Is SIA Shares Worth Buying? Here Are My Thoughts (August 2020)

22 August 2020

Think About How SIA Was When Times Was “Normal”

Before we got into this COVID-19 mess, SIA is already not a great business to own even when times were “normal.”

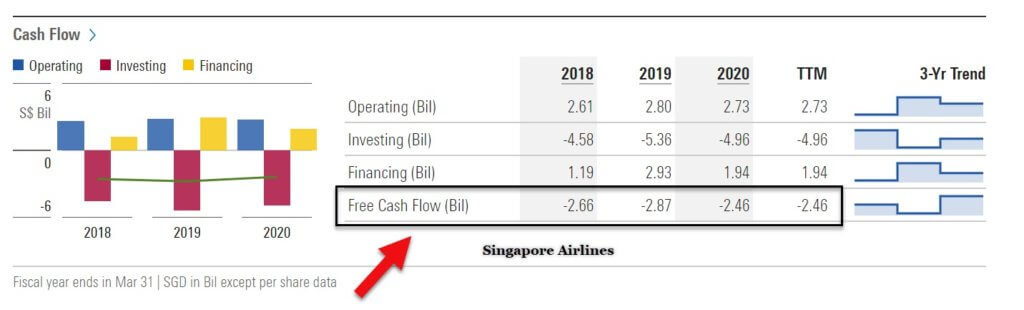

Source: Morningstar

All of us know that the airline business is a very capital intensive business. For SIA, their free cash flow has been negative most of the time in the last five years.

That means that after deducting their operating cash flow for capital expenditures, they are left with negative cash flow.

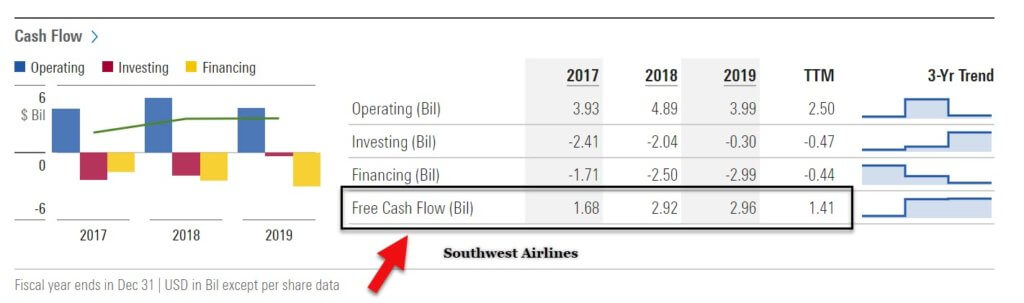

Source: Morningstar

The truth is very few airlines in the world can consistently produce a positive and growing free cash flow. Southwest Airlines, based in the US is an exception, as you can see from the chart above.

Southwest is able to do it because they are able to streamline their operations well – combined with an amazing working culture inside the company.

