Reflections

Qualcomm Will Not Supply Apple’s 2018 iPhones – And That is Okay (Q3 2018 Results)

Chris Lee Susanto, Founder at Re-ThinkWealth.com

26 July 2018

Qualcomm is the company that supplies phone makers like Samsung, Xiaomi, Huawei, Apple chips so that their phone can be a “smartphone.” Different chip suppliers will have different chips. And just by having a different chip, the performance of the phone can vary greatly.

I am vested in Qualcomm since 24 January 2018 at an average price of about $53.

Here are the facts from their quarter 3 2018 earnings call:

EPS $1.01 beats by $0.30, Revenue $5.6B beats by $410M (+5.7% yoy).

“In QTL, our third quarter results reflect a $500 million payment from the other licensee that is in dispute with us. This is a partial payment made while the negotiations continue for past royalties due going back to the third quarter of fiscal 2017.”

“Non-GAAP EPS of $1.01 was $0.31 above the $0.70 midpoint of our guidance range. The partial payment accounted for $0.26, with the remaining $0.05 above the midpoint driven by favorable interest expense, tax rate, and QTL OEM mix during the quarter.”

Qualcomm beats above their $0.70 midpoint guidance range because of the partial payment from a licensee that is in dispute with them. The licensee in dispute starting to pay the payment they owed is a good positive step for Qualcomm in resolving this payment dispute and put it behind them.

“We intend to terminate our agreement to acquire NXP at the end of the day. The decision for us to move forward without NXP was a difficult one. Continued uncertainty overhanging such a large acquisition introduces heightened risk. We weighed that risk against the likelihood of a change in the current geopolitical environment, which we didn’t believe was a high probability outcome in the near future.”

I would have loved for the NXP deal to go through so this is a sad news. But the current macro environment with U.S. and China at loggerheads would not allow it. China was the only regulators that had not approved the NXP Qualcomm deal.

So without the NXP acquisition, Qualcomm used the fund to approve a $30 billion stock repurchase authorization and planned to execute by the end of fiscal 2019. With a market capitalization of only $88.44B as of today, a $30 billion stock repurchase is a 33.90% reduction in share count – a massive boost for current shareholders. And it is worth noting that their repurchases will be funded almost entirely from balance sheet cash so they will not be over-leveraging themselves.

“Our Snapdragon franchise has moved well beyond mobile devices, becoming the leading platform in areas like AR and VR, and is positioned to be a critical enabler in AI and machine learning at the edge.”

“Our industrial IoT product revenues are also growing rapidly and are on track to double this fiscal year versus two years ago. We anticipate our addressable opportunity in the industrial IoT space to grow at approximately a 20% CAGR over the next few years, and we expect to exceed that growth for our industrial IoT revenues.”

“With continued execution on our growth strategy combined with systematic cost discipline and capital return, we are very well positioned to drive shareholder return in fiscal 2019 and beyond. As you can see from our quarterly results, our business continues to perform well, and the timelines we have previously highlighted to resolve our licensing disputes remain unchanged.”

“We are leading the industry to 5G commercialization next year and are pleased to see our OEM partners finalizing their 2019 5G smartphone launch plans. Qualcomm’s chipsets are now the leading 5G development platform of choice for operators, infrastructure suppliers, and smartphone OEMs.”

