Quick Analysis on FB Stock by Re-ThinkWealth.com (August 2021)

30 August 2021

In this “Quick Analysis” series, I will share my general quick views on different types of companies (you can think of it as a simplified summary). These are just my views and are not meant to be financial advice and you do not have to agree, they are purely for educational purposes only (read our full disclaimer here). If I am vested in the company as of the time of writing, I will also disclose it.

To be updated on all my latest articles, join my free Telegram Channel.

What Does Facebook Do?

Source: Facebook

Is Facebook a social media company?

An advertising company?

Or a chat company?

Or a VR company?

Online shopping company?

Based on their latest 2Q 2021 earnings, they foresee themselves transforming and be known as a metaverse company in the future.

So Facebook wants to be known as a metaverse company!

How will they make money from metaverse? They are looking to make money from selling virtual items in the metaverse along with advertising and other virtual experiences. It will take several years to build this vision of his, based on Mark Zuckerberg.

“A lot of the metaverse experience is going to be around being able to teleport from one experience to another. So being able to basically have your digital goods and your inventory and bring them from place to place, that’s going to be a big investment that people make.” – Mark Zuckerberg

An analyst estimated that Facebook is already spending about $5 billion per year on metaverse-related development.

As of their latest Q2 2021 earnings, they continue to execute well. The daily active users for the Facebook app continue to increase to now 1.908 billion users and the monthly active users are at 2.995 billion users.

Their family of apps daily active people increased to 2.76 billion and monthly active people is at 3.51 billion.

Revenue is the highest it has been in the last 3 years at $29.077 billion in the 2nd quarter of 2021, and so is diluted earnings per share at $3.61.

Cash and equivalents are also very high at $64.08 billion for Q2 2021.

Source: Facebook

The main source of Facebook’s revenue is still advertising, which is up 56% year on year. “Other” sources are gaining traction at $497 million for 2Q 2021.

In the metaverse vision, Mark also foresees that advertising will play a huge role in it (not surprising).

Does Facebook Have A Competitive Advantage?

In my view, Facebook has a clear and durable competitive advantage on three fronts:

1. Network effect

One of the key reasons why Facebook grew so big so fast is due to the “network effect”. It’s a simple principle that the more users Facebook has, the more attractive for others to join as well.

Simply put, Facebook becomes more useful to more people as more people join Facebook and its other apps (WhatsApp, Instagram, etc).

It’s kind of a “winner take all” situation in this social media kind of business.

2. Economies of Scale

Based on Harvard Business Review, Facebook enjoys three advantages over rivals: technological capabilities, economies of scale in its infrastructure, and network effects (our first point). With economies of scale, all of Facebook’s offerings can rely on the same back-end infrastructure system and hence, achieving cost-savings that rivals rarely be able to match.

3. Innovative Management

Facebook’s technological prowess in my view comes from the willingness of the management to fail in the process of innovation and keeping up with the times. There are many examples of companies being disrupted because they were too slow in innovation and therefore succumbs to disruptions from competitors.

Facebook has so far been able to move ahead of the curve (an example is their recent announcements with regards to building a Metaverse company) as well as their continuous investments in building payment and shopping infrastructure in their platforms.

How is The Management Quality of Facebook?

Mark Zuckerberg has proven over time that he is a reliable leader for Facebook.

Reliable not in the sense that there are no controversies. But reliable in the sense that he never fails to continue to try to innovate and be ahead of the curve in terms of what his customers want – and in terms of technological innovation.

“Facebook, it appears, can’t be hurt — not by major ad buyers boycotting its service, not by state and federal investigations, and not even by a pandemic.” – Fortune magazine

Mark has crafted Facebook in a way that there is no single customer concentration. Most of their revenue comes from the small and medium-sized businesses that do advertising on Facebook.

He has also been able to navigate Facebook throughout the different challenges that it has faced over the past few years, privacy issues, state and federal investigations, etc. And in between all those, there are improvements in terms of Facebook’s Oculus Quest 2 offerings and their initiatives on Metaverse.

So overall, the management of FB, in my view has been great. Innovative, flexible and forward looking.

How Is The Valuation Range For Facebook Like?

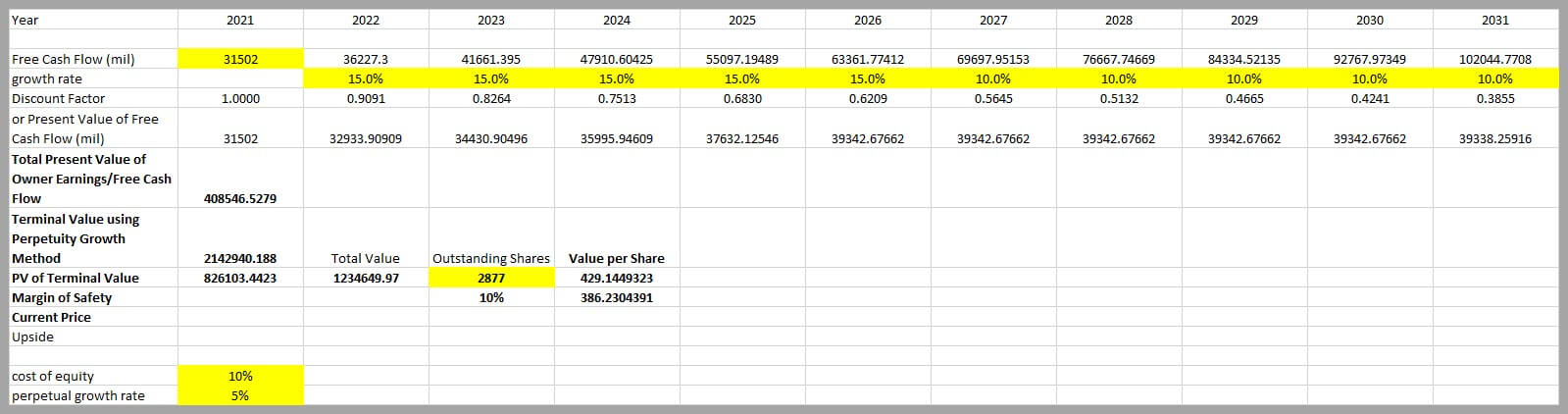

Source: own calculation and model

Facebook’s free cash flow has been steadily going up over the years. Using FB’s latest FCF figure, based on my assumption of a 15% FCF growth rate for the next 5 years followed by 10% for another 5 years before moving towards a perpetual growth rate of 5%, FB fair value is roughly $386.23 after a 10% margin of safety. As of 30 August 2020, FB’s price is at $372.60, which is around its fair valuation based on my assumption.

In Conclusion

I have owned FB for a few years now, first bought it at around $130, $140 region. I view FB as a great company that is in the category of Compounders. A company that continues to evolve and innovate, similar to Microsoft. That is why even in an overvalued region, I would think twice before selling FB.

Some companies are worth paying a premium on and in my view, FB is one of them.

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Disclosure:

I am/we are long FB. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Learned something from this article?

Share it 🙂

Chris Lee Susanto

Founder, investment blogger, full-time investor, and editor of this quality investing x business-like stock investing blog Re-ThinkWealth.com.

Chris started investing in stocks early at age 21 and is a big proponent of business-like stock investing – a mixture of both value and growth investing. He invests in companies where there is value to be found (as long as it is still within his circle of competence), be it a turnaround, depressed, value, or quality growth company (compounders). He either buys the stock outright or he profits through selling put or selling call options – or buying call options (buying and selling options are especially dangerous for those who do not know how to properly execute it).

Some of the places where Chris has been invited to speak or have added value as a mentor or writer includes Singapore Polytechnic, SMU Institute of Innovation and Entrepreneurship (IIE), Dollars and Sense, The New Savvy, Value Walk Blog, Investment Moats, NUS Tembusu College, NUS Investment Society, CGS-CIMB Singapore, Singapore Financial Conference by NTU IIC, The Financial Coconut Podcast, Money FM 89.3 and Internationally in Myanmar.

He is also a practitioner of Transcendental Meditation and Mindfulness practice. He also advocates regular exercise, enough sleep, and nutritious food as part of our lifestyle as an investor.

As of the time of this writing, Chris is focusing on setting up his MAS Licensed Fund with the goal to beat the market over the long run.

Feel free to join his FREE investment telegram channel here to be one of the first to be updated on his new articles.

Don’t Leave First, Read Also:

2 Billion Users ( > China Population): Why I Am Long on Facebook Stock

But over time, I would like to invest in good businesses at a fair price instead of continuing to invest in an OK business at a cheap price. Due to Facebook’s recent drop in its share price, I took a stake in Facebook during the past few months and right now, it consists of about a quarter of my portfolio.

Part 2 of 2: The Limitations of The Black Scholes Model (by Warren Buffett)

Before we touch on the limitations of Black-Scholes. let’s do a brief recap. In the first part of the article, we talked about how the Black-Scholes model is used to price options. They are commonly known as the options pricing model to know the fair price of the put or call options. There […]

Part 1 of 2: Here’s How to Use The Black-Scholes Model to Price Options

The Black-Scholes model was first developed by three economists. Two of them – Myron Scholes and Robert Merton – received a Nobel prize in 1997 for their work in this model. The Black-Scholes model is also commonly known as the options pricing model. And as the name indicates […]

New Logo Design for Re-ThinkWealth (Value Investing Blog)

The above image is how the new Re-ThinkWealth logo looks like. As you might have noticed, it is a combination of “R” and “W” which stands for Re-ThinkWealth. At the same time, the shape of the logo embodies the resemblance of how a stock market will behave. The stock market goes down and up […]

Here Are My Reflections After 3 Years 7 Months in The Stock Market

So basically, I knew that if I cannot beat the S&P 500 return over the long run, it’s better if I just invest in the S&P 500. While the S&P 500 practices in a huge diversification of 500 big companies listed in the U.S., my U.S. portfolio practices concentration of ideas in which I am most certain about […]

10 Reasons Why We Should Rethink How to Build Our Wealth

I am 25 years old this year and I am always fascinated by how a change in our thinking can result in a huge change in our wealth. I am convinced by the notion that how we think creates the wealth that we have. And writing has been an integral part of it all because it gives me an avenue to pen […]

Here’s My Quick Thought on Starbucks Stock

Starbucks is a company that needs not much introduction. I am sure that most of us have drunk Starbucks coffee before. And many of us have studied or did some work or caught up with a friend there. Starbucks is a familiar company that is in almost every airport around the world. Their story though started back in Seattle […]

Theranos Incident Shows Why It’s Dangerous to Invest Based on Hopes And Dreams

I do admit that a business is nothing without goals, hopes, and dreams. A successful business requires the founder to have a vision and to be able to turn that vision into reality. A successful business is one that has managed to turn hopes and dreams into reality. And by reality, I mean cash. Cold hard cash. Think Apple, […]

Qualcomm Will Not Supply Apple’s 2018 iPhones – And That is Okay (Q3 2018 Results)

Qualcomm is the company that supplies phone makers like Samsung, Xiaomi, Huawei, Apple chips so that their phone can be a “smartphone.” Different chip suppliers will have different chips. And just by having a different chip, the performance of the phone can vary greatly. I am vested in Qualcomm since 24 January 2018 at an average price of about $53. Here are the […]

Thinking of Betting in World Cup 2018 or Investing in Stocks? Read this first.

1. Soccer is very unpredictable – The ball is round. as of 28 of June 2018 in the qualifying round, Germany is out of the world cup. Who could have predicted that? Not UBS and Goldman Sachs, that’s for sure, who predicted Germany would win the cup and go to the final respectively. 2. The more the potential payout, the lesse […]

24/3/2017 Was The First Time I Bought GameStop: About Time a Private Equity Firm is Interested in it!

Because the fact is that today, it is reported by Reuters that GME has received buyout interest and is holding talks with private equity firms about a potential transaction. Seems like Sycamore Partners – one of the PE firms that have expressed interest in GME agrees with my conclusion and analysis that GME is mispriced […]

Sony – Deep Value?

Sony is at an inflection point after years of restructuring. Having shed and restructured loss-making business units, it comfortably exceeded its 2014 medium-term plan to deliver an ROE of 10% and operating profit of JPY500bn in FY17. The company is seeing a number of tailwinds for games, music, and the semiconductor segments […]