Is SIA Shares Worth Buying? Here Are My Thoughts (August 2020)

22 August 2020

Think About How SIA Was When Times Was “Normal”

Before we got into this COVID-19 mess, SIA is already not a great business to own even when times were “normal.”

Source: Morningstar

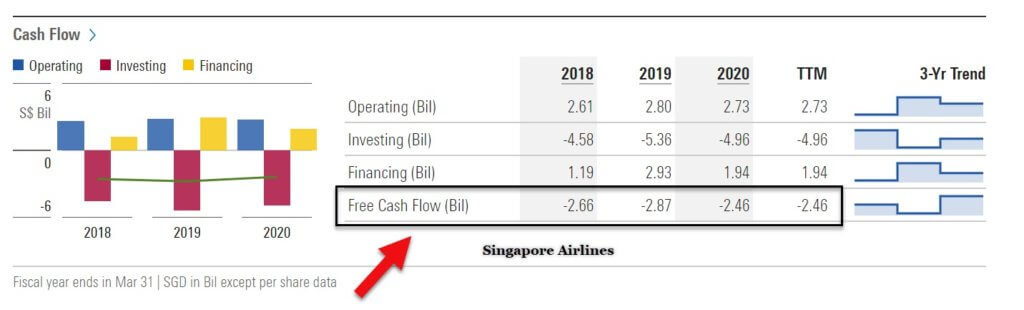

All of us know that the airline business is a very capital intensive business. For SIA, their free cash flow has been negative most of the time in the last five years.

That means that after deducting their operating cash flow for capital expenditures, they are left with negative cash flow.

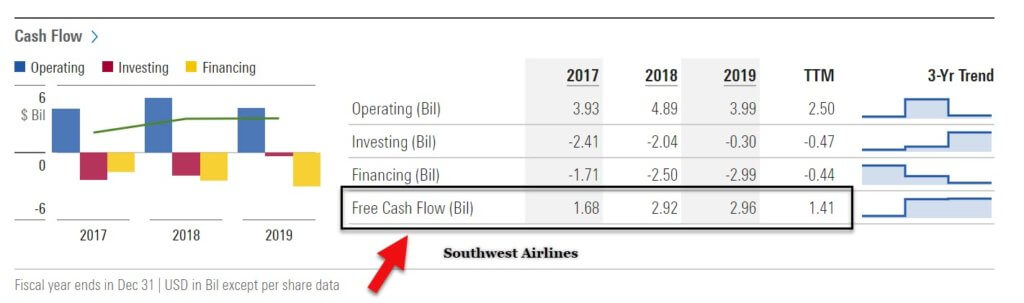

Source: Morningstar

The truth is very few airlines in the world can consistently produce a positive and growing free cash flow. Southwest Airlines, based in the US is an exception, as you can see from the chart above.

Southwest is able to do it because they are able to streamline their operations well – combined with an amazing working culture inside the company.

