Reflections

Qualcomm Will Not Supply Apple’s 2018 iPhones – And That is Okay (Q3 2018 Results)

Chris Lee Susanto, Founder at Re-ThinkWealth.com

26 July 2018

Qualcomm is the company that supplies phone makers like Samsung, Xiaomi, Huawei, Apple chips so that their phone can be a “smartphone.” Different chip suppliers will have different chips. And just by having a different chip, the performance of the phone can vary greatly.

I am vested in Qualcomm since 24 January 2018 at an average price of about $53.

Here are the facts from their quarter 3 2018 earnings call:

EPS $1.01 beats by $0.30, Revenue $5.6B beats by $410M (+5.7% yoy).

“In QTL, our third quarter results reflect a $500 million payment from the other licensee that is in dispute with us. This is a partial payment made while the negotiations continue for past royalties due going back to the third quarter of fiscal 2017.”

“Non-GAAP EPS of $1.01 was $0.31 above the $0.70 midpoint of our guidance range. The partial payment accounted for $0.26, with the remaining $0.05 above the midpoint driven by favorable interest expense, tax rate, and QTL OEM mix during the quarter.”

Qualcomm beats above their $0.70 midpoint guidance range because of the partial payment from a licensee that is in dispute with them. The licensee in dispute starting to pay the payment they owed is a good positive step for Qualcomm in resolving this payment dispute and put it behind them.

“We intend to terminate our agreement to acquire NXP at the end of the day. The decision for us to move forward without NXP was a difficult one. Continued uncertainty overhanging such a large acquisition introduces heightened risk. We weighed that risk against the likelihood of a change in the current geopolitical environment, which we didn’t believe was a high probability outcome in the near future.”

I would have loved for the NXP deal to go through so this is a sad news. But the current macro environment with U.S. and China at loggerheads would not allow it. China was the only regulators that had not approved the NXP Qualcomm deal.

So without the NXP acquisition, Qualcomm used the fund to approve a $30 billion stock repurchase authorization and planned to execute by the end of fiscal 2019. With a market capitalization of only $88.44B as of today, a $30 billion stock repurchase is a 33.90% reduction in share count – a massive boost for current shareholders. And it is worth noting that their repurchases will be funded almost entirely from balance sheet cash so they will not be over-leveraging themselves.

“Our Snapdragon franchise has moved well beyond mobile devices, becoming the leading platform in areas like AR and VR, and is positioned to be a critical enabler in AI and machine learning at the edge.”

“Our industrial IoT product revenues are also growing rapidly and are on track to double this fiscal year versus two years ago. We anticipate our addressable opportunity in the industrial IoT space to grow at approximately a 20% CAGR over the next few years, and we expect to exceed that growth for our industrial IoT revenues.”

“With continued execution on our growth strategy combined with systematic cost discipline and capital return, we are very well positioned to drive shareholder return in fiscal 2019 and beyond. As you can see from our quarterly results, our business continues to perform well, and the timelines we have previously highlighted to resolve our licensing disputes remain unchanged.”

“We are leading the industry to 5G commercialization next year and are pleased to see our OEM partners finalizing their 2019 5G smartphone launch plans. Qualcomm’s chipsets are now the leading 5G development platform of choice for operators, infrastructure suppliers, and smartphone OEMs.”