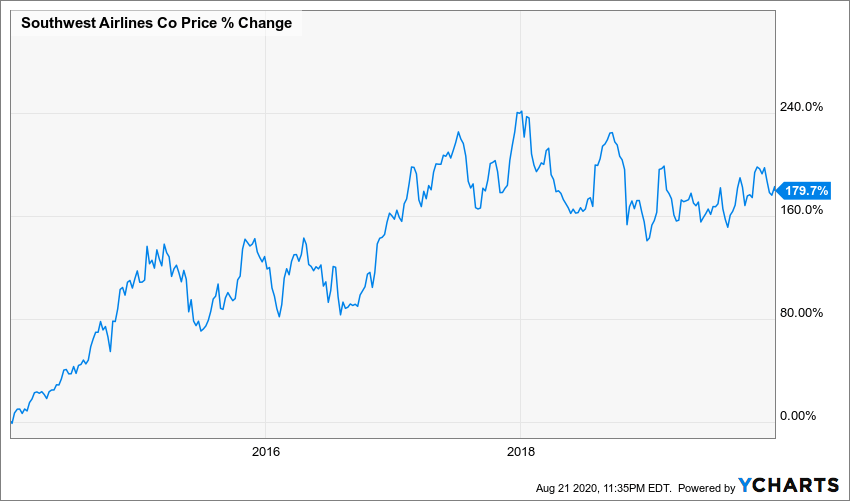

Source: Ycharts

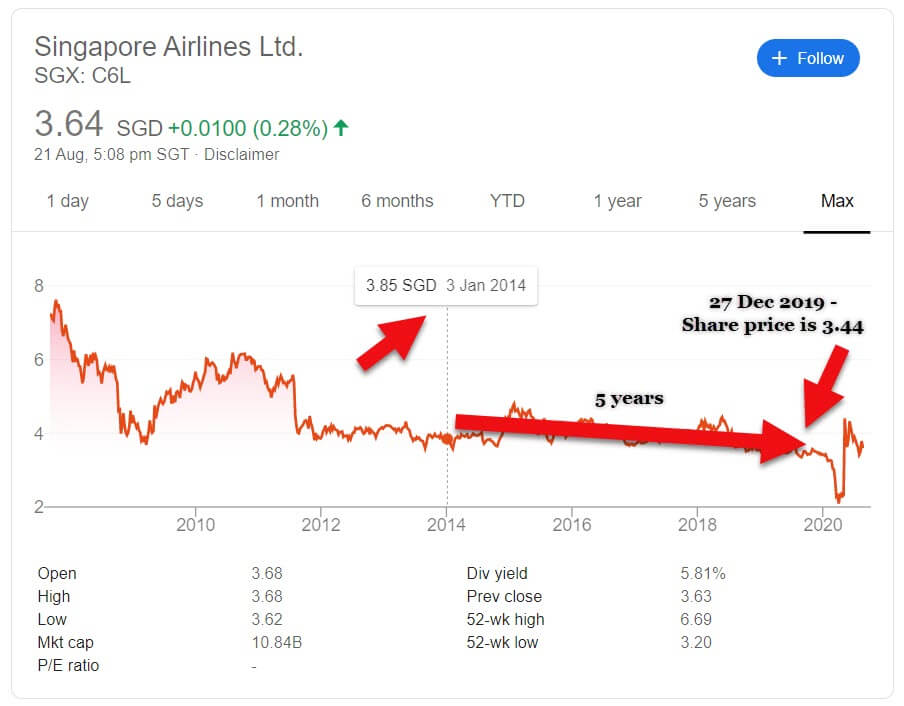

Source: Google

And based on the stock price chart above from 2014-2019, you can see that Southwest has been a better business (and therefore, stock) to own over the last five years as compared to SIA.

Based on the same 5-year period, while Southwest is up 179.7%, SIA is down 10.65%.

Yes, although we cannot compare directly as they operate in different markets but as investors, we still can choose where to allocate our capital.

And as you can see, the stock price reflects the strength of the business that we buy.

My fundamental investing philosophy is always, “if the business does well, the stock price will likely do well too.”

Hence I would say that as an airline business, I’d rather own Southwest as opposed to SIA.

See also: Our free telegram channel. We post daily.

Huge Dilution in A Competitive Industry

SIA is in such a dire state that due to the fund-raising they did, their issued share capital could potentially be diluted by more than 3 times its original share capital.

That simply means that if last time they earn $0.30 per share, and if we assume they manage to reach back to the previous net earnings, its earnings per share will be down to about $0.10 due to the dilution.

That is such a huge potential dilution in which the full effect we will only know maybe in 2021.

Great Branding, Bad Business Economics

Image Source: Wikipedia

SIA is an iconic brand. They are consistently ranked as the best airline brand in Asia.

In fact, in 2018, they were ranked as the most positively perceived brand by Singaporean consumers, based on a study by British-based independent research firm YouGov.

However, it’s economics paints a different picture.

