Growth or Value Investing? Why Not Both?

27 July 2021

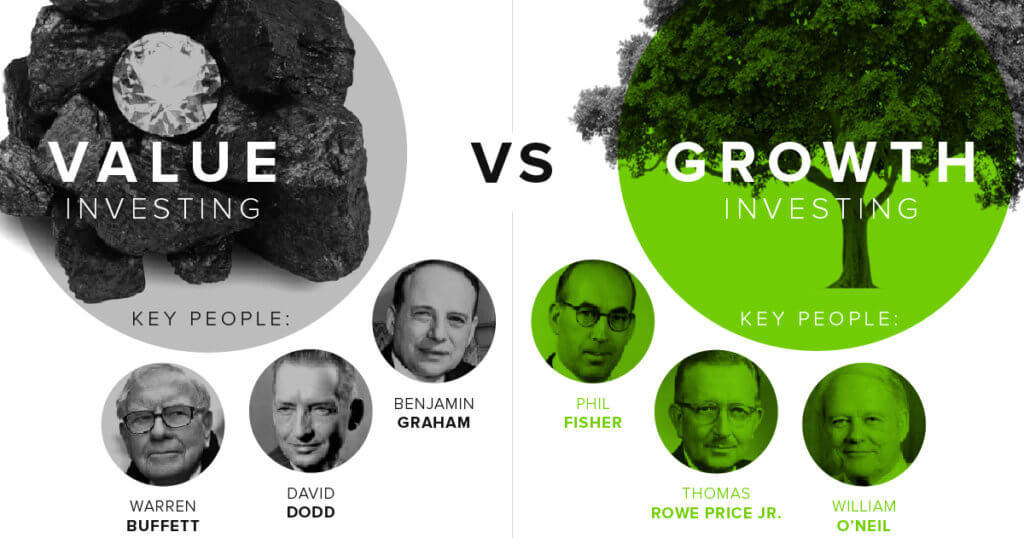

What is The Traditional Definition of Value and Growth Investing?

Image source: Visual Capitalist

In the traditional sense, value investing could be defined as buying a stock that is worth $1 today for 50 cents.

In the traditional sense, growth investing could be defined as buying something that is worth $1 today for $1.50 but it could be worth $6, five years from now.

Based on the Economic Times, growth investing is about finding companies that are expected to grow faster than the market while value investing is identifying companies whose stock prices are lower than their fundamental worth.

Why In My Definition, Value, and Growth Investing Essentially Has The Same Goal

Yes, growth stocks do not normally give out dividends and value stocks have the perception that they give out dividends more often. But value and growth investing have the same goal: which is to find the biggest opportunity or a gap or mispricing in relation to the business value at that point in time.

Both should simply be called “investing” or “business-focused or business-like investing”. Because both growth and value investing are business-focused investing in which an investor buys because they find that the price is cheap or reasonable in relation to what the true value of the business is.

There are more similarities in both the traditional senses of value investing and growth investing than we think.

Be it growth or value investing, like Warren Buffett said, “Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily understandable business whose earnings are virtually certain to be materially higher five, 10, and 20 years from now.”.

In Value or Growth Investing, Patience + Understanding of The Business is Key

In both value and growth investing, if we want to have big money, patience is one of the key ingredients for it. But again it really depends, a turnaround play can take less than 1 year to play out, on the other hand, asset play can take a few years or compounders – we may never want to sell it ever.

Ultimately, based on the type of company, we have to know which companies are worth paying a fair price or even a premium on.

“I don’t want to spend my time trying to earn a lot of little profits. I want very, very big profits that I’m ready to wait for.” – Philip Fisher

And hence, in both value and growth investing, we need to understand the business well enough to know at what price is good enough for us to buy it. So in the future, we have a reasonable probability of selling them at big profits (because we know their fair and overvalued range in relation to the price we bought them at).

I View The Categorization As We Are Either A Value or Growth Investor Limiting

Image source: Pixabay

If we view ourselves as a growth investor, then in the traditional sense, we will say no to value plays, asset plays, and turnaround plays for non-growth companies. And I find that limiting. Because in investing, we need to be flexible and adaptable as long as the opportunities are within our circle of competency, we should hit the big fat pitch that is right in front of us – no matter if it is growth or value plays.

So I propose us simply being an investor. A focused investor that is open to opportunities that we can understand be it in the traditional value plays or growth plays. Not saying no to the other simply because of our limiting categorization of ourselves either as a value or growth investor.

“Value investing, the way I regarded it, will never go out of style because value investing, the way I conceive it, is always wanting to get more value than you pay for when you buy a stock and that approach will never go out of style. Some people think that value investing is you chase companies that have a lot of cash and they’re in a lousy business or something. But I don’t define that as value investing. I think all good investing is value investing, and it’s just that some people look for values in strong companies and some look for values in weak companies, but every value investor tries to get more value than she pays for.” – Charlie Munger

So did Charlie just described value investing? or growth investing? My point is that it does not matter. All good investing should be the same – buying things for less than what we think will be worth in the future.

In Conclusion

Opportunities come from many angles.

A traditional value kind of investor should not overlook growth companies. A growth kind of investor should not overlook traditional value plays.

We should simply invest in anything that we understand and find mispricing in. Categorizing ourselves either as a growth or value investor in my view can be limiting.

I prefer to see myself simply as an investor, business-focused investing, or quality-focused investor.

Because in both the traditional kind of value or growth investing, we ultimately need to find quality in the play, and not speculate.

As long as I understand the business and it is run by great management, selling at a reasonable price compared to the business quality, I am open to investing in it – be it in the so-called value or growth companies. Because in my view, there is value in growth and there is also growth in value.