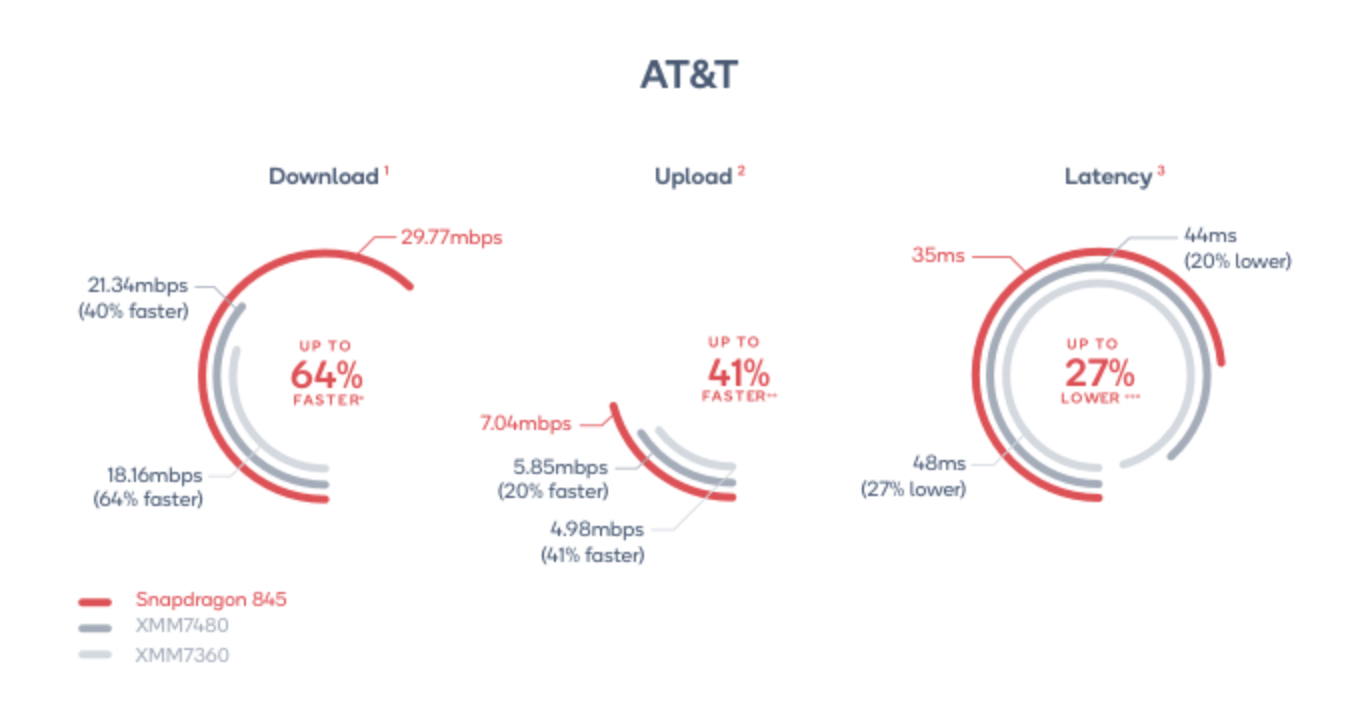

I am confident that Qualcomm will be the leading supplier of chips for the future – with or without Apple. Based on a study by an independent speed test company, Ookla, they revealed that Intel’s modems (the one Apple is currently using) are much slower than Qualcomm’s latest modems as you can see from the image below.

Source: Ookla Speed Test 2018

In conclusion, I believed that the hostile takeover attempt by Broadcom for Qualcomm was a wake-up call for Steve, the CEO of Qualcomm. They have the proven expertise and technology to lead the path into the future of 5G and beyond. They need to be more shareholder-oriented – and they finally had done that with a $30 billion share repurchase program announced. And I feel that it is only a matter of time before Apple goes back to Qualcomm as their chips supplier. Because simply put, Qualcomm has the better technology to give a better user experience.

Disclosure: I own shares of and is long on Qualcomm (NASDAQ: QCOM).

Disclaimer: The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Thank you for reading. 🙂

Is Snowflake (NYSE: SNOW) Worth Investing? Here Are My 5 Takeaways

Snowflake does cloud computing that implements a variable pricing model, which can be at times more attractive than fixed packages […]

Nasdaq Is Officially In A Correction Territory: What Is Next?

The adage that “In the short run, the market is a voting machine but in the long run, it is a weighing machine.” by Benjamin Graham could not be more true over the past few days. As of 9 September 2020, […]

My 3 Thoughts on Yesterday’s Deepest US Market Decline Since June

Yesterday (3 September 2020), the US market had its deepest one day decline since June. The S&P 500 and Nasdaq had their deepest declines since June 11 and for Dow, it was their biggest decline since June 26 […]

Will The Stock Market Crash One More Time in 2020?

My Bet: In 2020, The Stock Market Will Not Crash Again. Yes, it is hard to predict where the stock market is heading in the short term. But my bet with regards to virus-related concern is that I do not think that we will crash again back to March-April Lows in 2020 just because of it […]

Is SIA Shares Worth Buying? Here Are My Thoughts (August 2020)

Think About How SIA Was When Times Was “Normal” Before we got into this COVID-19 mess, SIA is already not a great business to own even when times were “normal.” All of us know that the airline […]

The Eight Accounting Fraud or Red Flag Signs To Look Out In Stocks

In this article, I’d like to share eight signs of potential fraud in our stocks portfolio that we should be careful of. These are eight simple potential warning signs of bad financial reporting or early markers […]

My 5 Key Takeaway From AEM Holdings 1H 2020 Results

3. As of 1H20, Most Earnings Paid Out As Dividends Based on AEM 1H20 reports, their cumulative capital allocation breakdown from 2017 to 1H2020 is as follows: Dividends – 47%, Acquisitions – 25%, Capex – 18%, Buybacks – 10%. It is interesting to note that […]

Kodak Stock is Up Over 1,400% in Two Days. Does It Make Sense?

Eastman Kodak Company (NYSE: KODK) opened at $2.15 (Monday) on July 27, 2020, and closed at $33.20 (Wednesday) by 29 July 2020. That is a 1,444.19% increase over a two day period. In this article, I am going to give you some background on the Kodak company, the reason […]

STI ETF: Historical Returns, Dividends, Investment Prospects in 2022

STI ETF or Straits Times Index is the index of the top 30 companies listed in […]

GoTo IPO: Will I Invest in The New Company of Gojek and Tokopedia?

GoTo IPO date is on 11 April 2022. Analyzing their prospectus, will I invest in […]

Russia-Ukraine War: How to Keep a Level Head And Invest Long Term

In this article, I will be sharing my opinion on how to keep a level head and invest […]

I Recently Got Covid. Here’s How It Affected My Investment Outlook

In this article, I will be sharing my journey on recently having acquired COVID-19 and […]