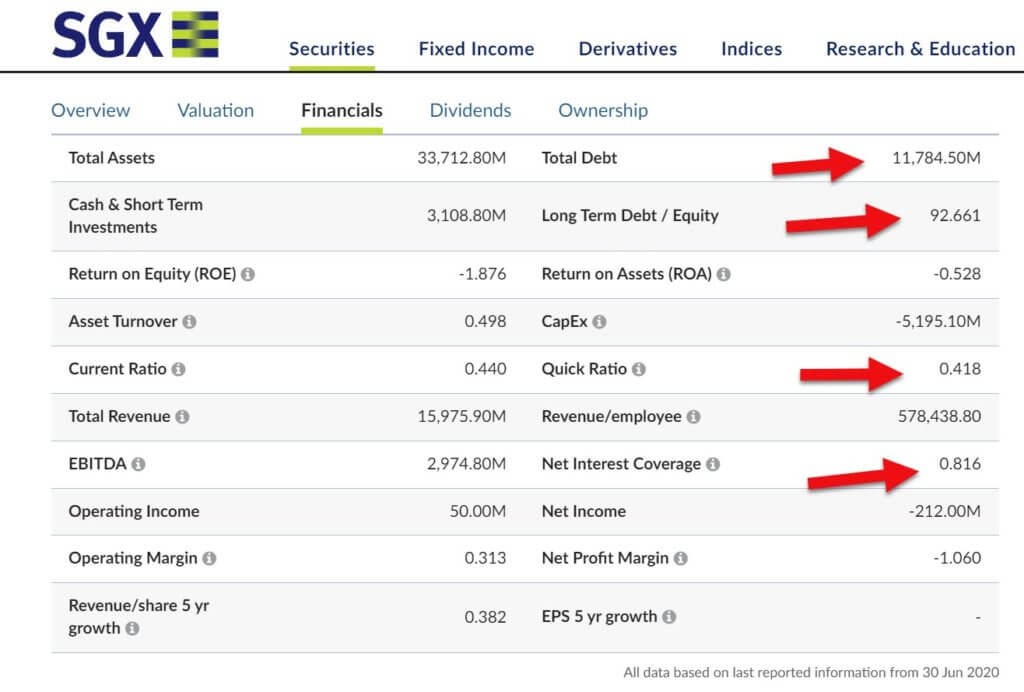

Source: SGX

Based on current data as of 30 June 2020, they are in a dire state. Their debt is more than 92 times as much as it’s equity.

They cannot even cover the current interest with net interest coverage of 0.816.

And their quick ratio is currently below 1. This means that they cannot meet their current short-term obligations with it’s most liquid assets.

Government Support is High for SIA

PM Lee said in April 2020 that the Singapore government is determined to see SIA through the Covid-19 crisis.

PM Lee said that no effort will be spared to ensure that SIA and the aviation sector see through the current crisis because it is a strategic sector.

“SIA has always flown Singapore’s flag high all over the world and made us proud. We will spare no effort to enable it to do so again.”

Share Price Might Go Up Due to Emotional Hype But Might Not Last Due to Lack of Growth

Due to government support, I do not think that SIA will go under.

When the vaccine is found, I think there might be an initial surge for its share price due to a possible return of flying.

But even before COVID-19, SIA is already struggling as a business with high capital expenditure.

Management has not seemed to have found a way to compete effectively in this competitive airline industry filled with other choices.

Also read: The Eight Accounting Fraud or Red Flag Signs To Look Out In Stocks

In Conclusion

The brand alone cannot be constituted as a good investment and a good business. They have to provide a solid return for shareholders.

Airlines like Southwest are able to have positive and growing free cash flow in normal times because they are able to streamline their business very well.

SIA on the other hand would need to innovate its business and give better returns to shareholders if they were to survive and grow.

The airline industry is already so tough, the COVID-19 pandemic would have been a nail in the coffin for SIA if not for government support.

Based on current information and my view as of August 2020, I Would Categorize SIA Stock as a speculation, not investment.

Read next: Kodak Stock is Up Over 1,400% in Two Days. Does It Make Sense?

