GameStop Corp (NYSE: GME)– A Cigar Butt Investing Play

Chris Lee Susanto, Founder and CEO, Re-ThinkWealth

12 May 2017

SUMMARY:

- GameStop’s valuation is at an all-time low

- Gross profit margins have been doing well

- Debt management is good

- I purchased it via selling a put option at 21.5 USD

- I valued it to be between 26 USD to 30 USD per share

How GameStop Caught My Eye As A Potential Cigar Butt Investing Play

It has been my habit to look around for investment opportunities on a regular basis.

Back in March 2017, I saw a high premium put option for this particular company called GameStop– 0.55% return for selling two days put option at the strike price of 21.5 USD. It was trading at around 24 USD back on 22 March 2017.

Of course, I decided to take a closer look at the company to assess if it is a good opportunity.

For those of you who have been following my blog for a while, you will know that selling options forms a core part of my overall investing strategy.

Brief Background On GameStop

GameStop is a video game speciality store from the United States and is headquartered in Grapevine, Texas. It operates over 7.600 stores throughout the United States, Canada, Australia, New Zealand and Europe– totalling across 14 countries.

It is a fortune 500 company– which means that its revenue is ranked in among the top 500 US companies.

They generate revenue from a few different sources– video games, collectables and technology– using different retail brand names such as GameStop, EB Games, Micromania, Spring Mobile, Simply Mac, Cricket Wireless and ThinkGeek.

At that point in time, from the outset, I know that retail stores are in a recession. In the country where I spent a lot of time, Singapore, many retail stores– even the iconic one such as John Little– closed their last store in December 2016 after 174 years in Singapore.

I already have the pre-assumption that a retail stock is bad.

However, decided to take a closer look.

During the most recent news release in 2017, GameStop gross margin expanded to a record rate of 35% and collectables sales achieved high-end revenue target growing 59.5%– helped by strong sales of Pokemon-related toys and apparel– to 494.1 Million for the year 2016. Video game sales were of course, weak– as I have had expected.

Looking at the year 2017, technology and collectables are expected to generate strong growth while the new hardware innovation in the video game category also looks promising.

This is the 2017 outlook provided by the management:

GameStop is providing the following guidance for fiscal 2017 (dollars in millions, except per share):

| Total Sales | -2.0% to +2.0% | |

| Comparable Store Sales (excludes Tech Brands stores) | -5.0% to 0.0% | |

| Depreciation & Amortization Expense | $150.0 to $160.0 | |

| Income Tax Rate | 35.0% to 35.5% | |

| Operating Margin | 6.5% to 7.0% | |

| Net Income | $320.0 to $354.0 | |

| Earnings Per Share (diluted) | $3.10 to $3.40 | |

| Capital Expenditures | $110.0 to $120.0 | |

| Technology Brands Operating Earnings | $120.0+ |

Earnings per share guidance are calculated based on weighted average shares outstanding of 102,500,000.

In 2017, the Company anticipates that it will open approximately 35 new Collectibles stores globally and approximately 65 new Technology Brand stores. The Company also anticipates that it will close between 2% to 3% of its global store footprint.

Potential Dividend Machine?

Source: Y Charts

Source: Y Charts

They have been increasing their dividends paid to shareholders since 2014.

For a retail store like GameStop to consistently increase their dividends paid, their cashflow needed to be stable.

A further update to the above chart revealed that on 1 March 2017, GameStop’s board of directors approved a further 2.7% increase in its regular annual cash dividend from 1.48 USD to 1.52 USD per share.

The question is really about how much is the current payout ratio for them since 2014.

That will shed a little bit of light on how much of their cash flows are paid out as dividends and how much are retained as retained earnings– and whether their dividends payments are sustainable or not.

The payout ratio is basically the proportion of earnings that is paid out to shareholders as dividends.

GameStop Payout Ratio

Source: Y Charts

Source: Y Charts

While the payout ratio has been increasing well over the past 10 years, it is still below the 50% mark. That means that they are able to pay out, even more, dividends if they want to.

GameStop Dividend Yield

Source: Y Charts

Source: Y Charts

Here is the surprising thing…

As GameStop increase their dividends paid and their payout ratio, their dividend yield rises along with it.

That can only mean one thing.

That means that as they are paying more dividends, their share price is also decreasing. That is because dividend yield is the dividend of a company expressed as a percentage of their current share price.

As an investor, this situation is interesting because it signals cheap valuation. Quite a similar situation with my previous investment in Mobile Telesystems (NYSE: MBT).

Manageable Debt

The key for a retail company to survive is whether they have a manageable debt or are they using too much debt.

If a company uses too much debt, they might not be able to meet their debt obligations and default payment as a result.

