Growth or Value Investing? Why Not Both?

27 July 2021

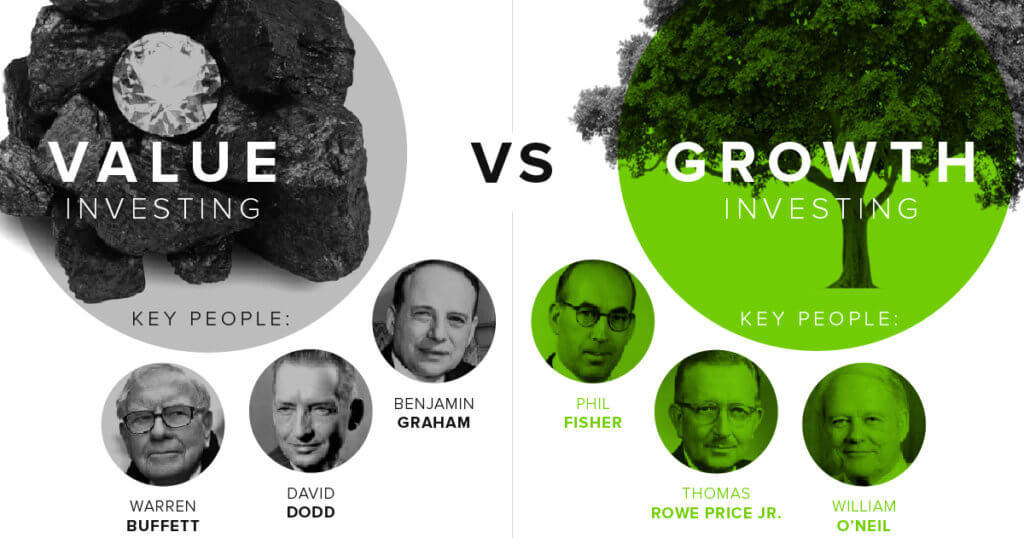

What is The Traditional Definition of Value and Growth Investing?

Image source: Visual Capitalist

In the traditional sense, value investing could be defined as buying a stock that is worth $1 today for 50 cents.

In the traditional sense, growth investing could be defined as buying something that is worth $1 today for $1.50 but it could be worth $6, five years from now.

Based on the Economic Times, growth investing is about finding companies that are expected to grow faster than the market while value investing is identifying companies whose stock prices are lower than their fundamental worth.

Why In My Definition, Value, and Growth Investing Essentially Has The Same Goal

Yes, growth stocks do not normally give out dividends and value stocks have the perception that they give out dividends more often. But value and growth investing have the same goal: which is to find the biggest opportunity or a gap or mispricing in relation to the business value at that point in time.

Both should simply be called “investing” or “business-focused or business-like investing”. Because both growth and value investing are business-focused investing in which an investor buys because they find that the price is cheap or reasonable in relation to what the true value of the business is.

There are more similarities in both the traditional senses of value investing and growth investing than we think.

Be it growth or value investing, like Warren Buffett said, “Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily understandable business whose earnings are virtually certain to be materially higher five, 10, and 20 years from now.”.

In Value or Growth Investing, Patience + Understanding of The Business is Key

In both value and growth investing, if we want to have big money, patience is one of the key ingredients for it. But again it really depends, a turnaround play can take less than 1 year to play out, on the other hand, asset play can take a few years or compounders – we may never want to sell it ever.

Ultimately, based on the type of company, we have to know which companies are worth paying a fair price or even a premium on.

“I don’t want to spend my time trying to earn a lot of little profits. I want very, very big profits that I’m ready to wait for.” – Philip Fisher

And hence, in both value and growth investing, we need to understand the business well enough to know at what price is good enough for us to buy it. So in the future, we have a reasonable probability of selling them at big profits (because we know their fair and overvalued range in relation to the price we bought them at).