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Chris Lee Susanto

Founder of the value investing blog Re-ThinkWealth.com (if you type “value investing blog” in Google, his blog is likely the first one). Being a full-time investor himself, Chris knows that he did not beat the S&P 500 return so far (as of the time of this writing) by listening to stock tips. So, when he teaches, he also doesn’t believe in giving stock tips as it is not sustainable for you in the long run. He will teach you how to make your own intelligent decisions with his 4M1S framework. Feel free to also join his free investment telegram channel here.

More from Chris

The Eight Accounting Fraud or Red Flag Signs To Look Out In Stocks

In this article, I’d like to share eight signs of potential fraud in our stocks portfolio that we should be careful of. These are eight simple potential warning signs of bad financial reporting or early markers […]

My 5 Key Takeaway From AEM Holdings 1H 2020 Results

3. As of 1H20, Most Earnings Paid Out As Dividends Based on AEM 1H20 reports, their cumulative capital allocation breakdown from 2017 to 1H2020 is as follows: Dividends – 47%, Acquisitions – 25%, Capex – 18%, Buybacks – 10%. It is interesting to note that […]

Kodak Stock is Up Over 1,400% in Two Days. Does It Make Sense?

Eastman Kodak Company (NYSE: KODK) opened at $2.15 (Monday) on July 27, 2020, and closed at $33.20 (Wednesday) by 29 July 2020. That is a 1,444.19% increase over a two day period. In this article, I am going to give you some background on the Kodak company, the reason […]

Here Are 4 Reasons Why Intel Stock Plunged 16% Last Friday

Last Friday on 24 July 2020, Intel closed 16.24% down. Although I do not own any Intel stock, I was curious why it fell after releasing its Q2 2020 results. Just a while ago, I saw the news that after 15 years of partnership, Apple decided to break up with Intel and stop using its […]

My 5 Key Takeaway From Temasek Portfolio Value in 2020

1. Temasek Portfolio is Huge. Although I know that Temasek has a huge portfolio, I was surprised to see that it is around the size of Warren Buffett’s. As of 31 March 2020, the net portfolio value or NPV is at S$306 billion. So we have our own Warren Buffett in Singapore, that is […]

What I Learnt From Adam Smith About Investment and Money

Who is Adam Smith? Adam Smith (1723-1790) was a philosopher and economist who was best known for authoring the book An Inquiry into the Nature and Causes of the Wealth of Nations. Wealth of Nations also happens to be one of Warren Buffett’s favourite books […]

A List of Value Investing Funds in Singapore and Outside of Singapore

As a value investor, as a practitioner of value investing, I am very interested in studying funds I view as an executioner of the various value investing methodologies I myself am very passionate about. In this article, I will list down some of the value investing funds in […]

Protected: My Gratitude Journal as An Investor (And The Benefits of It)

There is no excerpt because this is a protected post.

How to Get Rich by Investing in Stock Market? Patience

How do people get rich by investing in stocks? Can we actually get rich by investing in stocks? Yes, we can. But we need to utilize both Patience and Compound Interest in Great Companies. With the proper foundation, framework, character, and skills, I truly believe that […]

Here’s What Sun Tzu Art of War Quotes Can Teach Us About Investing

Sun Tzu Art of War Quotes “He will win who knows when to fight and when not to fight” – We should only invest when there is clear benefit to do so, do not do something just for the sake of doing something. “If you know the enemy and know yourself, you need not fear […]

Thinking, Fast and Slow Book Summary (What I Learnt As An Investor)

In this thinking fast and slow book summary, I will explain to you the various human biases that we have and why it is important for us as investors to understand it. It all begins with a simple premise that we all have two systems in our brain, system 1 and system 2 […]

7 Key Investing Lessons from Charlie Munger & Li Lu Interview

I chanced upon an edited transcripts from Guru Focus of an interview of Munger and Li Lu in one of China’s top finance magazines. Here are the 7 investing lessons I learned from Charlie Munger and Li Lu’s interview: 1. In investing, patience is very […]