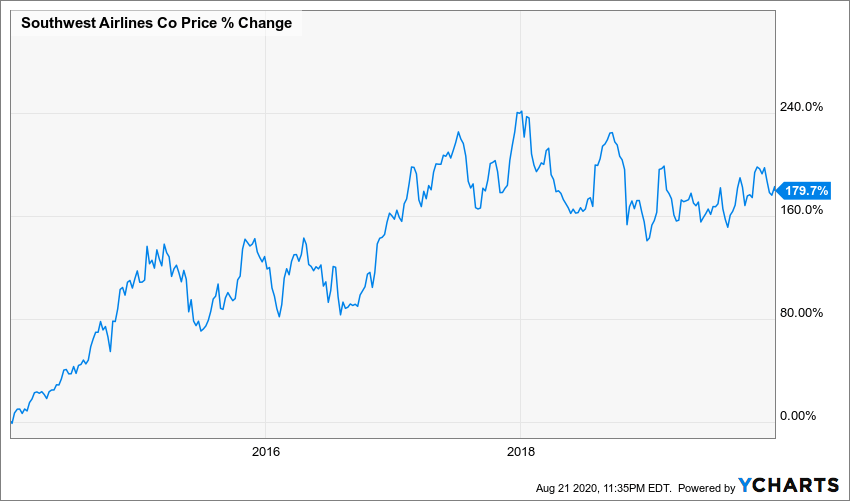

Source: Ycharts

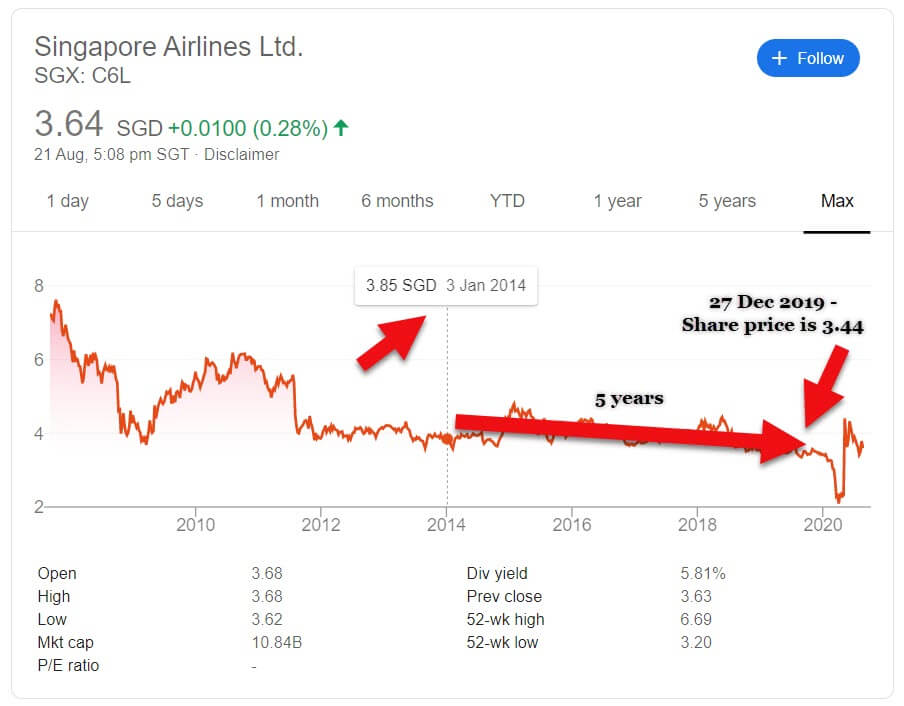

Source: Google

And based on the stock price chart above from 2014-2019, you can see that Southwest has been a better business (and therefore, stock) to own over the last five years as compared to SIA.

Based on the same 5-year period, while Southwest is up 179.7%, SIA is down 10.65%.

Yes, although we cannot compare directly as they operate in different markets but as investors, we still can choose where to allocate our capital.

And as you can see, the stock price reflects the strength of the business that we buy.

My fundamental investing philosophy is always, “if the business does well, the stock price will likely do well too.”

Hence I would say that as an airline business, I’d rather own Southwest as opposed to SIA.

See also: Our free telegram channel. We post daily.

Huge Dilution in A Competitive Industry

SIA is in such a dire state that due to the fund-raising they did, their issued share capital could potentially be diluted by more than 3 times its original share capital.

That simply means that if last time they earn $0.30 per share, and if we assume they manage to reach back to the previous net earnings, its earnings per share will be down to about $0.10 due to the dilution.

That is such a huge potential dilution in which the full effect we will only know maybe in 2021.

Great Branding, Bad Business Economics

Image Source: Wikipedia

SIA is an iconic brand. They are consistently ranked as the best airline brand in Asia.

In fact, in 2018, they were ranked as the most positively perceived brand by Singaporean consumers, based on a study by British-based independent research firm YouGov.

However, it’s economics paints a different picture.

