor himself, Chris knows that he did not beat the S&P 500 return so far (as of the time of this writing) by listening to stock tips. So, when he teaches, he also doesn’t believe in giving stock tips as it is not sustainable for you in the long run. He will teach you how to make your own intelligent decisions with his 4M1S framework. Feel free to also join his free investment telegram channel here.

More from Chris

Quick Analysis on FB Stock by Re-ThinkWealth.com (August 2021)

Is FB a social media company? An advertising company? Or a chat company? Or a VR company? Online […]

Growth or Value Investing? Why Not Both? – Re-ThinkWealth.com

Both value and growth investing have the same goal: which is to find the biggest opportunity or a gap or […]

Will Carnival Corp Stock Sail Higher in 2021? (June 2021)

“Carnival” based on the Oxford dictionary can also be defined as “a traveling funfair or circus.” The name is apt for a […]

Here Are My Quick Analysis on Palantir Technologies Stock (June 2021)

Palantir is a company that provides large organizations with a minimum of $500 million in revenue the ability to […]

High dividend yield, blue-chip stocks, is it safer? | Re-ThinkWealth.com

Many investors love to invest based on dividend yield alone. They think that dividend stocks are safe, but are all of […]

![The Best Investors And Money Managers of All Time [Ultimate List]](https://www.re-thinkwealth.com/wp-content/uploads/2021/05/warren-buffett-400x250.jpg)

The Best Investors And Money Managers of All Time [Ultimate List]

The purpose of this article is to compile a list of some of the worlds greatest investors and money managers. We will also […]

How to Invest Like Chamath Palihapitiya

Who is Chamath Palihapitiya? Chamath is a former Facebook executive who became a venture investor. How to invest like Chamath […]

8 Practical Way For Stock Investors To Be Emotionally Intelligent

Scientists have discovered that emotions are generally caused by our own thoughts. That means that two people in the same situation […]

Here Are The Daily Routine That Has Helped Me As A Stock Investor

For stock investors, I am a firm believer in having an optimized routine that supports us emotionally and rationally – so we can hopefully […]

Here’s My Investment Outlook for 2021 (Is It A Year of Recovery?)

2020 has been another great year for my portfolio. My portfolio is up around 81.24% for the year compared to the S&P 500 total […]

Year in Review: The 20 Most Popular Re-ThinkWealth Articles of 2020

20. Does Warren Buffett Invest In Options? Yes, But It’s Not What You Think Most people will not associate The Oracle of Omaha […]

Does Warren Buffett Invest In Options? Yes, But It’s Not What You Think

Options, Weapon of Mass Destruction? Most people will not associate The Oracle of Omaha with options. Because after all, options are […]