Stock analysis/investing

Here Are My Quick Analysis on Palantir Technologies Stock (June 2021)

19 June 2021

In this “Quick Analysis” series, I will share my general quick views on different types of companies (you can think of it as a simplified summary). These are just my views and are not meant to be financial advice and you do not have to agree, they are purely for educational purposes only (read our full disclaimer here). If I am vested in the company as of the time of writing, I will also disclose it.

To be updated on all my latest articles, join my free Telegram Channel.

What Does Palantir Technologies Do?

source: Palantir

Palantir is a company that provides large organizations with a minimum of $500 million in revenue the ability to manage large data sets to gain insights and drive operational outcomes.

It was founded back in 2003 and its Gotham software was released in 2008. Gotham is focusing on the government intelligence and defense sector.

It was only in 2016 that Palantir came out with Foundry – a software platform with the intent to become the data operating system for companies and industries.

Palantir would be considered a fast-growth company with a yearly revenue growth rate of upwards of 40%.

Does Palantir Have A Competitive Advantage?

In my view, by starting work with the U.S. government through its Gotham software, they do have a reputation for trust. And that trust leads to brand recognition and helps its Foundry software too, which focuses more on commercial customers.

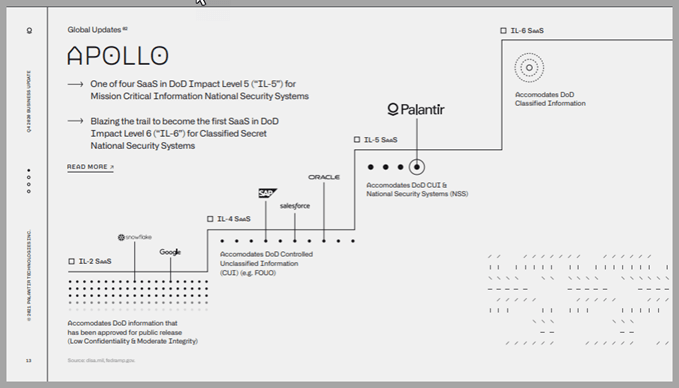

Source: Palantir Q420 presentation

Palantir’s Apollo system is differentiated in a way that it’s able to handle Mission Critical Information National Security Systems.

Apollo is the engine behind Gotham and Foundry, a continuous delivery system that allows Palantir customer to have their software run in purpose-built government or classified clouds that live separately from a standard public cloud.

They are aiming to go towards level 6 in the future which is for Classified Secret National Security Systems.

Source: Palantir Q420 presentation

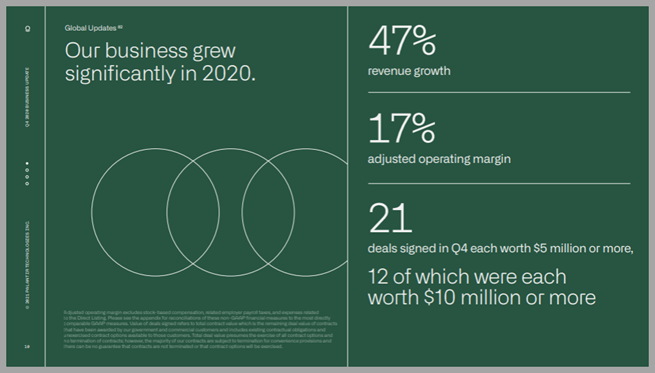

So far, Palantir has been able to translate its technical prowess into solid business results which delivered nearly 50% revenue growth in 2020.

12 of the 21 deals signed in Q4 of 2020 were worth $10 million or more.

Overall, my view is that Palantir does have signs of some competitive advantage in terms of switching costs and branding. However, whether it is unassailable for the next 10 years or so is less clear to me.

How is The Management Quality of Palantir?

The CEO of the company, Alexander Karp co-founded Palantir with Stephen Cohen (current company president and secretary). Peter Thiel is the chairman of Palantir since 2003.

With three different share classes, class A (with one vote), class B (with 10 votes), and Class F (variable number of votes), it allows the founders the ability to control nearly 50% of the total voting power.

So far, the management has done a good job executing well with Palantir’s enviable position in the big data management industry, I think they are pretty decent so far.

How Is The Valuation Range For Palantir Like?

Source: Ycharts

Based on a simple EV to Revenue, Palantir’s valuation is on the high side. Palantir’s EV to Revenue is at 37.87 as of 19 June 2021. Although it is lower than its historical EV to Revenue peak at around 56 back in January 2021, on absolute terms, it is still high for me.

Simply put, even if Palantir’s revenue doubled, its EV to Revenue will still be around the 18-19 range.

In Conclusion

I like Palantir’s business quality and management’s execution so far. It is a pretty special company.

However, personally, I’d like to wait for a bigger margin of safety before I will consider initiating a stake.

For now, it is in my watchlist of quality companies I’d like to own one day.

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Disclosure:

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Learned something from this article?

Share it 🙂

Chris Lee Susanto

Founder, investment blogger, and editor of this value investing x business-like stock investing blog Re-ThinkWealth.com.