I View The Categorization As We Are Either A Value or Growth Investor Limiting

Image source: Pixabay

If we view ourselves as a growth investor, then in the traditional sense, we will say no to value plays, asset plays, and turnaround plays for non-growth companies. And I find that limiting. Because in investing, we need to be flexible and adaptable as long as the opportunities are within our circle of competency, we should hit the big fat pitch that is right in front of us – no matter if it is growth or value plays.

So I propose us simply being an investor. A focused investor that is open to opportunities that we can understand be it in the traditional value plays or growth plays. Not saying no to the other simply because of our limiting categorization of ourselves either as a value or growth investor.

“Value investing, the way I regarded it, will never go out of style because value investing, the way I conceive it, is always wanting to get more value than you pay for when you buy a stock and that approach will never go out of style. Some people think that value investing is you chase companies that have a lot of cash and they’re in a lousy business or something. But I don’t define that as value investing. I think all good investing is value investing, and it’s just that some people look for values in strong companies and some look for values in weak companies, but every value investor tries to get more value than she pays for.” – Charlie Munger

So did Charlie just described value investing? or growth investing? My point is that it does not matter. All good investing should be the same – buying things for less than what we think will be worth in the future.

In Conclusion

Opportunities come from many angles.

A traditional value kind of investor should not overlook growth companies. A growth kind of investor should not overlook traditional value plays.

We should simply invest in anything that we understand and find mispricing in. Categorizing ourselves either as a growth or value investor in my view can be limiting.

I prefer to see myself simply as an investor, business-focused investing, or quality-focused investor.

Because in both the traditional kind of value or growth investing, we ultimately need to find quality in the play, and not speculate.

As long as I understand the business and it is run by great management, selling at a reasonable price compared to the business quality, I am open to investing in it – be it in the so-called value or growth companies. Because in my view, there is value in growth and there is also growth in value.

Based on Merrill, growth stocks tend to perform better when interest rates are falling and earnings are rising. But when economies are cooling, they are likely to be the first punished. While value stocks may do well early in an economic recovery but are typically more likely to lag in a sustained bull market.

Combining both value and growth strategies might give us the potential to gain throughout the economic cycles while staying within our circle of competence.

Even Fidelity suggests that we use a mix of growth and value strategies. They say it is akin to choosing between Batman and Superman. And I would agree. Why not do both?

Disclaimer:

The information provided is for educational and general information purposes only and is not intended to be personalized investment or financial advice. We make no promises as to the accuracy or usefulness of the information we present.

Important: Please read our full disclaimer.

Disclosure:

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Learned something from this article?

Share it 🙂

Chris Lee Susanto

Founder, investment blogger, full-time investor, and editor of this quality investing x business-like stock investing blog Re-ThinkWealth.com.

Chris is a big proponent of business-like stock investing – a mixture of both value and growth investing. He invests in companies where there is value to be found (as long as it is still within his circle of competence), be it a turnaround, depressed, value, or quality growth company (compounders). He either buys the stock outright or he profits through selling put or selling call options – or buying call options (buying and selling options are especially dangerous for those who do not know how to properly execute it).

Some of the places where Chris has been invited to speak or have added value as a mentor or writer includes Singapore Polytechnic, SMU Institute of Innovation and Entrepreneurship (IIE), Dollars and Sense, The New Savvy, Value Walk Blog, Investment Moats, NUS Tembusu College, NUS Investment Society, CGS-CIMB Singapore, Singapore Financial Conference by NTU IIC, The Financial Coconut Podcast, Money FM 89.3 and Internationally in Myanmar.

He is also a practitioner of Transcendental Meditation and Mindfulness practice. He also advocates regular exercise, enough sleep, and nutritious food as part of our lifestyle as an investor.

As of the time of this writing, Chris is focusing on setting up his MAS Licensed Fund with the goal to beat the market over the long run.

Feel free to join his FREE investment telegram channel here.