Quick And Current Ratio

Source: Y Charts

Source: Y Charts

The current ratio is calculated by taking the company’s current assets and dividing it by its current liabilities.

From the chart above, you would notice that GameStop has a current ratio of 1.215– well above 1– which means that their current assets can cover their current liabilities well.

The quick ratio is calculated by taking cash, marketable securities and accounts receivable and divide it by its current liabilities. This is a more stringent test to analyse a company’s debt.

From the chart above, you would notice that GameStop has a quick ratio of 0.505– which is well below one. However, historically the ratio has been this way since 2010.

This means that although GameStop is able to cover their current liabilities well using their current assets, their debt management would be considered as good rather than superb– as they cannot pass the quick ratio test.

Good Earnings

We have concluded that GameStop debt management is considered good. However, the key to sustainable managing debt well comes from their earnings.

In looking at whether a company has good earnings, a simple indicator I look at is their gross profit margins, Return on Assets and Return on Equity.

Gross profit margin is the proportion of money left over from revenues after accounting for the cost of goods sold.

Return on assets shows how profitable a company is as a percentage of their total assets. It is calculated by dividing the company’s annual earnings by its total assets.

Return on equity shows how profitable a company is as a percentage of their total equity. It is calculated by dividing the company’s annual earnings by its total equity.

GameStop Gross Profit Margin

Source: Y Charts

Source: Y Charts

You notice that from the chart above, gross profit margin has been increasing from 2005 and as of January 2017, it is 34.96%.

Historically, it is a good sign for GameStop but comparatively, the industry standard ranges around 40% easily for gross profit margins.

GameStop ROA And ROE

Source: Y Charts

Source: Y Charts

Similar with the gross profit margins, their ROA and ROE has been increasing these past few years –19.42% for ROE and 9.39% for ROA in 2016.

This is a good sign.

Rising Earnings Per Share

Source: Y Charts

Source: Y Charts

Another good sign in terms of profitability is that as gross profit margins, ROA and ROE increased, their earnings per share (EPS) increases along with it.

As their EPS increase, the company also continually buy back their shares which reduced their share outstanding to an all time low at 101.87 Million.

Cheap Valuation (1st Level Thinking)

Source: Y Charts

Source: Y Charts

If you look at the various metrics that I found to be relevant for GameStop valuation based on the above chart, their valuation looks cheap and is at an all time low.

Why Is It Cheap? (2nd Level Thinking)

Looking at the cheap valuation, many investors might be quick to jump in and label this as a value buy.

However, second level thinking requires us to ask deeper. Why is it cheap?

GameStop’s share price sank after a bad Q4 earnings that were reported on 24 March 2017 because they missed on revenue and gave a poor guidance.

The stock is cheap because the growth of sales is forecasted to slow down– as they plan to close 2-3% of their most unprofitable stores in 2017.

This will decrease their revenue but their margins might improve further in the long run.

Cigar Butt Investing

In cigar butt investing, the idea is that is we buy a stock at a very low price, there will usually be an opportunity for the investor to sell the stocks at a decent profit– even though the long-term performance of the stock might be bad.

The thing to take note is that whether the original “cheap” price is really cheap after all.

That is because a low valuation of a stock may prove to be expensive if the earnings of the business continue to fall.

In Conclusion

With the knowledge that GameStop’s stock is cheap for a good reason. Investors do not see this stock as a growth stock but rather a matured and declining business that warrants a low valuation.

However, the current forward PE ratio of 6.7 based on 2017 guidance which yields a 7% dividend yield warrants a closer look as to whether this is a potential cigar butt investing play.

While GameStop’s sales might decrease a lot due to the drop in demand for video game purchase via retail stores, the drop will not be catastrophic as it will be offset by the increase in demand for collectables and technology products– in which they aim to open 35 and 65 new stores respectively.

I valued GameStop to be a buy and to be worth about 26 USD to 30 USD.

Disclaimer: The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

The Role of Synergies in M&A; Reliable to Warrant a Premium Over Market Value?

Today, I want to talk about the role of synergies in M&A. And is it reliable enough for companies to pay a premium over market value because of it?

I for one think that this is a very important topic to discuss for both investors and business people alike. Simply because people tend to be over optimistic of the future and […]

Warren Buffett Often Talks About Intrinsic Value: What is it?

