Options

Part 2 of 2: The Limitations of The Black Scholes Model (by Warren Buffett)

Chris Lee Susanto, Founder at Re-ThinkWealth.com

24 October 2018

This is the second of the two-part article series on The Black-Scholes model. In the first part, we had covered how we can use The Black-Scholes model to price options and in this second part, the limitations of the Black-Scholes Model (including Warren Buffett’s opinion on it).

Summary

- The first limitation is that the original Black Scholes model does not take into account the dividends of stocks in valuing the options.

- The second limitation of the Black-Scholes model is one that is pointed out by a person I greatly admire, Warren Buffett himself. It got to do with the Black-Scholes limitations of valuing long-dated options.

A Brief Recap of The Black-Scholes Model

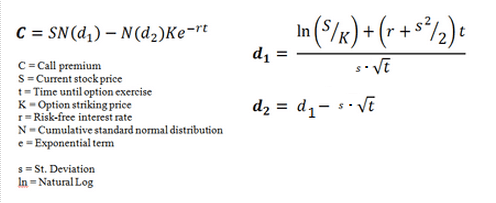

Before we touch on the limitations of Black-Scholes by Warren Buffett, let’s do a brief recap. In the first part of the article, we talked about how the Black-Scholes model is used to price options. They are commonly known as the options pricing model to know the fair price of the put or call options. There are six variables that are taken into account in calculating the options value. The six variables are time to expiry, the underlying stock price at the time, volatility of the underlying stock, type of option, strike price and risk-free rate. So this means that the value derived using the Black-Scholes model got to do with the inputs that are being put into the model – pretty straightforward.

Does the Black-Scholes Model Make Sense?

First, I believe that the Black-Scholes model makes good sense. Based on the formula of the model, it makes good sense that when the underlying price increases, the cheaper the options will be if it is a put option. And more expensive if it is a call option. So depending on whether you are a seller or a buyer of these options, the value of your options will increase or decrease accordingly.

For example, the buyer of the put options has the right to sell the stock at a predetermined strike price. If prices keep on going up, the put options contract logically become less of a value. Because why would the put options buyer want to sell its stocks at the lower strike price of the put options if selling at the market can fetch a higher price? And in this scenario, the seller of the put options who had received premiums/payments from the buyer of the put options will not need to be obliged to buy the stocks from the buyer of the put options. Hence, the put options become worthless on expiry if the price keeps on going up. Thus, put options value decreases when the underlying price of the stock keeps on going up.

Based on the formula of the model, it also makes good sense also that the greater the volatility, the higher the options price/value will be. Higher uncertainty will result in higher premiums due to higher perceived risks. It is the way it should be. It makes good sense too. Bonds by the government has less volatility so we are compensated lesser. As compared to if we invest in say stocks that have higher volatility and higher uncertainty.

The Original Formula of the Black-Scholes Model

To recap, this is the original formula for Black-Scholes:

Source: Investopedia

The original Black-Scholes formula takes into account the current stock price, time to expiry, options strike price, risk-free interest rate and the cumulative standard normal distribution which is known as the implied volatility or simply how volatile the stock is.

The Limitations of the Original Black-Scholes Model (Dividends Not Accounted for)

Here is the first limitation that I came out with: The underlying price of a stock will usually decrease accordingly by the amount of cash dividend declared on the ex-dividend date of a company. So, dividends do play a role too because it affects the underlying price of a stock. But in the Black-Scholes model, it makes the assumptions that no dividends are paid out during the life of the options. This means that a company that pays a lot of dividends will usually have the stock price decrease in relation to it. If during the course of the options, the company pays those dividends, the put options should be worth more and the call options should be worth less. But the original Black-Scholes model does not take those into dividends into account – and we need to adjust it accordingly. We can do that by subtracting the present value of the upcoming dividends of the stock during the life of the options from the current stock price – in which we then input the subtracted value to the original Black-Scholes model.

The Limitations of the Original Black-Scholes Model (by Warren Buffett)

The second limitation of the Black-Scholes model is one that is pointed out by a person I greatly admire, Warren Buffett himself. It got to do with the Black-Scholes limitations of valuing long-dated options.

