Options

Part 2 of 2: The Limitations of The Black Scholes Model (by Warren Buffett)

Chris Lee Susanto, Founder at Re-ThinkWealth.com

24 October 2018

This is the second of the two-part article series on The Black-Scholes model. In the first part, we had covered how we can use The Black-Scholes model to price options and in this second part, the limitations of the Black-Scholes Model (including Warren Buffett’s opinion on it).

Summary

- The first limitation is that the original Black Scholes model does not take into account the dividends of stocks in valuing the options.

- The second limitation of the Black-Scholes model is one that is pointed out by a person I greatly admire, Warren Buffett himself. It got to do with the Black-Scholes limitations of valuing long-dated options.

A Brief Recap of The Black-Scholes Model

Before we touch on the limitations of Black-Scholes by Warren Buffett, let’s do a brief recap. In the first part of the article, we talked about how the Black-Scholes model is used to price options. They are commonly known as the options pricing model to know the fair price of the put or call options. There are six variables that are taken into account in calculating the options value. The six variables are time to expiry, the underlying stock price at the time, volatility of the underlying stock, type of option, strike price and risk-free rate. So this means that the value derived using the Black-Scholes model got to do with the inputs that are being put into the model – pretty straightforward.

Does the Black-Scholes Model Make Sense?

First, I believe that the Black-Scholes model makes good sense. Based on the formula of the model, it makes good sense that when the underlying price increases, the cheaper the options will be if it is a put option. And more expensive if it is a call option. So depending on whether you are a seller or a buyer of these options, the value of your options will increase or decrease accordingly.

For example, the buyer of the put options has the right to sell the stock at a predetermined strike price. If prices keep on going up, the put options contract logically become less of a value. Because why would the put options buyer want to sell its stocks at the lower strike price of the put options if selling at the market can fetch a higher price? And in this scenario, the seller of the put options who had received premiums/payments from the buyer of the put options will not need to be obliged to buy the stocks from the buyer of the put options. Hence, the put options become worthless on expiry if the price keeps on going up. Thus, put options value decreases when the underlying price of the stock keeps on going up.

Based on the formula of the model, it also makes good sense also that the greater the volatility, the higher the options price/value will be. Higher uncertainty will result in higher premiums due to higher perceived risks. It is the way it should be. It makes good sense too. Bonds by the government has less volatility so we are compensated lesser. As compared to if we invest in say stocks that have higher volatility and higher uncertainty.

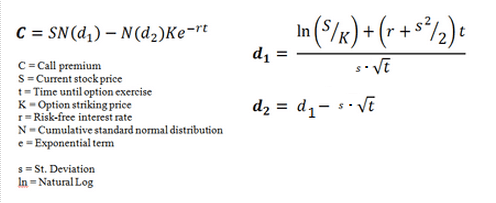

The Original Formula of the Black-Scholes Model

To recap, this is the original formula for Black-Scholes:

Source: Investopedia

The original Black-Scholes formula takes into account the current stock price, time to expiry, options strike price, risk-free interest rate and the cumulative standard normal distribution which is known as the implied volatility or simply how volatile the stock is.

The Limitations of the Original Black-Scholes Model (Dividends Not Accounted for)

Here is the first limitation that I came out with: The underlying price of a stock will usually decrease accordingly by the amount of cash dividend declared on the ex-dividend date of a company. So, dividends do play a role too because it affects the underlying price of a stock. But in the Black-Scholes model, it makes the assumptions that no dividends are paid out during the life of the options. This means that a company that pays a lot of dividends will usually have the stock price decrease in relation to it. If during the course of the options, the company pays those dividends, the put options should be worth more and the call options should be worth less. But the original Black-Scholes model does not take those into dividends into account – and we need to adjust it accordingly. We can do that by subtracting the present value of the upcoming dividends of the stock during the life of the options from the current stock price – in which we then input the subtracted value to the original Black-Scholes model.

The Limitations of the Original Black-Scholes Model (by Warren Buffett)

The second limitation of the Black-Scholes model is one that is pointed out by a person I greatly admire, Warren Buffett himself. It got to do with the Black-Scholes limitations of valuing long-dated options.