Chris is a big proponent of business-like stock investing. He invests in companies where there is value to be found, be it a turnaround, depressed, value, or quality growth company (compounders). He either buys the stock outright or he profits through selling put or selling call options – or buying call options (buying and selling options are especially dangerous for those who do not know how to properly execute it).

Some of the places where Chris has been invited to speak or have added value as a mentor or writer includes Singapore Polytechnic, SMU Institute of Innovation and Entrepreneurship (IIE), Dollars and Sense, The New Savvy, Value Walk Blog, Investment Moats, NUS Tembusu College, NUS Investment Society, CGS-CIMB Singapore, Singapore Financial Conference by NTU IIC, The Financial Coconut Podcast, Money FM 89.3 and Internationally in Myanmar.

Being a full-time investor, Chris knows that he did not beat the S&P 500 return so far (as of the time of this writing) by listening to stock tips. So, when he teaches, he also doesn’t believe in giving stock tips as it is not sustainable for you in the long run.

As of now, Chris’s focus is on setting up a MAS Licensed Fund in the future with the goal to beat the market over the long run. Feel free to join his FREE investment telegram channel here.

Don’t Leave First, Read Also:

Sustainability of Dividends

First, we must understand that business conditions are dynamic. Occasionally, different cycles will cause earnings to fluctuate up or down and it affects the business’ ability to pay out dividends. As investor, we must never have the expectations for dividends to remain the same forever […]

The Role of Synergies in M&A; Reliable to Warrant a Premium Over Market Value?

Today, I want to talk about the role of synergies in M&A. And is it reliable enough for companies to pay a premium over market value because of it?

I for one think that this is a very important topic to discuss for both investors and business people alike. Simply because people tend to be over optimistic of the future and […]

Warren Buffett Often Talks About Intrinsic Value: What is it?

Warren Buffett often talks about intrinsic value. But what exactly is an intrinsic value? Knowing what is intrinsic value is the FIRST step for any aspiring investors who want to be a practitioner of value investing. UNDERSTANDING what is intrinsic value is, of course, the second step for aspiring value investors. Because […]

My Thoughts on Qualcomm Q1 2018 Results

Yesterday’s was Qualcomm’s release of its quarter 1 2018 results. You can view its SEC filing here. It is for the quarterly period ended March 25, 2018. A short background, Qualcomm is simply the company behind most of the smartphones that we are using – in terms of the chips or you can call it, the “brain” […]

Good Result and Yet The Stock Fell 10+% – GameStop’s So Unloved

The stock hit fresh near 13 year low despite the company doing pretty well during the earnings call on 28 March 2018. It closes at 10.39% down. It is not an easy day for any GameStop holders (except the short sellers), from my end, I am thinking where I could have gone wrong – or is the market wrong. I am more than willing to […]

Here’s My Thoughts on GameStop’s Q417 Earnings Results (Released 28/3/2018)

Despite the increase in sales and the beat in earnings from analyst estimates, their profits are still down 11.4% year on year basis on the adjusted diluted EPS portion (from $3.77 to $3.34). However, $3.34 is near the top of the management guidance for FY2017 – and the focus on improving the trade awareness where […]

5 Reasons Why Having The Long-Term View is Vital in Stock Investing

Having a long-term view is important in stock investing. And the reason is not just because many of the world’s most successful and richest investors such as Warren Buffett and Seth Klarman say so. “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” – Warren Buffett […]

Is GameStop Doomed? I Visited Their Stores in NY to Find Out

As of the market close on 11 January 2018 at $19.96, I am at a 7.81% paper gain excluding of realized gains I received via dividends and options premium. And GameStop consists of 30.80% of my portfolio – second on the list – with the first being Qualcomm at 40.60% of my portfolio. Naturally, going down to GameStop stores in New […]

Last day of 2017 – A Review of My Investment Journey So Far

This year, the stock market rally would have given many investors with a good profit – the Dow (top 30 company in the united states stock market) up 25%, S&P 500 (top 500 company in the united states stock market) up 19% and Nasdaq are up 28% this year. And I think it is maybe time to be cautious. Or I should say, cautiously […]

Here’s My Opinion on Bitcoin

Bitcoin is a currency that was founded/discovered pretty recently in 2009 by a person (still unknown) using the alias Satoshi Nakamoto.The good thing about transacting using Bitcoin is that there will be no middleman required to do the transacting. There is also no fees tagged to transacting with Bitcoin and no requirements […]

What is moat in Warren Buffett’s terms & why it’s important

Moat is important because it protects a company from losing their market share easily which will erode its earnings power over time. This is important for us as investors because we would want the company we invest in to have its earnings grow over time – then the share price will follow – and not the other way round. So, we […]

GameStop Q3 17 Earnings — Glad Going Against The Crowd Was Right

25% of their stores have already been turned to GameStop plus format which is a 50–50 combination of games and collectibles. What is interesting here is that despite lesser space to put video games, they actually see an increase in video games sales. This got to do with the new types of customers that these […]