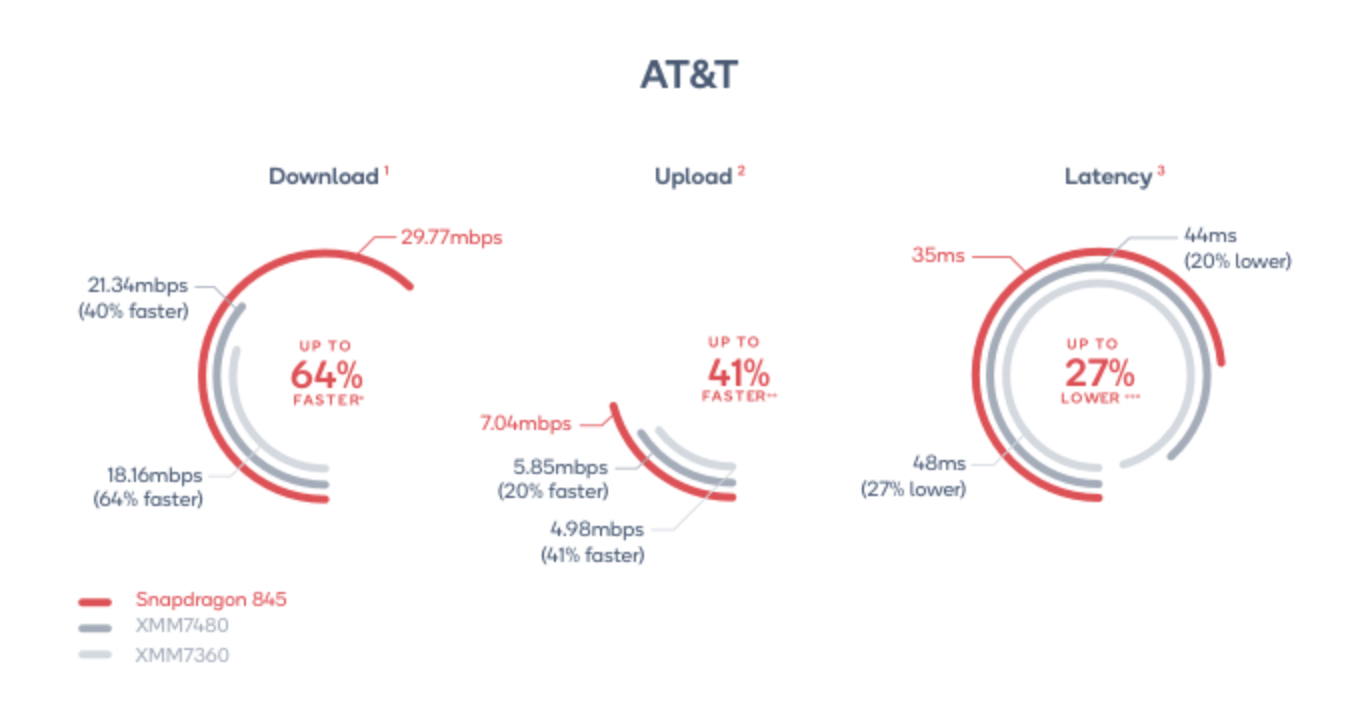

I am confident that Qualcomm will be the leading supplier of chips for the future – with or without Apple. Based on a study by an independent speed test company, Ookla, they revealed that Intel’s modems (the one Apple is currently using) are much slower than Qualcomm’s latest modems as you can see from the image below.

Source: Ookla Speed Test 2018

In conclusion, I believed that the hostile takeover attempt by Broadcom for Qualcomm was a wake-up call for Steve, the CEO of Qualcomm. They have the proven expertise and technology to lead the path into the future of 5G and beyond. They need to be more shareholder-oriented – and they finally had done that with a $30 billion share repurchase program announced. And I feel that it is only a matter of time before Apple goes back to Qualcomm as their chips supplier. Because simply put, Qualcomm has the better technology to give a better user experience.

Disclosure: I own shares of and is long on Qualcomm (NASDAQ: QCOM).

Disclaimer: The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Thank you for reading. 🙂

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

Remembering Daniel Kahneman: Author of Thinking, Fast and Slow

The world of behavioral economics and psychology lost a giant with the passing of Daniel Kahneman in March …

Ray Dalio’s Gems: My Key Learnings for Life and Success (Updated Regularly)

Ray Dalio is a global macro investor for more than 50 years, who founded Bridgewater Associates out of …

Asbury Automotive: An Undervalued Gem in The Stock Market?

I have owned shares in Asbury Automotive Group, Inc., for about 18 months. Asbury is essentially a collection of …

Recession Fears and Value Investing: Navigating Uncertainty and Building Long-Term Wealth

In the past year, the world has been grappling with a looming recession and high inflation. There is a question of whether we […]

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …