Reflections, 13 March 2024

Asbury Automotive: An Undervalued Gem in The Stock Market?

by Chris Susanto,

Founder, Re-ThinkWealth.com

Mentor, VIM.sg

This article is suitable for:

Beginners and intermediate investors.

First, disclaimer: As of this writing, I am vested in Asbury Automotive Group, Inc.

In this article, I will share a little bit more about what Asbury does as a company and a little bit about its current valuation.

What does Asbury Automotive do?

Image source: Asbury Automotive

I have owned shares in Asbury Automotive Group, Inc., for about 18 months.

Asbury is essentially a collection of many automobile dealerships. They operate around 158 new-vehicle stores and 37 collision centers.

Over 70% of their new vehicle revenue is from luxury and import brands. They also offer third-party financing and insurance products.

Asbury operates in sixteen states in the US. And it generated $14.8 billion in revenue in 2023. They target at least $30 billion of revenue sometime between 2025 and 2030.

Is Asbury Automotive an Undervalued Gem?

Image source: Asbury Automotive

Since 2018, Asbury has experienced a 115% increase in revenue (17% CAGR) and a 288% increase in Adj. Eps (31% CAGR), and a 90% increase in new car dealerships.

They have historically grown by acquisitions.

Asbury has also been repurchasing their own shares through their share buyback program and has purchased 1.3M shares so far using $258M in 2023.

However, revenue growth has been stagnant in 2023, with total revenue for the full year 2023 at $14.8 billion, which is a 4% decrease from the prior year.

EBITDA decreased by 15% from the prior year to $1.1 billion, while adjusted operating cash flow for 2023 was $705 million, a decrease of $282 million from the prior year.

For the full year 2023, Asbury reported net income of $603 million compared to $997 million in the prior year, which is a decrease in net income of around 39.5% year over year.

Despite the drop in earnings, based on Asbury’s current market capitalization of $4.3B as of 13 March 2023, the current price-to-earnings ratio is only around 7.13, which, in my view, is attractive.

Future Outlook of Asbury

In 2023, Asbury already used $258 million to repurchase 1.3 million shares (average price: $198.46). As of December 31, 2023, the company still has another $203 million remaining on its share repurchase authorization.

Buyers of luxury brands such as Lexus and BMW have higher incomes than average (and Asbury gets over 70% of new vehicle revenue from luxury and midline imports). This means that these buyers are usually those who can afford a new car and maintain their cars even during a recession.

Image source: Asbury Automotive

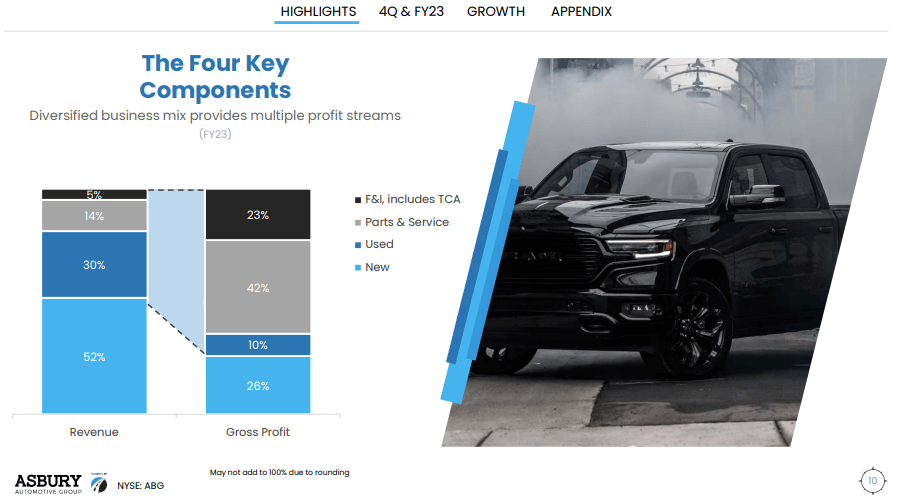

Parts and servicing is a high-margin business for Asbury because although it only contributed around 14% of 2023 revenue, it contributed 42% of gross profit. People normally go to the dealer for repair because of the automakers’ warranty requirements.

Conclusion

My view is that Asbury Automotive differentiates itself in the market through its economies of scale and its focus on luxury brands, which attracts a more affluent customer base.

Yes, the company’s long-term debt to TTM net income is slightly high at around 5+ ($3.343B long-term debt compared to $602.5M TTM net income), but in my view, it is still alright for a company that grows primarily through acquisition.

Operating cash flow is also still strong. With a price-to-earnings ratio of slightly over 7, my view is Asbury Automotive stock currently looks attractive.

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Disclosure:

As of the time of this writing, I/we have a beneficial long position in the shares of Asbury Automotive Group, Inc (NYSE: ABG). I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Be an Insider!

Click here to join our FREE Telegram Channel now!

Like what you just read? share it.

About the writer

Chris is the founder of Re-ThinkWealth.com. He is also the founder of VIM/Value Investing Mentorship™, a Board Member in Bansea (Asia’s Oldest Angel Investment Network) and SPGG (Singapore Polytechnic Graduates Guild), and an independent director in Bansea Fund 2.

Since 2015, Chris has been empowering value investors through his passion for value investing, guiding individuals through his blog (Re-ThinkWealth.com) and private mentorship program at VIM. He leverages his extensive experience, including serving as an Independent Director of Bansea Fund 2 and Board Member at SPGG & Bansea (Asia’s oldest angel investment network), and his own investing journey starting at 21 to mentor and empower the next generation of value investors. Chris is a sought-after mentor/speaker, having shared his expertise at institutions like CGS-CIMB, NTU Singapore Financial Conference, SMU IIE, NUS Invest, Seedly TV and Money FM 89.3.

Learn more about building your value investing skills with VIM, a private mentorship and community (capped at 150 mentees/students), at: https://www.vim.sg/

Read more insights?

2 Billion Users ( > China Population): Why I Am Long on Facebook Stock

But over time, I would like to invest in good businesses at a fair price instead of continuing to invest in an OK business at a cheap price. Due to Facebook’s recent drop in its share price, I took a stake in Facebook during the past few months and right now, it consists of about a quarter of my portfolio.

Part 2 of 2: The Limitations of The Black Scholes Model (by Warren Buffett)

Before we touch on the limitations of Black-Scholes. let’s do a brief recap. In the first part of the article, we talked about how the Black-Scholes model is used to price options. They are commonly known as the options pricing model to know the fair price of the put or call options. There […]

Part 1 of 2: Here’s How to Use The Black-Scholes Model to Price Options

The Black-Scholes model was first developed by three economists. Two of them – Myron Scholes and Robert Merton – received a Nobel prize in 1997 for their work in this model. The Black-Scholes model is also commonly known as the options pricing model. And as the name indicates […]

New Logo Design for Re-ThinkWealth (Value Investing Blog)

The above image is how the new Re-ThinkWealth logo looks like. As you might have noticed, it is a combination of “R” and “W” which stands for Re-ThinkWealth. At the same time, the shape of the logo embodies the resemblance of how a stock market will behave. The stock market goes down and up […]

Here Are My Reflections After 3 Years 7 Months in The Stock Market

So basically, I knew that if I cannot beat the S&P 500 return over the long run, it’s better if I just invest in the S&P 500. While the S&P 500 practices in a huge diversification of 500 big companies listed in the U.S., my U.S. portfolio practices concentration of ideas in which I am most certain about […]

10 Reasons Why We Should Rethink How to Build Our Wealth

I am 25 years old this year and I am always fascinated by how a change in our thinking can result in a huge change in our wealth. I am convinced by the notion that how we think creates the wealth that we have. And writing has been an integral part of it all because it gives me an avenue to pen […]