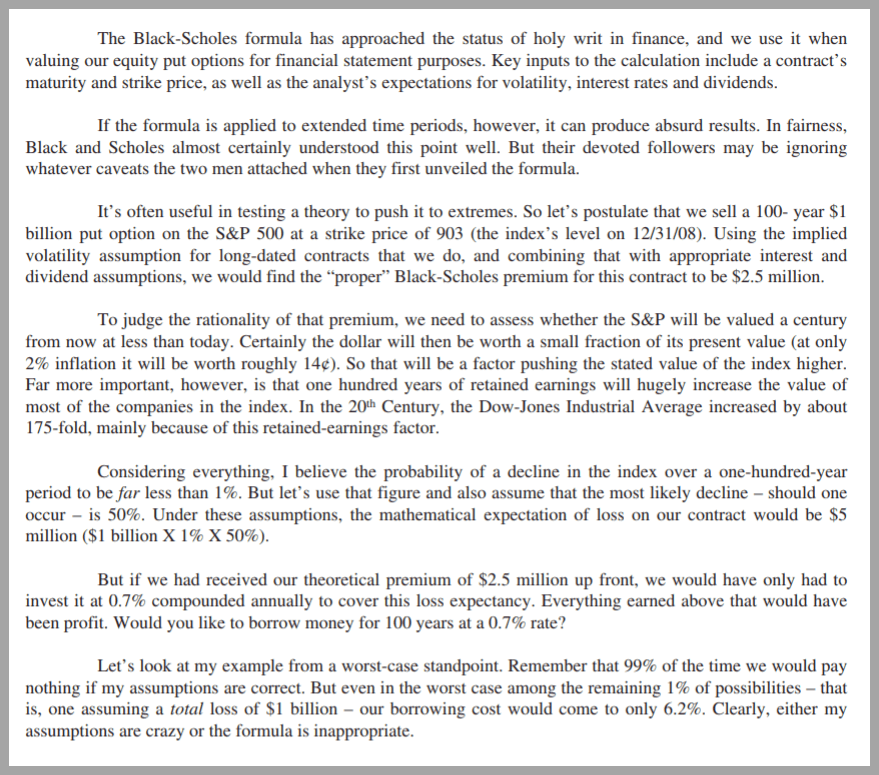

Source: Berkshire Hathaway 2008 Annual Report

Based on Warren Buffett, while the Black-Scholes model has been the widely used model to value equity put options, he thinks that there are limitations to it – when the model is applied to an extended time period, they can produce absurd results. So Waren Buffett is saying that the Black-Scholes model is bad at valuing long-dated options.

Warren Buffett also gives an example to explain this theory of his by pushing it to the extremes as you can see from the image screenshot above. He gave the example of selling a 100-year-old $1 billion put option on the S&P 500 at a strike price of 903 which was the index’s level on 31 December 2008. Using the “proper” Black-Scholes model at the time, he will get a premium of about $2.5 million. And he sees that the expected loss on the contract would be $5 million (by taking $1 billion which is the contract value of the options times a 1% chance that 100 years from now the S&P 500 is going to be worth less and times it by 50% which is the chance of that decline).

Using this example, Warren Buffett said that if he received the $2.5 million up front, he only need to invest and get 0.7% annually for the next 100 years to cover the expected loss. So he said that this is akin to borrowing the money which is $2.5 million for a rate of 0.7% annually. Even at a total loss of $1 billion, the “borrowing cost” will only be about 6.2%.

For Warren Buffett personally, he has made use of these kinds of market inefficiency to sell put options when the volatility is high so that he was able to get more premiums/cash flows. And then he uses these premiums/cash flows to invest and get returns.

“Our put contracts total $37.1 billion (at current exchange rates) and are spread among four major indices: the S&P 500 in the U.S., the FTSE 100 in the U.K., the Euro Stoxx 50 in Europe, and the Nikkei 225 in Japan. Our first contract comes due on September 9, 2019 and our last on January 24, 2028. We have received premiums of $4.9 billion, money we have invested. We, meanwhile, have paid nothing, since all expiration dates are far in the future. Nonetheless, we have used Black-Scholes valuation methods to record a yearend liability of $10 billion, an amount that will change on every reporting date. The two financial items – this estimated loss of $10 billion minus the $4.9 billion in premiums we have received – means that we have so far reported a mark-to-market loss of $5.1 billion from these contracts.” – Warren Buffett

While Warren is able to utilize the volatility of the stock market to get more premiums, he criticizes Black-Scholes as being limited simply because of the financial reporting regulation that forces him to use the Black-Scholes.