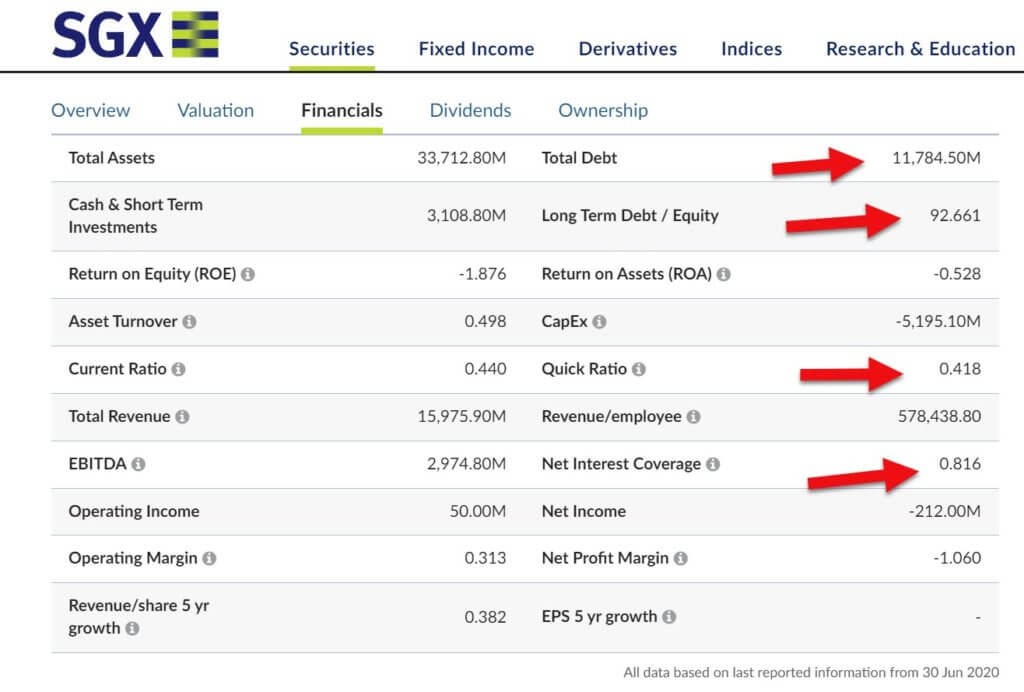

Source: SGX

Based on current data as of 30 June 2020, they are in a dire state. Their debt is more than 92 times as much as it’s equity.

They cannot even cover the current interest with net interest coverage of 0.816.

And their quick ratio is currently below 1. This means that they cannot meet their current short-term obligations with it’s most liquid assets.

Government Support is High for SIA

PM Lee said in April 2020 that the Singapore government is determined to see SIA through the Covid-19 crisis.

PM Lee said that no effort will be spared to ensure that SIA and the aviation sector see through the current crisis because it is a strategic sector.

“SIA has always flown Singapore’s flag high all over the world and made us proud. We will spare no effort to enable it to do so again.”

Share Price Might Go Up Due to Emotional Hype But Might Not Last Due to Lack of Growth

Due to government support, I do not think that SIA will go under.

When the vaccine is found, I think there might be an initial surge for its share price due to a possible return of flying.

But even before COVID-19, SIA is already struggling as a business with high capital expenditure.

Management has not seemed to have found a way to compete effectively in this competitive airline industry filled with other choices.

Also read: The Eight Accounting Fraud or Red Flag Signs To Look Out In Stocks

In Conclusion

The brand alone cannot be constituted as a good investment and a good business. They have to provide a solid return for shareholders.

Airlines like Southwest are able to have positive and growing free cash flow in normal times because they are able to streamline their business very well.

SIA on the other hand would need to innovate its business and give better returns to shareholders if they were to survive and grow.

The airline industry is already so tough, the COVID-19 pandemic would have been a nail in the coffin for SIA if not for government support.

Based on current information and my view as of August 2020, I Would Categorize SIA Stock as a speculation, not investment.

Read next: Kodak Stock is Up Over 1,400% in Two Days. Does It Make Sense?

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Chris Lee Susanto

Founder of the value investing blog Re-ThinkWealth.com (if you type “value investing blog” in Google, his blog is likely the first one). Being a full-time investor himself, Chris knows that he did not beat the S&P 500 return so far (as of the time of this writing) by listening to stock tips. So, when he teaches, he also doesn’t believe in giving stock tips as it is not sustainable for you in the long run. He will teach you how to make your own intelligent decisions with his 4M1S framework. Feel free to also join his free investment telegram channel here.