Based on Merrill, growth stocks tend to perform better when interest rates are falling and earnings are rising. But when economies are cooling, they are likely to be the first punished. While value stocks may do well early in an economic recovery but are typically more likely to lag in a sustained bull market.

Combining both value and growth strategies might give us the potential to gain throughout the economic cycles while staying within our circle of competence.

Even Fidelity suggests that we use a mix of growth and value strategies. They say it is akin to choosing between Batman and Superman. And I would agree. Why not do both?

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Disclosure:

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Learned something from this article?

Share it 🙂

Chris Lee Susanto

Founder, investment blogger, full-time investor, and editor of this quality investing x business-like stock investing blog Re-ThinkWealth.com.

Chris is a big proponent of business-like stock investing – a mixture of both value and growth investing. He invests in companies where there is value to be found (as long as it is still within his circle of competence), be it a turnaround, depressed, value, or quality growth company (compounders). He either buys the stock outright or he profits through selling put or selling call options – or buying call options (buying and selling options are especially dangerous for those who do not know how to properly execute it).

Some of the places where Chris has been invited to speak or have added value as a mentor or writer includes Singapore Polytechnic, SMU Institute of Innovation and Entrepreneurship (IIE), Dollars and Sense, The New Savvy, Value Walk Blog, Investment Moats, NUS Tembusu College, NUS Investment Society, CGS-CIMB Singapore, Singapore Financial Conference by NTU IIC, The Financial Coconut Podcast, Money FM 89.3 and Internationally in Myanmar.

He is also a practitioner of Transcendental Meditation and Mindfulness practice. He also advocates regular exercise, enough sleep, and nutritious food as part of our lifestyle as an investor.

As of the time of this writing, Chris is focusing on setting up his MAS Licensed Fund with the goal to beat the market over the long run.

Feel free to join his FREE investment telegram channel here.

Don’t Leave First, Read Also:

Sustainability of Dividends

First, we must understand that business conditions are dynamic. Occasionally, different cycles will cause earnings to fluctuate up or down and it affects the business’ ability to pay out dividends. As investor, we must never have the expectations for dividends to remain the same forever […]

The Role of Synergies in M&A; Reliable to Warrant a Premium Over Market Value?

Today, I want to talk about the role of synergies in M&A. And is it reliable enough for companies to pay a premium over market value because of it?

I for one think that this is a very important topic to discuss for both investors and business people alike. Simply because people tend to be over optimistic of the future and […]

Warren Buffett Often Talks About Intrinsic Value: What is it?

Warren Buffett often talks about intrinsic value. But what exactly is an intrinsic value? Knowing what is intrinsic value is the FIRST step for any aspiring investors who want to be a practitioner of value investing. UNDERSTANDING what is intrinsic value is, of course, the second step for aspiring value investors. Because […]

My Thoughts on Qualcomm Q1 2018 Results

Yesterday’s was Qualcomm’s release of its quarter 1 2018 results. You can view its SEC filing here. It is for the quarterly period ended March 25, 2018. A short background, Qualcomm is simply the company behind most of the smartphones that we are using – in terms of the chips or you can call it, the “brain” […]

Good Result and Yet The Stock Fell 10+% – GameStop’s So Unloved

The stock hit fresh near 13 year low despite the company doing pretty well during the earnings call on 28 March 2018. It closes at 10.39% down. It is not an easy day for any GameStop holders (except the short sellers), from my end, I am thinking where I could have gone wrong – or is the market wrong. I am more than willing to […]

Here’s My Thoughts on GameStop’s Q417 Earnings Results (Released 28/3/2018)

Despite the increase in sales and the beat in earnings from analyst estimates, their profits are still down 11.4% year on year basis on the adjusted diluted EPS portion (from $3.77 to $3.34). However, $3.34 is near the top of the management guidance for FY2017 – and the focus on improving the trade awareness where […]

5 Reasons Why Having The Long-Term View is Vital in Stock Investing

Having a long-term view is important in stock investing. And the reason is not just because many of the world’s most successful and richest investors such as Warren Buffett and Seth Klarman say so. “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” – Warren Buffett […]

Is GameStop Doomed? I Visited Their Stores in NY to Find Out

As of the market close on 11 January 2018 at $19.96, I am at a 7.81% paper gain excluding of realized gains I received via dividends and options premium. And GameStop consists of 30.80% of my portfolio – second on the list – with the first being Qualcomm at 40.60% of my portfolio. Naturally, going down to GameStop stores in New […]

Last day of 2017 – A Review of My Investment Journey So Far

This year, the stock market rally would have given many investors with a good profit – the Dow (top 30 company in the united states stock market) up 25%, S&P 500 (top 500 company in the united states stock market) up 19% and Nasdaq are up 28% this year. And I think it is maybe time to be cautious. Or I should say, cautiously […]

Here’s My Opinion on Bitcoin

Bitcoin is a currency that was founded/discovered pretty recently in 2009 by a person (still unknown) using the alias Satoshi Nakamoto.The good thing about transacting using Bitcoin is that there will be no middleman required to do the transacting. There is also no fees tagged to transacting with Bitcoin and no requirements […]

What is moat in Warren Buffett’s terms & why it’s important

Moat is important because it protects a company from losing their market share easily which will erode its earnings power over time. This is important for us as investors because we would want the company we invest in to have its earnings grow over time – then the share price will follow – and not the other way round. So, we […]

GameStop Q3 17 Earnings — Glad Going Against The Crowd Was Right

25% of their stores have already been turned to GameStop plus format which is a 50–50 combination of games and collectibles. What is interesting here is that despite lesser space to put video games, they actually see an increase in video games sales. This got to do with the new types of customers that these […]