Don’t Leave First, Read Also:

2 Billion Users ( > China Population): Why I Am Long on Facebook Stock

But over time, I would like to invest in good businesses at a fair price instead of continuing to invest in an OK business at a cheap price. Due to Facebook’s recent drop in its share price, I took a stake in Facebook during the past few months and right now, it consists of about a quarter of my portfolio.

Part 2 of 2: The Limitations of The Black Scholes Model (by Warren Buffett)

Before we touch on the limitations of Black-Scholes. let’s do a brief recap. In the first part of the article, we talked about how the Black-Scholes model is used to price options. They are commonly known as the options pricing model to know the fair price of the put or call options. There […]

Part 1 of 2: Here’s How to Use The Black-Scholes Model to Price Options

The Black-Scholes model was first developed by three economists. Two of them – Myron Scholes and Robert Merton – received a Nobel prize in 1997 for their work in this model. The Black-Scholes model is also commonly known as the options pricing model. And as the name indicates […]

New Logo Design for Re-ThinkWealth (Value Investing Blog)

The above image is how the new Re-ThinkWealth logo looks like. As you might have noticed, it is a combination of “R” and “W” which stands for Re-ThinkWealth. At the same time, the shape of the logo embodies the resemblance of how a stock market will behave. The stock market goes down and up […]

Here Are My Reflections After 3 Years 7 Months in The Stock Market

So basically, I knew that if I cannot beat the S&P 500 return over the long run, it’s better if I just invest in the S&P 500. While the S&P 500 practices in a huge diversification of 500 big companies listed in the U.S., my U.S. portfolio practices concentration of ideas in which I am most certain about […]

10 Reasons Why We Should Rethink How to Build Our Wealth

I am 25 years old this year and I am always fascinated by how a change in our thinking can result in a huge change in our wealth. I am convinced by the notion that how we think creates the wealth that we have. And writing has been an integral part of it all because it gives me an avenue to pen […]

Here’s My Quick Thought on Starbucks Stock

Starbucks is a company that needs not much introduction. I am sure that most of us have drunk Starbucks coffee before. And many of us have studied or did some work or caught up with a friend there. Starbucks is a familiar company that is in almost every airport around the world. Their story though started back in Seattle […]

Theranos Incident Shows Why It’s Dangerous to Invest Based on Hopes And Dreams

I do admit that a business is nothing without goals, hopes, and dreams. A successful business requires the founder to have a vision and to be able to turn that vision into reality. A successful business is one that has managed to turn hopes and dreams into reality. And by reality, I mean cash. Cold hard cash. Think Apple, […]

Qualcomm Will Not Supply Apple’s 2018 iPhones – And That is Okay (Q3 2018 Results)

Qualcomm is the company that supplies phone makers like Samsung, Xiaomi, Huawei, Apple chips so that their phone can be a “smartphone.” Different chip suppliers will have different chips. And just by having a different chip, the performance of the phone can vary greatly. I am vested in Qualcomm since 24 January 2018 at an average price of about $53. Here are the […]

Thinking of Betting in World Cup 2018 or Investing in Stocks? Read this first.

1. Soccer is very unpredictable – The ball is round. as of 28 of June 2018 in the qualifying round, Germany is out of the world cup. Who could have predicted that? Not UBS and Goldman Sachs, that’s for sure, who predicted Germany would win the cup and go to the final respectively. 2. The more the potential payout, the lesse […]

24/3/2017 Was The First Time I Bought GameStop: About Time a Private Equity Firm is Interested in it!

Because the fact is that today, it is reported by Reuters that GME has received buyout interest and is holding talks with private equity firms about a potential transaction. Seems like Sycamore Partners – one of the PE firms that have expressed interest in GME agrees with my conclusion and analysis that GME is mispriced […]

Sony – Deep Value?

Sony is at an inflection point after years of restructuring. Having shed and restructured loss-making business units, it comfortably exceeded its 2014 medium-term plan to deliver an ROE of 10% and operating profit of JPY500bn in FY17. The company is seeing a number of tailwinds for games, music, and the semiconductor segments […]