My Stock Updates

Here’s My Thoughts on GameStop’s Q417 Earnings Results (Released 28/3/2018)

Chris Lee Susanto, Editor in Chief at Re-ThinkWealth

29 March 2018

Focusing on Fundamentals via Improving The 3 Core Businesses:

The above statement is the general takeaway on the direction GameStop is going in the upcoming year. They are resilient – despite the secular decline of their industry. They are tough and pragmatic to say the least and I like what they are planning for the upcoming year. The new CEO is practical and they managed to stay true to what they are good at. And the direction of targetting different demographics such as the focus on families will drive certain growth into the future too (with big retailers such as Toys R Us closing down stores). The improvement in omnichannel sales and the focus on investing more into that is a good sign as well. They are still negotiating with AT&T and seems confident of the outcome of a win-win solution (CEO reiterated numerous times throughout the call that AT&T is a good partner to GameStop – and is still one of the pillar driving growth under technology business).

The facts from listening to their earnings call (you can do the same at http://news.gamestop.com/events-and-presentations under webcast):

- The CEO plans to focus on fundamentals and operational excellence moving forward – fixing and focusing on current businesses (collectibles, video games, and technology) and expand on customer demographics (to moms and families and casual consumers)

- Get a better value proposition for their loyalty programs that focus on collectibles and other products

- Planning to invest more in omnichannel experience (order in store and have it sent to your house and vice versa)

- Increase average transactions value through warranties and accessories (and other relevant operating expenses)

- More promotional activities designed for trade-ins on pre-owned (increase trade and reservations awareness)

- Converting their stores to hybrids and more organized and friendly

- Mentioned that AT&T is a good partner for them – and the focus is more on a win-win solution. Still in negotiation and is confident to get something that produces a longer-term result

- SG&A reduction is part of their strategy (one of the fundamentals to focus on reducing costs – be frugal but not cheap to improve value to shareholders)

- The high increase in inventory is to support the sales of the growth in collectibles and hardware

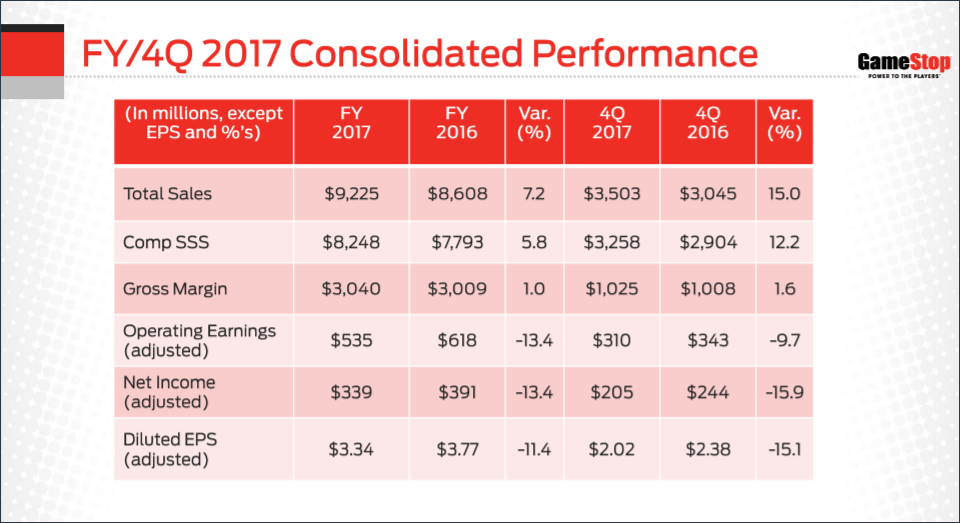

Here are the facts for GameStop based on yesterday’s earnings report (28/3/2018) on Q4 earnings:

- Posted adjusted earnings of $2.02 per share and revenue of $3.5 B – 15% more than a year ago.

- New hardware sales increased by 44.8% due to continued strength in Nintendo Switch sales

- Comparable store sales growth is 12.2%

- Digital sales and non-GAAP digital receipts increased 41% and 15.1% respectively

- Collectibles sales increased 22.8%

- Omnichannel sales increased 24.8%

Here are the facts for GameStop based on yesterday’s earnings report (28/3/2018) on FY2017 earnings:

- Total global sales increased 7.2% to $9.2B

- Comparable store sales increased 5.8%

- New hardware sales increased 28.3%

- Collectible sales increased 28.8%

- Omnichannel sales increased 48.9%

The management prediction for FY 2018:

- Total sales will fall 2-6%

- Same-store sales will be flat to -5%

- Income tax rate at 26-27%

- Adjusted Non-GAAP EPS $3-$3.35

More results comparisons based on FY and quarter basis:

Source: GameStop Earnings Call

Closing Thoughts

Despite the increase in sales and the beat in earnings from analyst estimates, their profits are still down 11.4% year on year basis on the adjusted diluted EPS portion (from $3.77 to $3.34). However, $3.34 is near the top of the management guidance for FY2017 – and the focus on improving the trade awareness whereby GameStop has the most margin in, can prove to be useful. Especially with the fact that Nintendo Switch has little storage space inside and does not support much online game downloads – so buying Nintendo Switch would require users to buy more physical games and accessories in the future – this supports both trade in and further sales for GameStop. Do remember, Nintendo Switch plays a gargantuan role in the comparable store sales increase for the last 1 year.

My average cost for GameStop now is $17.23 excluding the dividends and options premium I gained. Including dividends and premiums, my average cost is about $16+. I am satisfied with the earnings result and I wish the management good execution for the year ahead. Meanwhile, I will still hold on – but I will sell when a more attractive investment opportunity on a price to value ratio shows up.

My other articles on GameStop:

Disclaimer: The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Thank you for your time reading.

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

Why Investing is Not About Predicting, but Positioning

InvestingWhy Investing is Not About Predicting, but PositioningBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipIn a world where everyone is obsessed with the noise of stock price fluctuations, quarterly earnings beat or macro economic...

Strategic Positioning: How to Win Without Predicting the Future

ReflectionsStrategic Positioning: How to Win Without Predicting the FutureBy Chris Susanto,Editor at Re-ThinkWealthFounder at Value Investing MentorshipMost people treat their lives like a lottery ticket. They pick a number—a specific career goal, a dream house, a...

VIM Introduces New Logo & Reflects on It’s Transformation over the Years

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …

My Reflections and Learnings on My 31st Birthday | Re-ThinkWealth

I just turned 31 recently and usually on my birthdays, it’s always feels like the right time to reflect on my …