More from Chris

2 Billion Users ( > China Population): Why I Am Long on Facebook Stock

But over time, I would like to invest in good businesses at a fair price instead of continuing to invest in an OK business at a cheap price. Due to Facebook’s recent drop in its share price, I took a stake in Facebook during the past few months and right now, it consists of about a quarter of my portfolio.

Part 2 of 2: The Limitations of The Black Scholes Model (by Warren Buffett)

Before we touch on the limitations of Black-Scholes. let’s do a brief recap. In the first part of the article, we talked about how the Black-Scholes model is used to price options. They are commonly known as the options pricing model to know the fair price of the put or call options. There […]

Part 1 of 2: Here’s How to Use The Black-Scholes Model to Price Options

The Black-Scholes model was first developed by three economists. Two of them – Myron Scholes and Robert Merton – received a Nobel prize in 1997 for their work in this model. The Black-Scholes model is also commonly known as the options pricing model. And as the name indicates […]

New Logo Design for Re-ThinkWealth (Value Investing Blog)

The above image is how the new Re-ThinkWealth logo looks like. As you might have noticed, it is a combination of “R” and “W” which stands for Re-ThinkWealth. At the same time, the shape of the logo embodies the resemblance of how a stock market will behave. The stock market goes down and up […]

Here Are My Reflections After 3 Years 7 Months in The Stock Market

So basically, I knew that if I cannot beat the S&P 500 return over the long run, it’s better if I just invest in the S&P 500. While the S&P 500 practices in a huge diversification of 500 big companies listed in the U.S., my U.S. portfolio practices concentration of ideas in which I am most certain about […]

10 Reasons Why We Should Rethink How to Build Our Wealth

I am 25 years old this year and I am always fascinated by how a change in our thinking can result in a huge change in our wealth. I am convinced by the notion that how we think creates the wealth that we have. And writing has been an integral part of it all because it gives me an avenue to pen […]

Here’s My Quick Thought on Starbucks Stock

Starbucks is a company that needs not much introduction. I am sure that most of us have drunk Starbucks coffee before. And many of us have studied or did some work or caught up with a friend there. Starbucks is a familiar company that is in almost every airport around the world. Their story though started back in Seattle […]

Theranos Incident Shows Why It’s Dangerous to Invest Based on Hopes And Dreams

I do admit that a business is nothing without goals, hopes, and dreams. A successful business requires the founder to have a vision and to be able to turn that vision into reality. A successful business is one that has managed to turn hopes and dreams into reality. And by reality, I mean cash. Cold hard cash. Think Apple, […]

Qualcomm Will Not Supply Apple’s 2018 iPhones – And That is Okay (Q3 2018 Results)

Qualcomm is the company that supplies phone makers like Samsung, Xiaomi, Huawei, Apple chips so that their phone can be a “smartphone.” Different chip suppliers will have different chips. And just by having a different chip, the performance of the phone can vary greatly. I am vested in Qualcomm since 24 January 2018 at an average price of about $53. Here are the […]

Thinking of Betting in World Cup 2018 or Investing in Stocks? Read this first.

1. Soccer is very unpredictable – The ball is round. as of 28 of June 2018 in the qualifying round, Germany is out of the world cup. Who could have predicted that? Not UBS and Goldman Sachs, that’s for sure, who predicted Germany would win the cup and go to the final respectively. 2. The more the potential payout, the lesse […]

24/3/2017 Was The First Time I Bought GameStop: About Time a Private Equity Firm is Interested in it!

Because the fact is that today, it is reported by Reuters that GME has received buyout interest and is holding talks with private equity firms about a potential transaction. Seems like Sycamore Partners – one of the PE firms that have expressed interest in GME agrees with my conclusion and analysis that GME is mispriced […]

Sony – Deep Value?

Sony is at an inflection point after years of restructuring. Having shed and restructured loss-making business units, it comfortably exceeded its 2014 medium-term plan to deliver an ROE of 10% and operating profit of JPY500bn in FY17. The company is seeing a number of tailwinds for games, music, and the semiconductor segments […]