Warren Buffett often talks about intrinsic value. But what exactly is an intrinsic value? Knowing what is intrinsic value is the FIRST step for any aspiring investors who want to be a practitioner of value investing. UNDERSTANDING what is intrinsic value is, of course, the second step for aspiring value investors. Because […]

My Thoughts on Qualcomm Q1 2018 Results

Yesterday’s was Qualcomm’s release of its quarter 1 2018 results. You can view its SEC filing here. It is for the quarterly period ended March 25, 2018. A short background, Qualcomm is simply the company behind most of the smartphones that we are using – in terms of the chips or you can call it, the “brain” […]

Good Result and Yet The Stock Fell 10+% – GameStop’s So Unloved

The stock hit fresh near 13 year low despite the company doing pretty well during the earnings call on 28 March 2018. It closes at 10.39% down. It is not an easy day for any GameStop holders (except the short sellers), from my end, I am thinking where I could have gone wrong – or is the market wrong. I am more than willing to […]

Here’s My Thoughts on GameStop’s Q417 Earnings Results (Released 28/3/2018)

Despite the increase in sales and the beat in earnings from analyst estimates, their profits are still down 11.4% year on year basis on the adjusted diluted EPS portion (from $3.77 to $3.34). However, $3.34 is near the top of the management guidance for FY2017 – and the focus on improving the trade awareness where […]

5 Reasons Why Having The Long-Term View is Vital in Stock Investing

Having a long-term view is important in stock investing. And the reason is not just because many of the world’s most successful and richest investors such as Warren Buffett and Seth Klarman say so. “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” – Warren Buffett […]

Is GameStop Doomed? I Visited Their Stores in NY to Find Out

As of the market close on 11 January 2018 at $19.96, I am at a 7.81% paper gain excluding of realized gains I received via dividends and options premium. And GameStop consists of 30.80% of my portfolio – second on the list – with the first being Qualcomm at 40.60% of my portfolio. Naturally, going down to GameStop stores in New […]

Last day of 2017 – A Review of My Investment Journey So Far

This year, the stock market rally would have given many investors with a good profit – the Dow (top 30 company in the united states stock market) up 25%, S&P 500 (top 500 company in the united states stock market) up 19% and Nasdaq are up 28% this year. And I think it is maybe time to be cautious. Or I should say, cautiously […]

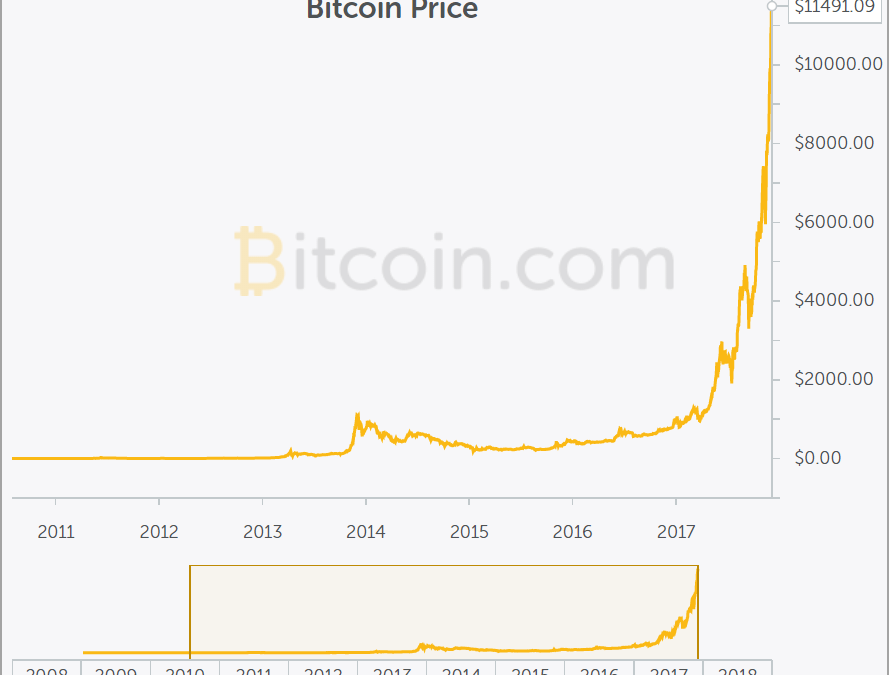

Here’s My Opinion on Bitcoin

Bitcoin is a currency that was founded/discovered pretty recently in 2009 by a person (still unknown) using the alias Satoshi Nakamoto.The good thing about transacting using Bitcoin is that there will be no middleman required to do the transacting. There is also no fees tagged to transacting with Bitcoin and no requirements […]

What is moat in Warren Buffett’s terms & why it’s important

Moat is important because it protects a company from losing their market share easily which will erode its earnings power over time. This is important for us as investors because we would want the company we invest in to have its earnings grow over time – then the share price will follow – and not the other way round. So, we […]

Want new articles before they get published? Subscribe to our Awesome Community.