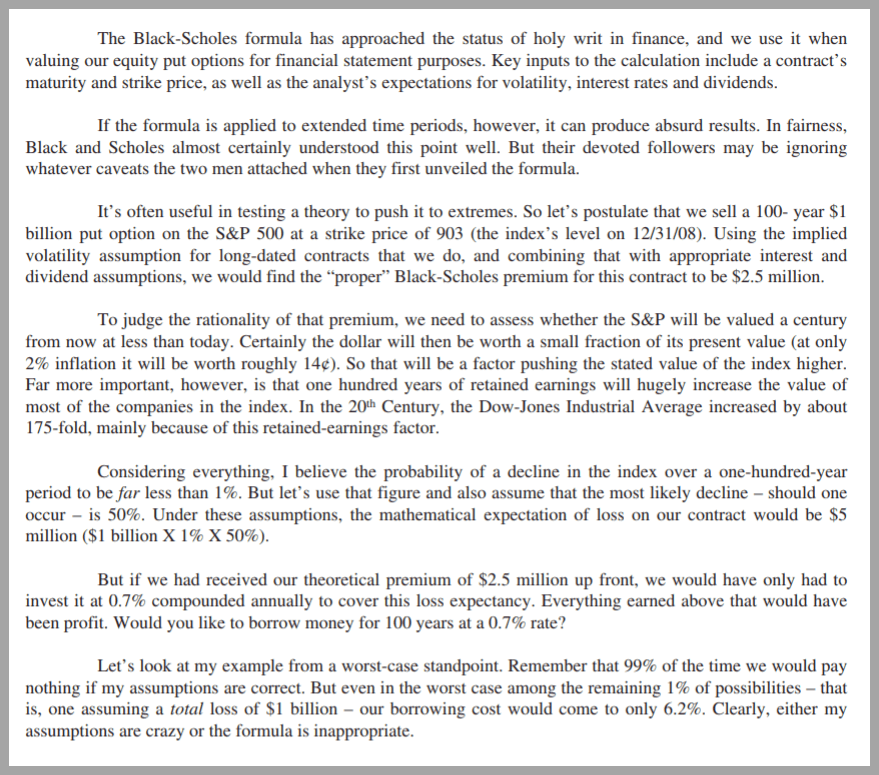

Source: Berkshire Hathaway 2008 Annual Report

Based on Warren Buffett, while the Black-Scholes model has been the widely used model to value equity put options, he thinks that there are limitations to it – when the model is applied to an extended time period, they can produce absurd results. So Waren Buffett is saying that the Black-Scholes model is bad at valuing long-dated options.

Warren Buffett also gives an example to explain this theory of his by pushing it to the extremes as you can see from the image screenshot above. He gave the example of selling a 100-year-old $1 billion put option on the S&P 500 at a strike price of 903 which was the index’s level on 31 December 2008. Using the “proper” Black-Scholes model at the time, he will get a premium of about $2.5 million. And he sees that the expected loss on the contract would be $5 million (by taking $1 billion which is the contract value of the options times a 1% chance that 100 years from now the S&P 500 is going to be worth less and times it by 50% which is the chance of that decline).

Using this example, Warren Buffett said that if he received the $2.5 million up front, he only need to invest and get 0.7% annually for the next 100 years to cover the expected loss. So he said that this is akin to borrowing the money which is $2.5 million for a rate of 0.7% annually. Even at a total loss of $1 billion, the “borrowing cost” will only be about 6.2%.

For Warren Buffett personally, he has made use of these kinds of market inefficiency to sell put options when the volatility is high so that he was able to get more premiums/cash flows. And then he uses these premiums/cash flows to invest and get returns.

“Our put contracts total $37.1 billion (at current exchange rates) and are spread among four major indices: the S&P 500 in the U.S., the FTSE 100 in the U.K., the Euro Stoxx 50 in Europe, and the Nikkei 225 in Japan. Our first contract comes due on September 9, 2019 and our last on January 24, 2028. We have received premiums of $4.9 billion, money we have invested. We, meanwhile, have paid nothing, since all expiration dates are far in the future. Nonetheless, we have used Black-Scholes valuation methods to record a yearend liability of $10 billion, an amount that will change on every reporting date. The two financial items – this estimated loss of $10 billion minus the $4.9 billion in premiums we have received – means that we have so far reported a mark-to-market loss of $5.1 billion from these contracts.” – Warren Buffett

While Warren is able to utilize the volatility of the stock market to get more premiums, he criticizes Black-Scholes as being limited simply because of the financial reporting regulation that forces him to use the Black-Scholes.

Disclaimer:

The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

Is Spotify Stock Invest-Worthy? Seeing it From A Value Perspective.

Daniel Ek has built a great business with Spotify. Now that it has recently IPO-ed in 2018, is this digital music streaming service of his, invest-worthy? I am sure that by now you would most likely have heard of Spotify before. But I am sure that not many of you know that Spotify was founded and […]

2 Billion Users ( > China Population): Why I Am Long on Facebook Stock

But over time, I would like to invest in good businesses at a fair price instead of continuing to invest in an OK business at a cheap price. Due to Facebook’s recent drop in its share price, I took a stake in Facebook during the past few months and right now, it consists of about a quarter of my portfolio.

Part 1 of 2: Here’s How to Use The Black-Scholes Model to Price Options

The Black-Scholes model was first developed by three economists. Two of them – Myron Scholes and Robert Merton – received a Nobel prize in 1997 for their work in this model. The Black-Scholes model is also commonly known as the options pricing model. And as the name indicates […]

New Logo Design for Re-ThinkWealth (Value Investing Blog)

The above image is how the new Re-ThinkWealth logo looks like. As you might have noticed, it is a combination of “R” and “W” which stands for Re-ThinkWealth. At the same time, the shape of the logo embodies the resemblance of how a stock market will behave. The stock market goes down and up […]

Here Are My Reflections After 3 Years 7 Months in The Stock Market

So basically, I knew that if I cannot beat the S&P 500 return over the long run, it’s better if I just invest in the S&P 500. While the S&P 500 practices in a huge diversification of 500 big companies listed in the U.S., my U.S. portfolio practices concentration of ideas in which I am most certain about […]

10 Reasons Why We Should Rethink How to Build Our Wealth

I am 25 years old this year and I am always fascinated by how a change in our thinking can result in a huge change in our wealth. I am convinced by the notion that how we think creates the wealth that we have. And writing has been an integral part of it all because it gives me an avenue to pen […]

Here’s My Quick Thought on Starbucks Stock

Starbucks is a company that needs not much introduction. I am sure that most of us have drunk Starbucks coffee before. And many of us have studied or did some work or caught up with a friend there. Starbucks is a familiar company that is in almost every airport around the world. Their story though started back in Seattle […]

Theranos Incident Shows Why It’s Dangerous to Invest Based on Hopes And Dreams

I do admit that a business is nothing without goals, hopes, and dreams. A successful business requires the founder to have a vision and to be able to turn that vision into reality. A successful business is one that has managed to turn hopes and dreams into reality. And by reality, I mean cash. Cold hard cash. Think Apple, […]

Qualcomm Will Not Supply Apple’s 2018 iPhones – And That is Okay (Q3 2018 Results)

Qualcomm is the company that supplies phone makers like Samsung, Xiaomi, Huawei, Apple chips so that their phone can be a “smartphone.” Different chip suppliers will have different chips. And just by having a different chip, the performance of the phone can vary greatly. I am vested in Qualcomm since 24 January 2018 at an average price of about $53. Here are the […]

Thinking of Betting in World Cup 2018 or Investing in Stocks? Read this first.

1. Soccer is very unpredictable – The ball is round. as of 28 of June 2018 in the qualifying round, Germany is out of the world cup. Who could have predicted that? Not UBS and Goldman Sachs, that’s for sure, who predicted Germany would win the cup and go to the final respectively. 2. The more the potential payout, the lesse […]

24/3/2017 Was The First Time I Bought GameStop: About Time a Private Equity Firm is Interested in it!

Because the fact is that today, it is reported by Reuters that GME has received buyout interest and is holding talks with private equity firms about a potential transaction. Seems like Sycamore Partners – one of the PE firms that have expressed interest in GME agrees with my conclusion and analysis that GME is mispriced […]

Sony – Deep Value?

Sony is at an inflection point after years of restructuring. Having shed and restructured loss-making business units, it comfortably exceeded its 2014 medium-term plan to deliver an ROE of 10% and operating profit of JPY500bn in FY17. The company is seeing a number of tailwinds for games, music, and the semiconductor segments […]

Wait, Wait!

I often share insights that I do not share in this blog over at my Facebook page. Don’t forget to like it before you go!

Here Are 4 Reasons Why Intel Stock Plunged 16% Last Friday

Last Friday on 24 July 2020, Intel closed 16.24% down. Although I do not own any Intel stock, I was curious why it fell after releasing its Q2 2020 results. Just a while ago, I saw the news that after 15 years of partnership, Apple decided to break up with Intel and stop using its […]

My 5 Key Takeaway From Temasek Portfolio Value in 2020

1. Temasek Portfolio is Huge. Although I know that Temasek has a huge portfolio, I was surprised to see that it is around the size of Warren Buffett’s. As of 31 March 2020, the net portfolio value or NPV is at S$306 billion. So we have our own Warren Buffett in Singapore, that is […]

What I Learnt From Adam Smith About Investment and Money

Who is Adam Smith? Adam Smith (1723-1790) was a philosopher and economist who was best known for authoring the book An Inquiry into the Nature and Causes of the Wealth of Nations. Wealth of Nations also happens to be one of Warren Buffett’s favourite books […]

A List of Value Investing Funds in Singapore and Outside of Singapore

As a value investor, as a practitioner of value investing, I am very interested in studying funds I view as an executioner of the various value investing methodologies I myself am very passionate about. In this article, I will list down some of the value investing funds in […]

Protected: My Gratitude Journal as An Investor (And The Benefits of It)

There is no excerpt because this is a protected post.

How to Get Rich by Investing in Stock Market? Patience

How do people get rich by investing in stocks? Can we actually get rich by investing in stocks? Yes, we can. But we need to utilize both Patience and Compound Interest in Great Companies. With the proper foundation, framework, character, and skills, I truly believe that […]

Here’s What Sun Tzu Art of War Quotes Can Teach Us About Investing

Sun Tzu Art of War Quotes “He will win who knows when to fight and when not to fight” – We should only invest when there is clear benefit to do so, do not do something just for the sake of doing something. “If you know the enemy and know yourself, you need not fear […]

Thinking, Fast and Slow Book Summary (What I Learnt As An Investor)

In this thinking fast and slow book summary, I will explain to you the various human biases that we have and why it is important for us as investors to understand it. It all begins with a simple premise that we all have two systems in our brain, system 1 and system 2 […]