Options

Part 2 of 2: The Limitations of The Black Scholes Model (by Warren Buffett)

Chris Lee Susanto, Founder at Re-ThinkWealth.com

24 October 2018

This is the second of the two-part article series on The Black-Scholes model. In the first part, we had covered how we can use The Black-Scholes model to price options and in this second part, the limitations of the Black-Scholes Model (including Warren Buffett’s opinion on it).

Summary

- The first limitation is that the original Black Scholes model does not take into account the dividends of stocks in valuing the options.

- The second limitation of the Black-Scholes model is one that is pointed out by a person I greatly admire, Warren Buffett himself. It got to do with the Black-Scholes limitations of valuing long-dated options.

A Brief Recap of The Black-Scholes Model

Before we touch on the limitations of Black-Scholes by Warren Buffett, let’s do a brief recap. In the first part of the article, we talked about how the Black-Scholes model is used to price options. They are commonly known as the options pricing model to know the fair price of the put or call options. There are six variables that are taken into account in calculating the options value. The six variables are time to expiry, the underlying stock price at the time, volatility of the underlying stock, type of option, strike price and risk-free rate. So this means that the value derived using the Black-Scholes model got to do with the inputs that are being put into the model – pretty straightforward.

Does the Black-Scholes Model Make Sense?

First, I believe that the Black-Scholes model makes good sense. Based on the formula of the model, it makes good sense that when the underlying price increases, the cheaper the options will be if it is a put option. And more expensive if it is a call option. So depending on whether you are a seller or a buyer of these options, the value of your options will increase or decrease accordingly.

For example, the buyer of the put options has the right to sell the stock at a predetermined strike price. If prices keep on going up, the put options contract logically become less of a value. Because why would the put options buyer want to sell its stocks at the lower strike price of the put options if selling at the market can fetch a higher price? And in this scenario, the seller of the put options who had received premiums/payments from the buyer of the put options will not need to be obliged to buy the stocks from the buyer of the put options. Hence, the put options become worthless on expiry if the price keeps on going up. Thus, put options value decreases when the underlying price of the stock keeps on going up.

Based on the formula of the model, it also makes good sense also that the greater the volatility, the higher the options price/value will be. Higher uncertainty will result in higher premiums due to higher perceived risks. It is the way it should be. It makes good sense too. Bonds by the government has less volatility so we are compensated lesser. As compared to if we invest in say stocks that have higher volatility and higher uncertainty.

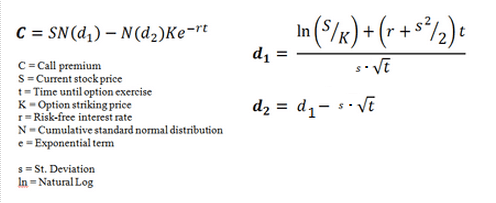

The Original Formula of the Black-Scholes Model

To recap, this is the original formula for Black-Scholes:

Source: Investopedia

The original Black-Scholes formula takes into account the current stock price, time to expiry, options strike price, risk-free interest rate and the cumulative standard normal distribution which is known as the implied volatility or simply how volatile the stock is.

The Limitations of the Original Black-Scholes Model (Dividends Not Accounted for)

Here is the first limitation that I came out with: The underlying price of a stock will usually decrease accordingly by the amount of cash dividend declared on the ex-dividend date of a company. So, dividends do play a role too because it affects the underlying price of a stock. But in the Black-Scholes model, it makes the assumptions that no dividends are paid out during the life of the options. This means that a company that pays a lot of dividends will usually have the stock price decrease in relation to it. If during the course of the options, the company pays those dividends, the put options should be worth more and the call options should be worth less. But the original Black-Scholes model does not take those into dividends into account – and we need to adjust it accordingly. We can do that by subtracting the present value of the upcoming dividends of the stock during the life of the options from the current stock price – in which we then input the subtracted value to the original Black-Scholes model.

The Limitations of the Original Black-Scholes Model (by Warren Buffett)

The second limitation of the Black-Scholes model is one that is pointed out by a person I greatly admire, Warren Buffett himself. It got to do with the Black-Scholes limitations of valuing long-dated options.

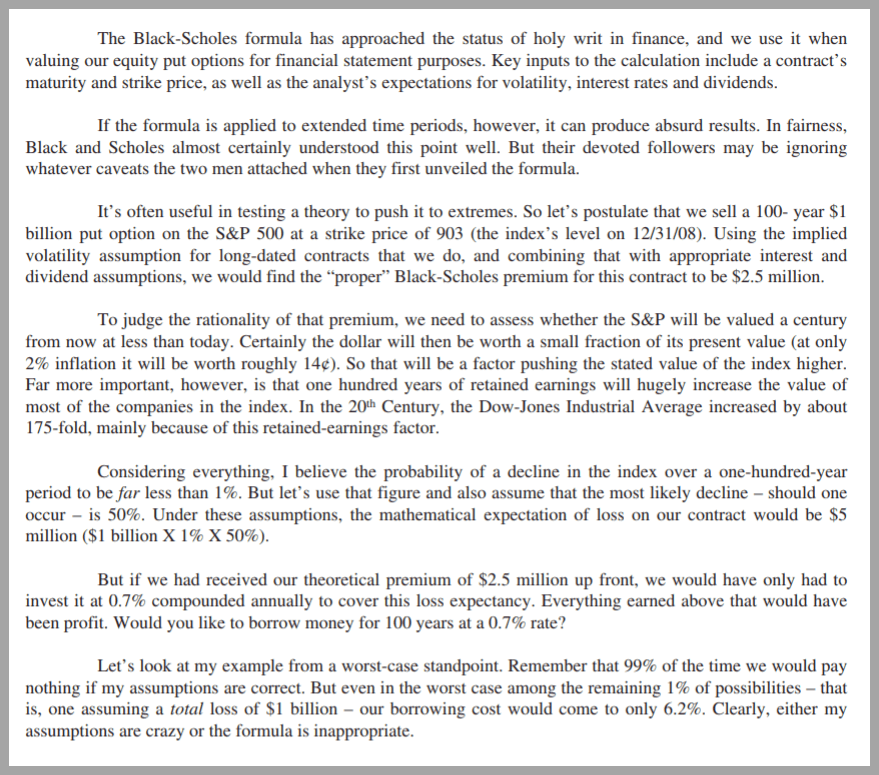

Source: Berkshire Hathaway 2008 Annual Report

Based on Warren Buffett, while the Black-Scholes model has been the widely used model to value equity put options, he thinks that there are limitations to it – when the model is applied to an extended time period, they can produce absurd results. So Waren Buffett is saying that the Black-Scholes model is bad at valuing long-dated options.

Warren Buffett also gives an example to explain this theory of his by pushing it to the extremes as you can see from the image screenshot above. He gave the example of selling a 100-year-old $1 billion put option on the S&P 500 at a strike price of 903 which was the index’s level on 31 December 2008. Using the “proper” Black-Scholes model at the time, he will get a premium of about $2.5 million. And he sees that the expected loss on the contract would be $5 million (by taking $1 billion which is the contract value of the options times a 1% chance that 100 years from now the S&P 500 is going to be worth less and times it by 50% which is the chance of that decline).

Using this example, Warren Buffett said that if he received the $2.5 million up front, he only need to invest and get 0.7% annually for the next 100 years to cover the expected loss. So he said that this is akin to borrowing the money which is $2.5 million for a rate of 0.7% annually. Even at a total loss of $1 billion, the “borrowing cost” will only be about 6.2%.

For Warren Buffett personally, he has made use of these kinds of market inefficiency to sell put options when the volatility is high so that he was able to get more premiums/cash flows. And then he uses these premiums/cash flows to invest and get returns.

“Our put contracts total $37.1 billion (at current exchange rates) and are spread among four major indices: the S&P 500 in the U.S., the FTSE 100 in the U.K., the Euro Stoxx 50 in Europe, and the Nikkei 225 in Japan. Our first contract comes due on September 9, 2019 and our last on January 24, 2028. We have received premiums of $4.9 billion, money we have invested. We, meanwhile, have paid nothing, since all expiration dates are far in the future. Nonetheless, we have used Black-Scholes valuation methods to record a yearend liability of $10 billion, an amount that will change on every reporting date. The two financial items – this estimated loss of $10 billion minus the $4.9 billion in premiums we have received – means that we have so far reported a mark-to-market loss of $5.1 billion from these contracts.” – Warren Buffett

While Warren is able to utilize the volatility of the stock market to get more premiums, he criticizes Black-Scholes as being limited simply because of the financial reporting regulation that forces him to use the Black-Scholes.

Disclaimer:

The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

No Results Found

The page you requested could not be found. Try refining your search, or use the navigation above to locate the post.

Wait, Wait!

I often share insights that I do not share in this blog over at my Facebook page. Don’t forget to like it before you go!

Reasons Why One Of My Top Holdings Keryx Biopharmaceuticals (NASDAQ: KERX) Went Up 10.12% in One day

KERX is one the top holdings of my portfolio to which I categorized it as a growth stock - which means there is a potential for it to grow multi-fold in terms of the stock price. I first talked about KERX in my earlier article and it gives a good summary of the stock....

Key Take Aways From AIESEC SIM Youth Dialogue 2016

"You don't have to be great to start but you have to start to be great"- Zig Ziglar 1) Develop a growth mindset instead of a fixed mindset Do not let the voices inside your head dictates what you can or you cannot do. You feed the beliefs in your head, so if you feel...

My Week 8 Summary of Yale University Financial Markets Course: Conclusion to the 8 Weeks Course

Non- Profit Finance The idea of finance for a long time has always been to make a lot of money. However, in fact, non-profit finance is a pretty big thing in the United States - it is around 4% of their gross domestic product (GDP). Many people such as Professor Dean...

3 Reasons Why I Bought Keppel DC REIT (SGX: AJBU)

Keppel DC REIT (AGX: AJBU) is a Singapore-based real estate investment trust (REIT), established with the main investment strategy of investing in a portfolio of income-producing real estate assets which are used primarily for data centre purposes, with an initial...

Want To Be Rich? Get The Right Habits and This Is How You Can Start…

I have never been a believer of getting rich quick schemes, success to me is nothing but 1% inspiration and 99% perspiration - with an element of luck that will only come along to those who are prepared. Ultimately, no matter who you are, I believe that becoming rich...

My Week 7 Summary of Yale University Financial Markets Course: Critical Elements of the Financial Infrastructure

The Financial Infrastructure Includes: 1) Buy side People who are in the business of buying securities like stocks and bonds. They do it as professionals. Professional Investment Managers and Their Influence The law prescribes that Investment Managers who manage other...

#FAQ: What Is Value Investing?

As Investing is both an art and also a science, similarly different people can have a different definition of value investing - I can share with you mine in a few short paragraphs: It is essentially buying the stock of a cheap and good business with a large enough...

My Week 6 Summary of Yale University Financial Markets Course: Key Role of Banks and Monetary Policies

Disclaimer: This will be one of the more "difficult to understand" chapter as compared to the past 5 weeks (although I tried my best to make it as easy as possible to understand) - so feel free to ask me any questions! Guide: Bank Runs = A situation that occurs when...