Disclaimer:

The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Is Bitcoin Worth Investing in 2020? Here’s My Quick Thoughts

Bitcoin can be considered the world’s best-known cryptocurrency. Today is the 21st of November, 2020 and coincidentally, Bitcoin supply is also […]

Is Oculus Owned by Facebook? Yes And Here’s Why It’s Great

I have been wanting to buy the Oculus Quest for the longest time. A few years ago, when Oculus first came out with The Oculus Quest, I wanted to […]

Election Results: Biden or Trump? Here’s Why To The Stock Market, It Doesn’t Matter

Based on the current trend of the mail-in ballots, it seems likely that Biden is going to be the victor of the US election in

Why Netflix Raised The Price of It’s U.S. Subscription And Is It A Mistake?

Netflix currently has more than 65 million U.S. subscribers and about 195 million paid […] Their last hike for the U.S. price was in January 2019.

The Ultimate List of Investment and Finance Blogs/Websites in Singapore

Being an avid follower of many investment and finance blogs or websites in Singapore, I thought why not I create an

My 5 Key Takeaways From SPH FY2020’s Earnings

1. Long-Term Challenge With Media Division The first thing that comes to mind when we hear SPH is the newspaper. And newspaper makes money through […]

8 Value Investing Lessons From Beating The S&P 500 Return So Far

There are many value investing lessons that I have learned throughout these past five, six years. For today, I thought to share with you eight of the value investing lessons […]

Here Are My Five Key Takeaway From Tesla 2020 Battery Day

Elon Musk is a fantastic marketer and an innovative entrepreneur. I have been curious about the Tesla story for quite some time. And here are my five key takeaway from Tesla 2020 […]

Is Snowflake (NYSE: SNOW) Worth Investing? Here Are My 5 Takeaways

Snowflake does cloud computing that implements a variable pricing model, which can be at times more attractive than fixed packages […]

Nasdaq Is Officially In A Correction Territory: What Is Next?

The adage that “In the short run, the market is a voting machine but in the long run, it is a weighing machine.” by Benjamin Graham could not be more true over the past few days. As of 9 September 2020, […]

My 3 Thoughts on Yesterday’s Deepest US Market Decline Since June

Yesterday (3 September 2020), the US market had its deepest one day decline since June. The S&P 500 and Nasdaq had their deepest declines since June 11 and for Dow, it was their biggest decline since June 26 […]

Will The Stock Market Crash One More Time in 2020?

My Bet: In 2020, The Stock Market Will Not Crash Again. Yes, it is hard to predict where the stock market is heading in the short term. But my bet with regards to virus-related concern is that I do not think that we will crash again back to March-April Lows in 2020 just because of it […]

Wait, Wait!

I often share insights that I do not share in this blog over at my Facebook page. Don’t forget to like it before you go!

22.70% vs 15.19%; My Performance vs S&P 500 for Close to 7 Years

In this article, I am going to try to condense what I have reflected on, learned, and applied through […]

3Q 2021 Update to My Carnival Corp Stock Thesis

In June 2021, I wrote that I think Carnival Corp stock is likely going to sail higher in 2021. It took a […]

What is Sustainable Stock Investing and Does It Work?

What is Sustainable Stock Investing? ESG/ sustainable investing is a form of investing that is generally […]

Top 10 Warren Buffett Quotes on Investing | Re-ThinkWealth.com

Is FB a social media company? An advertising company? Or a chat company? Or a VR company? Online […]

Quick Analysis on FB Stock by Re-ThinkWealth.com (August 2021)

Is FB a social media company? An advertising company? Or a chat company? Or a VR company? Online […]

Growth or Value Investing? Why Not Both? – Re-ThinkWealth.com

Both value and growth investing have the same goal: which is to find the biggest opportunity or a gap or […]

Will Carnival Corp Stock Sail Higher in 2021? (June 2021)

“Carnival” based on the Oxford dictionary can also be defined as “a traveling funfair or circus.” The name is apt for a […]

Here Are My Quick Analysis on Palantir Technologies Stock (June 2021)

Palantir is a company that provides large organizations with a minimum of $500 million in revenue the ability to […]