Stock Analysis [Simple]

Here’s My Quick Thought on Starbucks Stock

Chris Lee Susanto, Founder at Re-ThinkWealth.com

19 September 2018

Starbucks is a company that needs not much introduction. I am sure that most of us have drunk Starbucks coffee before. And many of us have studied or did some work or caught up with a friend there. Starbucks is a familiar company that is in almost every airport around the world. Their story though started back in Seattle, which was also where Microsoft started.

Starbucks company was formed back in 1985 and it became what it is today under the leadership of its ex-CEO, Howard Schultz who bought Starbucks back in August 1987 for only $3.8 million and turned it into a great brand it is today.

In April 2018, Howard stepped down as CEO to become executive chairman of Starbucks. Kevin Johnson, who has been with Starbucks for over a decade is now CEO.

China is currently Starbucks second largest and fastest-growing market. And Starbucks firmly believe that China and U.S. will be the two most powerful drivers for their future growth.

For the fiscal year 2017, Starbucks revenue grew 5% year on year to $22.4 billion. The revenue growth was due to a 3% rise in global comparable store sales, opening of more than 2,250 net new stores to bring their total store count to 27,000 and share gains in at-home coffee.

Moving ahead, Starbucks have a couple of key priorities that would form their business drivers (based on their 2017 letter to shareholders), they are:

1. Positioning for long-term growth in China

Starbucks firmly believes that the U.S. and China will be two major growth engines for Starbucks. China is where an increasing portion of the overall profit will be coming from. Every 15 hours, Starbucks opens a new store in China.

They have been in China for almost 20 years. And they just opened the world’s largest Starbucks location in Shanghai recently called the Shanghai Starbucks Reserve Roastery.

Starbucks’ partnerships with leading Chinese companies such as Alibaba and Tencent will also help them to perform well in Chinese market.

Recently in August 2018, Alibaba and Starbucks officially partner up to deliver coffee – starting with Beijing and Shanghai and will roll out to other parts of China in the future.

“We’re going to integrate a Starbucks virtual store into all of the Alibaba Group properties,” Johnson told “Mad Money” host Jim Cramer in an interview.

“This means that a customer that uses Alipay or Taobao or Tmall or Hema has an integrated Starbucks virtual store similar to the mobile app embedded right into that experience,” the CEO, Johnson said. “That opens up 500 million or more active users of those apps that will have access to Starbucks.”

The partnership results are something for us to look forward to in the future.

2. Amplifying their core, high-growth businesses

In some region, they have partially licensed model and other regions they have a fully company-owned model. Starbucks aims to fine tune these business models better according to the geography to ensure that they will be more effective. What do Starbucks define as effective remains vague based on their annual reports and letter to shareholders.

Their Teavana’s online store and retail stores have closed. They plan to shift their focus to sell Teavana through their channel partners e-commerce platforms instead of doing it on their own.

Starbucks’ business drivers would be from their China expansion because that is where they are investing at and where they believe the growth will be.

So overall, Starbucks said that their main business drivers moving forward is number 1, growth via China and number 2, amplifying their core, high-growth business via a combination of fine tuning their combination of licensed to company-owned stores and making more money from their Teavana brand.

With regards to Starbucks’s fundamentals as a company, here are the facts:

1. Its EPS grew from 0.93 to 2.16 in a span of 5 years, CAGR of 18.36%. This is a high rate of annual growth for their earnings and if their expansion into China succeeds, this CAGR can be maintained at least or even grow further.

2. It has an industry-leading return on equity of 88.39% and a return on invested capital of 43.85%. This shows that they are very good at generating returns using both equity and debt.

3. Their debt repayment ability is marvelous with a long-term debt to net income ratio of 0.87. This means that in a span of one year, they are able to pay off all their long-term debt with their net income.

And a quick discounted cash flow valuation will show that:

Starbucks free cash flow grew from $919.10 m in June 2011 to $2.618 b in June 2018. A CAGR of 16.13%. If we assume that Starbucks will grow its free cash flow at a higher than average rate of 20% over the next 4 years (due to a potential success in expanding in China and the growth of their Teavana brand) and down to 10% due to saturation for another 5 years and using a 4% perpetual growth rate with 10% cost of equity, we get a value of $67.38 per share and utilizing 15% margin of safety, we get $57.27 as the value for Starbucks’s stock. This scenario is assuming that Starbucks will continue growing at a higher rate for the next 4 years as compared to the last 5 years. If we are to be more conservative, we can instead use a higher margin of safety of 20% instead of 15%. Or you can adjust it based on your own expectations, analysis and assumptions.

Actionable steps for you:

1. Do your own research on Starbucks’s stocks by reading into their annual report to see their plans moving forward.

2. If you like Starbucks, reflect why. What about their brand that you like? or dislike?

3. If you need more help, I can teach you privately. Indicate your interest at valueinvestingmentorship.com.

Disclosure: I own shares of and is long on Starbucks (NASDAQ: SBUX).

Disclaimer: The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

I hope you have enjoyed reading the article.

Good Result and Yet The Stock Fell 10+% – GameStop’s So Unloved

The stock hit fresh near 13 year low despite the company doing pretty well during the earnings call on 28 March 2018. It closes at 10.39% down. It is not an easy day for any GameStop holders (except the short sellers), from my end, I am thinking where I could have gone wrong – or is the market wrong. I am more than willing to […]

Here’s My Thoughts on GameStop’s Q417 Earnings Results (Released 28/3/2018)

Despite the increase in sales and the beat in earnings from analyst estimates, their profits are still down 11.4% year on year basis on the adjusted diluted EPS portion (from $3.77 to $3.34). However, $3.34 is near the top of the management guidance for FY2017 – and the focus on improving the trade awareness where […]

5 Reasons Why Having The Long-Term View is Vital in Stock Investing

Having a long-term view is important in stock investing. And the reason is not just because many of the world’s most successful and richest investors such as Warren Buffett and Seth Klarman say so. “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” – Warren Buffett […]

Is GameStop Doomed? I Visited Their Stores in NY to Find Out

As of the market close on 11 January 2018 at $19.96, I am at a 7.81% paper gain excluding of realized gains I received via dividends and options premium. And GameStop consists of 30.80% of my portfolio – second on the list – with the first being Qualcomm at 40.60% of my portfolio. Naturally, going down to GameStop stores in New […]

Last day of 2017 – A Review of My Investment Journey So Far

This year, the stock market rally would have given many investors with a good profit – the Dow (top 30 company in the united states stock market) up 25%, S&P 500 (top 500 company in the united states stock market) up 19% and Nasdaq are up 28% this year. And I think it is maybe time to be cautious. Or I should say, cautiously […]

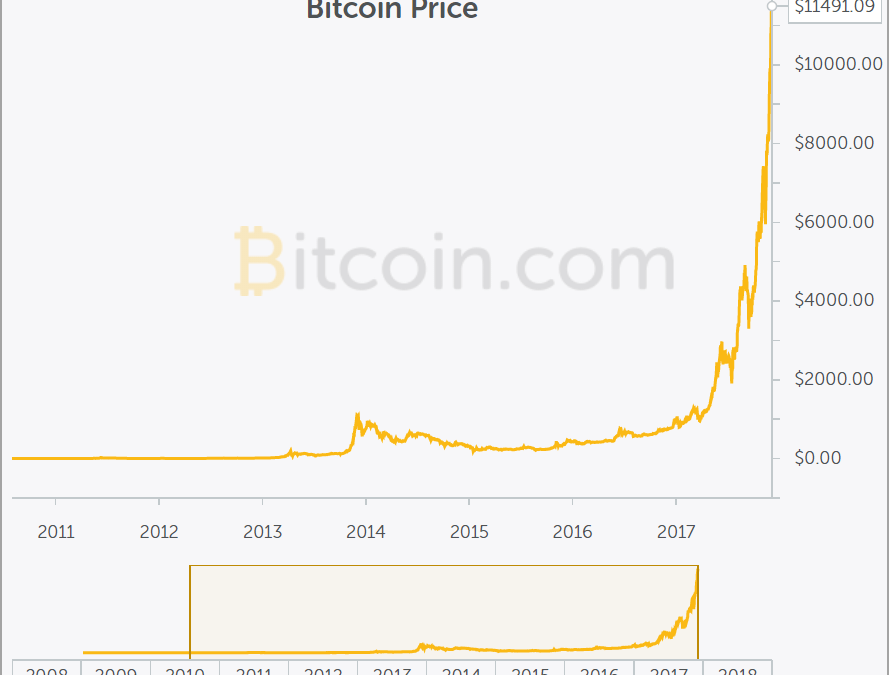

Here’s My Opinion on Bitcoin

Bitcoin is a currency that was founded/discovered pretty recently in 2009 by a person (still unknown) using the alias Satoshi Nakamoto.The good thing about transacting using Bitcoin is that there will be no middleman required to do the transacting. There is also no fees tagged to transacting with Bitcoin and no requirements […]

What is moat in Warren Buffett’s terms & why it’s important

Moat is important because it protects a company from losing their market share easily which will erode its earnings power over time. This is important for us as investors because we would want the company we invest in to have its earnings grow over time – then the share price will follow – and not the other way round. So, we […]

GameStop Q3 17 Earnings — Glad Going Against The Crowd Was Right

25% of their stores have already been turned to GameStop plus format which is a 50–50 combination of games and collectibles. What is interesting here is that despite lesser space to put video games, they actually see an increase in video games sales. This got to do with the new types of customers that these […]

Is Snowflake (NYSE: SNOW) Worth Investing? Here Are My 5 Takeaways

Snowflake does cloud computing that implements a variable pricing model, which can be at times more attractive than fixed packages […]

Nasdaq Is Officially In A Correction Territory: What Is Next?

The adage that “In the short run, the market is a voting machine but in the long run, it is a weighing machine.” by Benjamin Graham could not be more true over the past few days. As of 9 September 2020, […]

My 3 Thoughts on Yesterday’s Deepest US Market Decline Since June

Yesterday (3 September 2020), the US market had its deepest one day decline since June. The S&P 500 and Nasdaq had their deepest declines since June 11 and for Dow, it was their biggest decline since June 26 […]

Will The Stock Market Crash One More Time in 2020?

My Bet: In 2020, The Stock Market Will Not Crash Again. Yes, it is hard to predict where the stock market is heading in the short term. But my bet with regards to virus-related concern is that I do not think that we will crash again back to March-April Lows in 2020 just because of it […]